We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

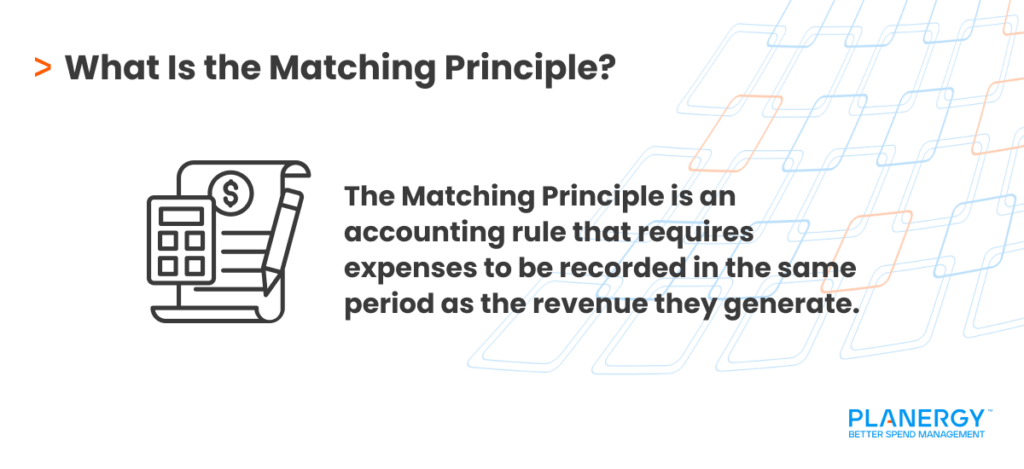

The matching principle ensures expenses are recorded in the same period as the revenue they generate, improving financial accuracy under accrual accounting.

It distinguishes between period costs (recorded when incurred) and product costs (allocated over time to match revenue).

Applying the matching principle correctly prevents distorted financial statements and supports better decision-making and performance analysis.

While essential, the principle can be challenging when dealing with indirect costs, long-term projects, and estimates like depreciation or marketing impact.

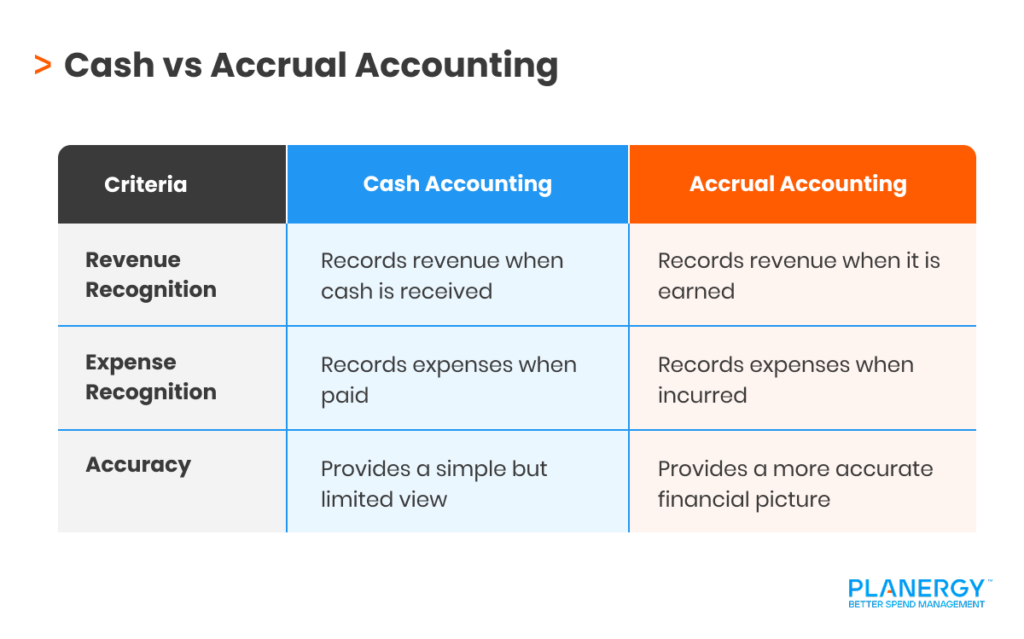

Businesses generally have two accounting methods to choose from: cash basis accounting and accrual basis accounting. The cash method is simple – you record cash when you receive it and you record expenses when they’re paid.

The accrual method, while more complex, is also more accurate. In accrual accounting, you record revenue when it’s earned and expenses when they occur.

In most cases, the accounting is straightforward, but it can get complicated when you’re dealing with things like commissions, journal entries, bonuses, and amortization and depreciation expense.

That’s when you need to use the matching principle, which helps ensure that you record transactions properly.

What Is the Matching Principle?

One of the ten Generally Accepted Accounting Principles (GAAP), the matching principle has a cause-and-effect relationship that ensures that expenses are recorded in the same reporting period as the corresponding revenue.

Also known as the expense recognition principle, the matching principle uses adjusting entries typically completed at the end of the accounting period to record any expenses that are directly related to revenue.

The matching principle has two components, period costs and product costs, with each recorded differently.

Period Costs

Period costs are costs that are not directly related to a product or service, such as office rent, officer salaries, and other overhead expenses, and should be recorded when they’re incurred.

For instance, the expense for September’s rent would be recorded in September, even if it’s paid in August.

Product Costs

Product costs are handled differently. For instance, when you purchase machinery for a factory with a useful life of 5 years, the cost should be depreciated each month, so it matches with the subsequent revenue earned from purchasing the machinery.

Another example of the matching principle is employee commissions. If John earns $5,000 in commissions for June, with payment made in July, the expense is recorded in June—the same month the revenue was earned, not when the bonus is paid.

Why Is the Matching Principle Important?

The matching principle is a core component of GAAP and ensures that financial statements, such as the income statement and balance sheet, are consistent and compliant with all GAAP rules.

Recording revenue or expenses in the wrong accounting period can severely distort financial statements and inflate expenses or lowering profits, while recognizing revenue in the wrong period can inflate profitability in one period and understate it in another.

Recording revenue and expenses properly ensures financial statement accuracy.

The matching principle also provides an accurate basis for decision-making. It’s impossible to understand when to cut spending or move toward expansion if you can’t rely on the information included in your financial statements.

Finally, if you’re running financial ratios to compare your business performance against the competition, it’s essential that the information on your financial statements, which provides the basis for your ratio calculations, is accurate.

What Are the Challenges of the Matching Principle?

Despite its usefulness, the matching principle also presents some challenges, mainly when dealing with more complex issues such as long-term projects and depreciation.

While posting the bonus allocation expense to the correct revenue month is easy, other decisions may require subjective judgment.

Those using a manual accounting method may also struggle with recording accrued expenses in a timely fashion.

Indirect or shared costs, as well as non-cash items, are also difficult to match to revenue, and inventory, if not managed properly, can pose a challenge as well.

Even a simple expense, such as marketing or advertising, can be difficult to allocate properly.

For example, if you decide to run an online ad for three months, you’ll likely see revenue derived from it months afterward, making it difficult to match the expense to the revenue as accurately as you might like.

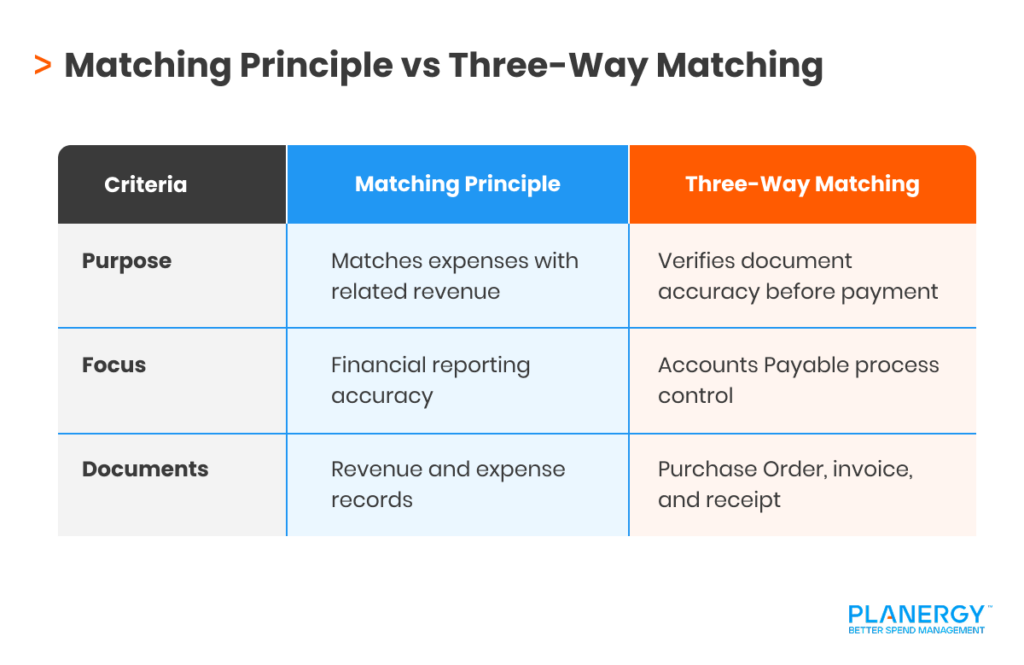

What Is the Difference Between the Matching Principle and Three-Way Matching?

The matching principle and three-way matching may sound similar, but they are two very different processes.

The matching principle ensures that revenues and related expenses are recorded in the same accounting period, while three-way matching is a procedural component used in accounts payable that matches a purchase order, an invoice, and a packing slip.

The matching principle focuses on recording accounting transactions properly, while three-way matching is used to ensure document accuracy and authenticity.

For instance, Company A uses the matching principle to record a sale and the corresponding bonuses that will be paid to salespeople in the same accounting period, regardless of when payment is received or bonuses are paid.

On the other hand, Company A uses the three-way matching process to verify order and invoice accuracy before an invoice is paid, comparing the following information on all three documents (purchase order, invoice, and packing slip) to verify accuracy:

Quantity

Services provided

Product or service description

Price

Terms

If there is a discrepancy or an exception is found, Company A will delay invoice processing until the discrepancy is fully investigated.

What Is the Difference Between the Matching Principle and the Revenue Recognition Principle?

The revenue recognition principle is designed to be used in conjunction with the expense recognition principle, with both used to ensure that any related revenue and expense transactions are posted in the same accounting period.

Revenue recognition states that revenue should be recognized when it is earned, not when it is received.

Let’s say on August 31, you sell $10,000 worth of supplies to a customer. You would record the revenue in August, even though you won’t be paid for another month.

Keep in mind that the revenue recognition principle is part of the matching principle, which states that all corresponding expenses should be recorded in the same period as the revenue.

So, if your salespeople are receiving a bonus on the $10,000 sale, the bonus expense should also be recorded in August as an accrual, even though it won’t be paid until the following month.

How Does the Matching Principle Relate to Financial Statements?

Using the matching principle has an immediate impact on the accuracy of your financial statements.

Income Statement

The matching principle directly impacts your income statement by correctly matching expenses and revenues in the same accounting period, rendering accurate profit totals.

Balance Sheet

The matching principle also impacts balance sheet accuracy by ensuring that expenses are decreased as revenue is received.

Profit Margin

Finally, the matching principle also affects your reported gross and net income totals, directly impacting your profit margin.

Using the principle properly also eliminates the possibility of understated or overstated profits, which in turn directly affects statements and tax liability.

How Do Businesses Make Sure Their Financial Statements Show the True Picture of Their Operations?

Businesses can ensure the accuracy of their financial statements by investing in the latest technology, such as an automated accounting software system.

An automated system makes it easier to implement robust internal controls that ensure financial statement accuracy, such as segregation of duties, three-way matching, regular account reconciliations, and regular audits.

Automation also reduces manual errors and offers real-time reporting to all stakeholders.

Publicly held businesses should also include proper disclosures when issuing financial statements, outlining current policies and providing notes and explanations for any unusual activity noted in the statements.

Why Is Accuracy So important?

Accurate financial statements are a necessity for all stakeholders, including company officers such as the CFO and CEO.

They’re also vital for both potential and current investors, creditors, and regulatory agencies. Inaccurate statements can lead to a host of issues including:

Overstated Profits Overstating profits results in paying too much in taxes and also impacts investor relations if profits are not accurately stated on the income statement.

Understated Profits Understating profits can be just as detrimental to your business. Understating profits can mean an inability to obtain a loan or attract investors, blocking expansion efforts.

Uninform Decision-Making Every business decision, from whether to add or reduce staff, add or eliminate products and services, and even whether to purchase new equipment, relies on accurate financial statements.

Financial statement accuracy also provides a host of benefits to businesses, including:

Easier Adherence to Regulatory Standards If you’re a publicly held company, accurate financial statements are not only a good idea, but a requirement.

Organizations like the Financial Accounting Standards Board (FASB) or the International Financial Reporting Standards (IFRS), have strict requirements for financial reporting from publicly traded companies.

Improved Operations It’s impossible to manage your company’s finances effectively if you’re working off inaccurate financial statements. Having an accurate view of your financial health allows you to make more informed decisions.

More Effective Monitoring

Financial ratios are an easy way to manage financial performance, spot trends, track performance, and make timely changes. But without accurate financial statements, all of those ratio results will be useless.

Better Lending and Credit terms Financial statements are used by creditors and investors alike to view your company’s financial health. Inaccurate financial statements can impact your ability to obtain a loan or enjoy favorable credit terms.

Ability to Spot Fraudulent Activity Without accurate financial statements, it’s difficult to spot potentially fraudulent activity.

Accurate financial reporting isn’t just for publicly held businesses. Even small business bookkeeping will benefit from accurate financial statements.

From empowering decision-makers to gaining a stellar reputation in the business world, having access to accurate financial statements is a must.

What’s your goal today?

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")