The global payments landscape in 2025 is fast, fluid, and full of momentum. Across industries and regions, the way people and businesses transact is being reshaped by digital wallets, real-time payments, AI-driven security, and rising consumer expectations.

With payments revenue set to reach $3.1 trillion by 2028 and digital wallets expected to power $25 trillion in transactions by 2027, the evolution of payments is not slowing down—it’s accelerating.

While the last few years laid the foundation, 2025 is about execution. Businesses are scaling up infrastructure to support instant, secure payments.

Consumers are ditching physical wallets for mobile-first convenience. And regulators are navigating emerging technologies like Buy Now, Pay Later (BNPL), cryptocurrencies, and Central Bank Digital Currencies (CBDCs).

So, what’s shaping the industry this year—and what lies ahead? This report breaks down the latest trends, stats, and innovation hotspots defining global payments in 2025.

Revenue and Growth: Payments as a Global Powerhouse

The payments industry continues to gain ground in 2025. What started as a rebound from the pandemic has now become sustained momentum.

Global payments revenue reached $2.4 trillion in 2023, and it’s projected to grow at 5% annually, hitting $3.1 trillion by 2028.[3]

Payments are on track to represent 35% of total banking revenue by 2028, underscoring the sector’s central role in financial services.

Growth is being driven by several key segments. Merchant acquiring services, for example, are expected to grow at a 8.7% compound annual growth rate (CAGR) and surpass $160 billion in revenue by 2026.[1] Non-bank players are also reshaping the market, having doubled their volume in the U.S. between 2019 and 2021.[1]

In 2025, the focus is on scalability and innovation—real-time systems, AI, and seamless cross-border payments.

With digital wallets projected to handle $25 trillion in transactions by 2027, payment providers are under pressure to deliver convenience, speed, and trust at scale.[9]

The Rise of Digital Wallets: Ubiquity in Transactions

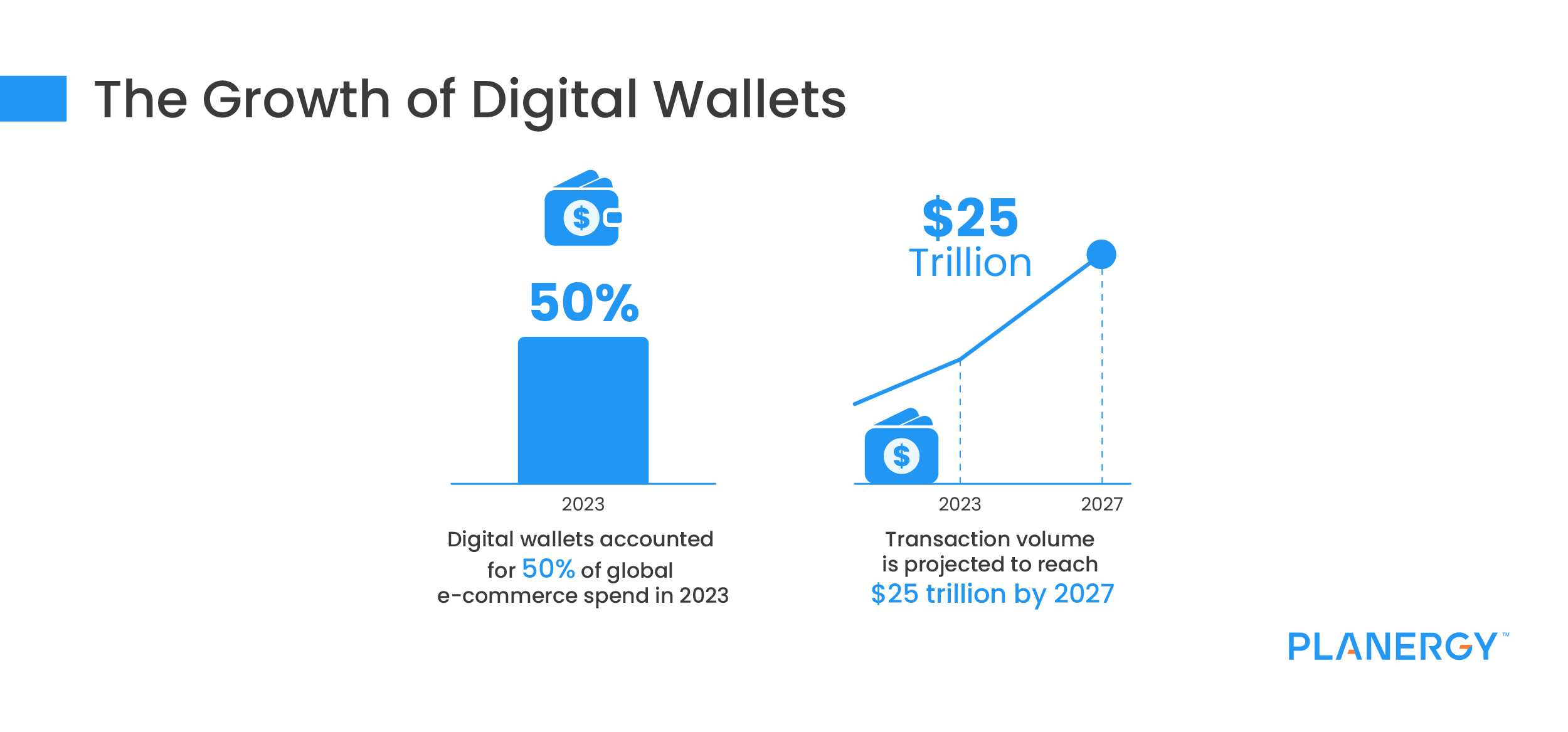

Digital wallets have firmly cemented their place as a dominant force in payments.

In 2023, wallets accounted for 50% of global e-commerce spend (over $3.1 trillion) and 30% of point-of-sale (POS) spend (over $10.8 trillion).[9]

That momentum has only grown in 2025, with global wallet transactions expected to hit $25 trillion by 2027 across both e-commerce and in-store transactions.[9]

Consumer behavior continues to evolve. One in five users now leaves the house without a physical wallet, relying entirely on digital options.[4] In the U.S., 28% of consumers now use in-store digital wallets—up from 19% in 2019.[4] Globally, digital wallet adoption now powers over $10 trillion in consumer-to-business spending annually.[4]

APAC leads the pack, where wallets account for 70% of e-commerce transactions.[9] Europe and North America are catching up, with wallets projected to grow at a 17% CAGR through 2027.[9] Whether it’s PayPal and Apple Pay or regional leaders like Swish in Sweden, wallets are now a fixture—not a feature—of global commerce.

Cash, Cards, and Real-Time Payments: A Shifting Balance

The global shift away from cash continues to accelerate. By 2024, cash usage had fallen to 80% of 2019 levels, declining at about 4% annually.[3]

In emerging economies like India, cash’s share of consumer payments is expected to drop from 23% to under 10% by 2028.[3] In the U.S., cash now accounts for just 5% of consumer payment value.[3]

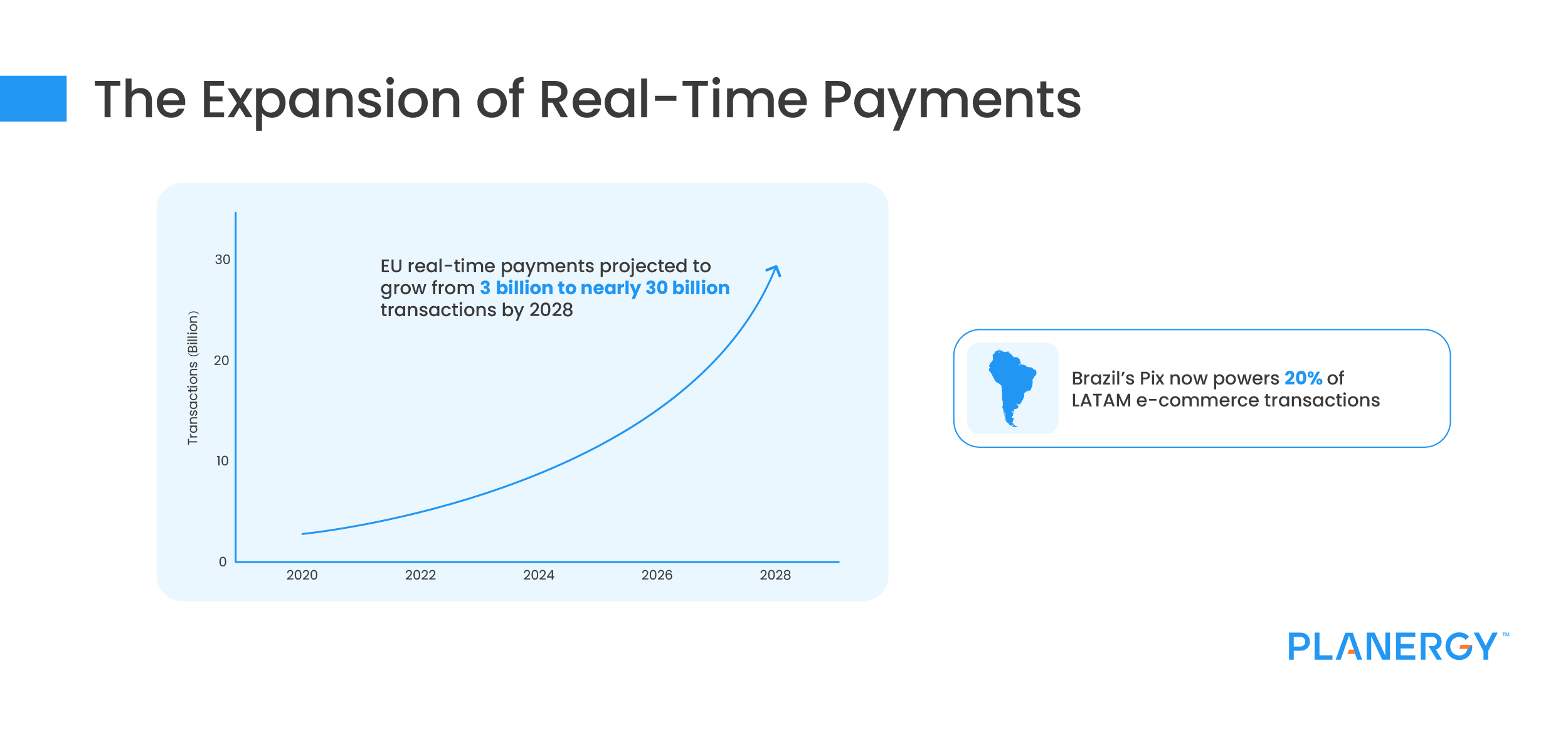

At the same time, real-time payments are reshaping how money moves. In the EU, instant payment transactions are projected to grow from 3 billion to nearly 30 billion by 2028, a 50% annual increase.[3] Countries like Brazil and India are paving the way through government support and regulatory mandates.

Cards remain a core channel, with global credit card transactions growing by $800 billion between 2021 and 2022—surpassing $13 trillion.[1]

However, with competition from QR codes, digital wallets, and account-to-account (A2A) payment rails, traditional card models are facing more pressure than ever to innovate and evolve.

Emerging Technologies: AI, Fraud Prevention, and Beyond

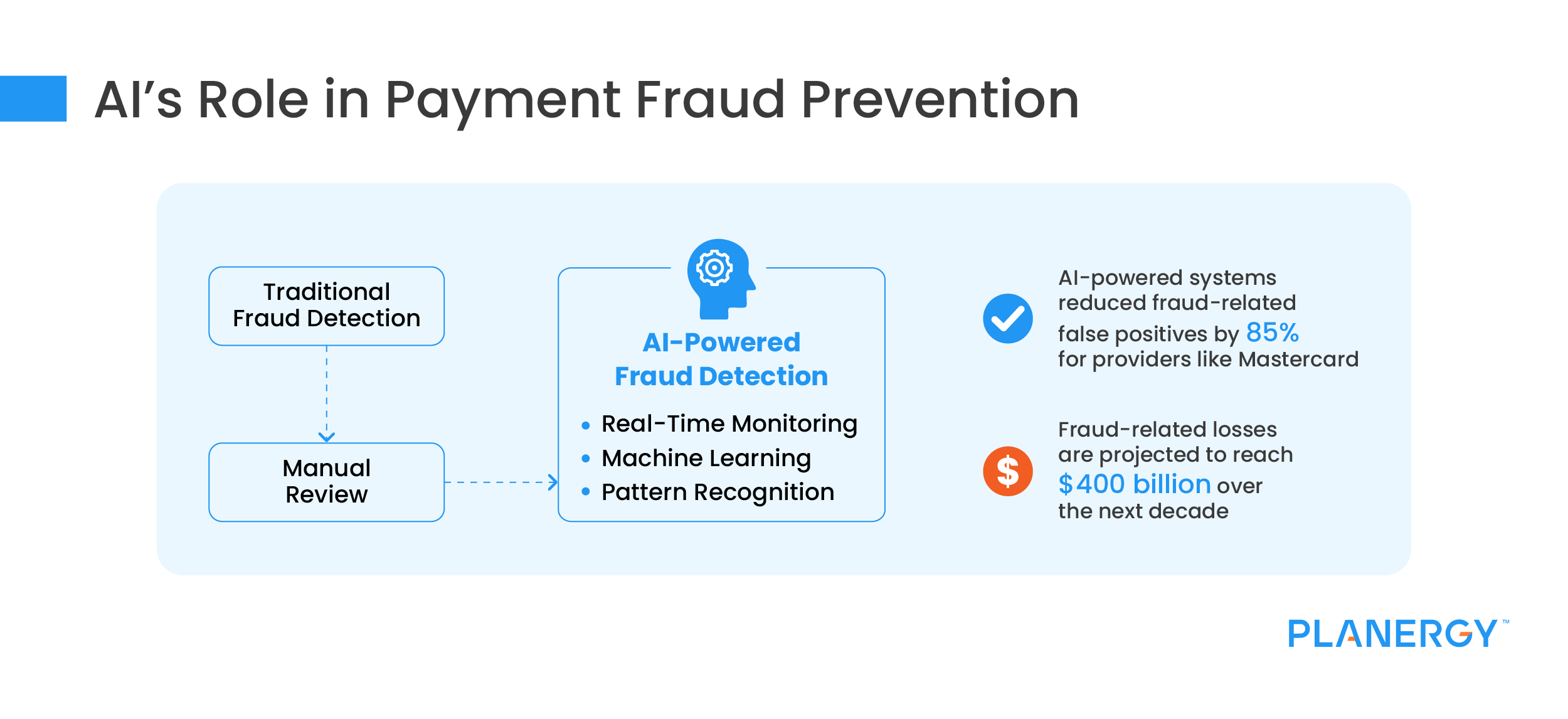

Emerging technologies are reshaping how payments are processed, verified, and protected in 2025. Artificial intelligence (AI) is leading the charge—particularly in fraud prevention.

While payment card fraud losses are projected to reach $400 billion over the next decade, companies like Mastercard have already reduced fraud-related false positives by 85% using AI.[8][3]

Beyond fraud, AI and machine learning are also helping to optimize approval rates, detect anomalies, and reduce false declines.

Augmented reality (AR) is making its way into e-commerce, with 53% of businesses planning to integrate AR to create immersive shopping experiences.[2]

On the infrastructure side, 24/7 real-time payment availability is becoming the norm. Banks are investing in ISO 20022 and machine learning-powered compliance systems that improve transaction screening and reduce false positives.[6]

These changes are creating faster, smarter, and more inclusive payment networks—one transaction at a time.

Buy Now, Pay Later (BNPL): From Retail to Travel

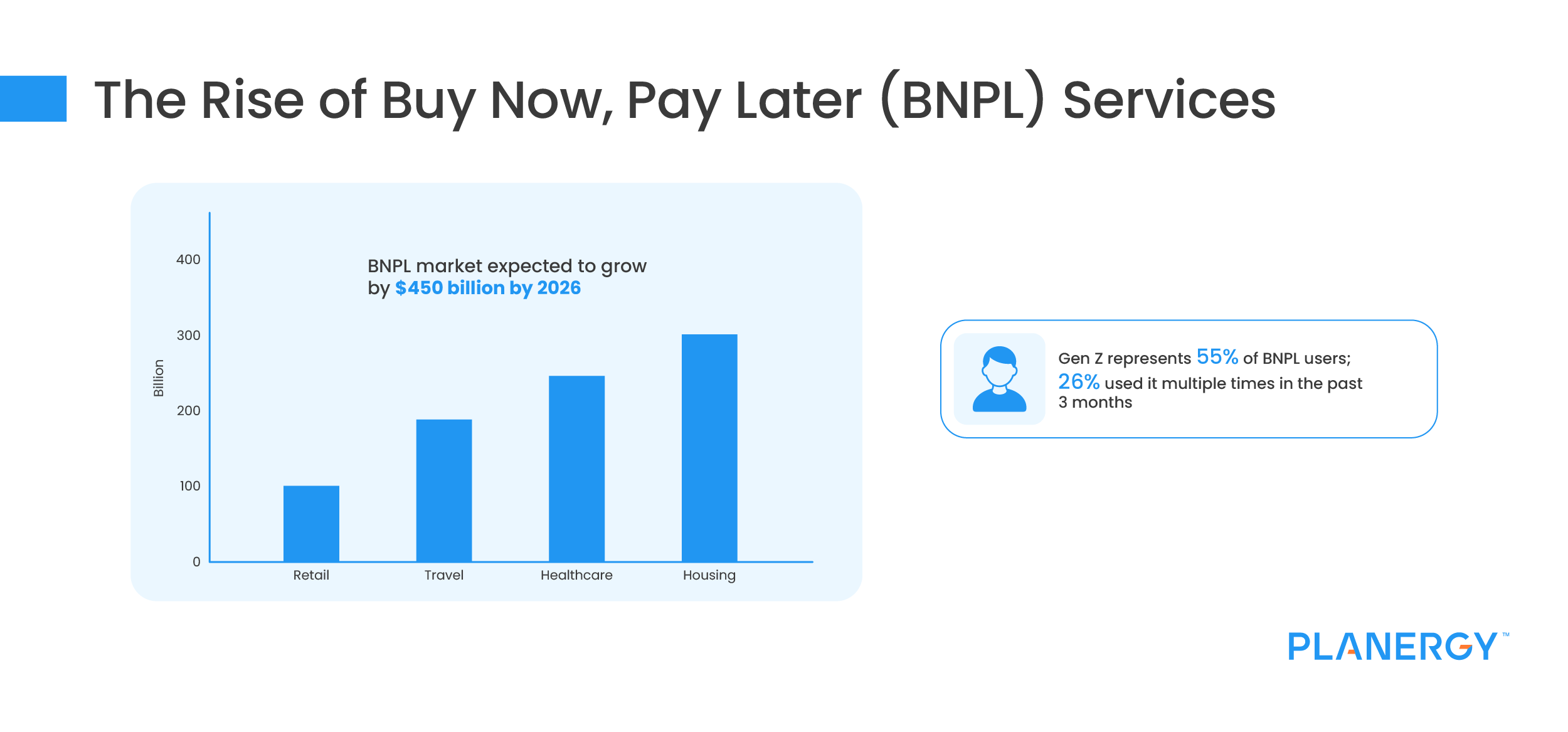

BNPL services are expanding far beyond fast fashion. In 2025, this payment option is enabling access to larger purchases, wider demographics, and new sectors. The market is forecast to grow by $450 billion by 2026.[2]

In terms of user behavior, Gen Z accounts for 55% of BNPL penetration, with 26% of this group having used BNPL multiple times in just three months.[2] BNPL is also gaining traction in travel, where 71% of consumers say they would use it to fund vacations. Merchants offering BNPL through PayPal report 31% higher average order values.[2]

It’s even being used for big-ticket expenses: Providers like Affirm and PayPal now offer credit limits of up to $20,000.[8] As the model grows, regulators are taking note.

In the U.S., the Consumer Financial Protection Bureau (CFPB) is reviewing rules to ensure responsible lending and consumer protection.[8]

Cryptocurrencies and Central Bank Digital Currencies (CBDCs)

Crypto and CBDCs continue to shape the digital payments narrative in 2025. The number of crypto wallets surged by 75% between 2020 and 2022, reaching 81 million globally.[1]

Market revenue is also on the rise—projected to grow from $34.9 billion in 2023 to $64.9 billion by 2027, at a 14.4% CAGR.[2]

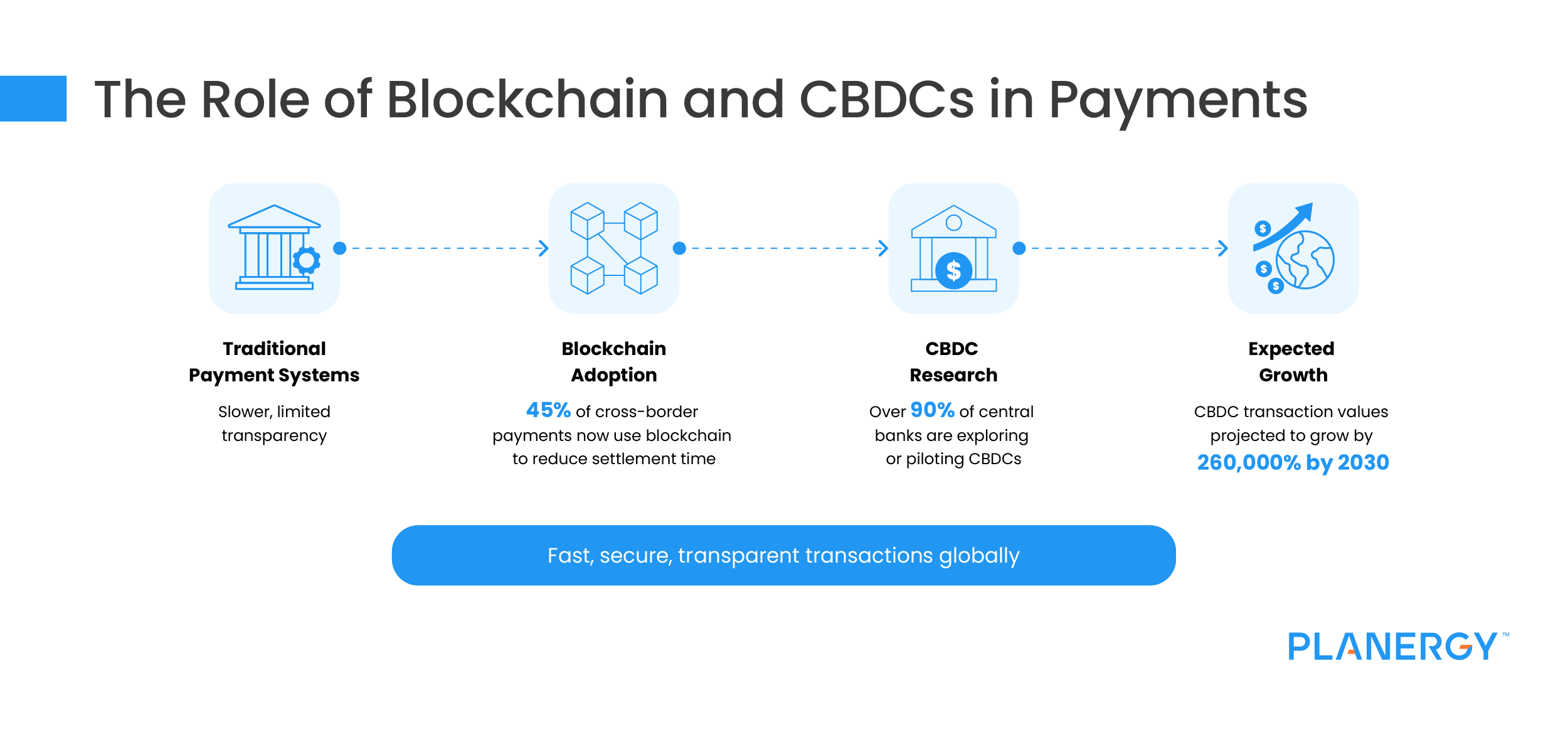

CBDCs are gaining serious traction. Over 90% of central banks are exploring or piloting CBDCs, and more than 30 pilot programs are currently underway.[3] Their value proposition? Faster cross-border payments, financial inclusion, and reduced dependence on stablecoins.

Take the Inthanon-Lionrock initiative, a cross-border CBDC project between Thailand and Hong Kong—it’s setting the standard for future collaborations.[5] Meanwhile, the global CBDC transaction value is projected to surge by 260,000% by 2030.[5]

Geopolitically, trends like de-dollarization are influencing global flows. As countries explore local alternatives and the BRICS bloc discusses a shared currency, traditional global payment structures may soon look very different.[5]

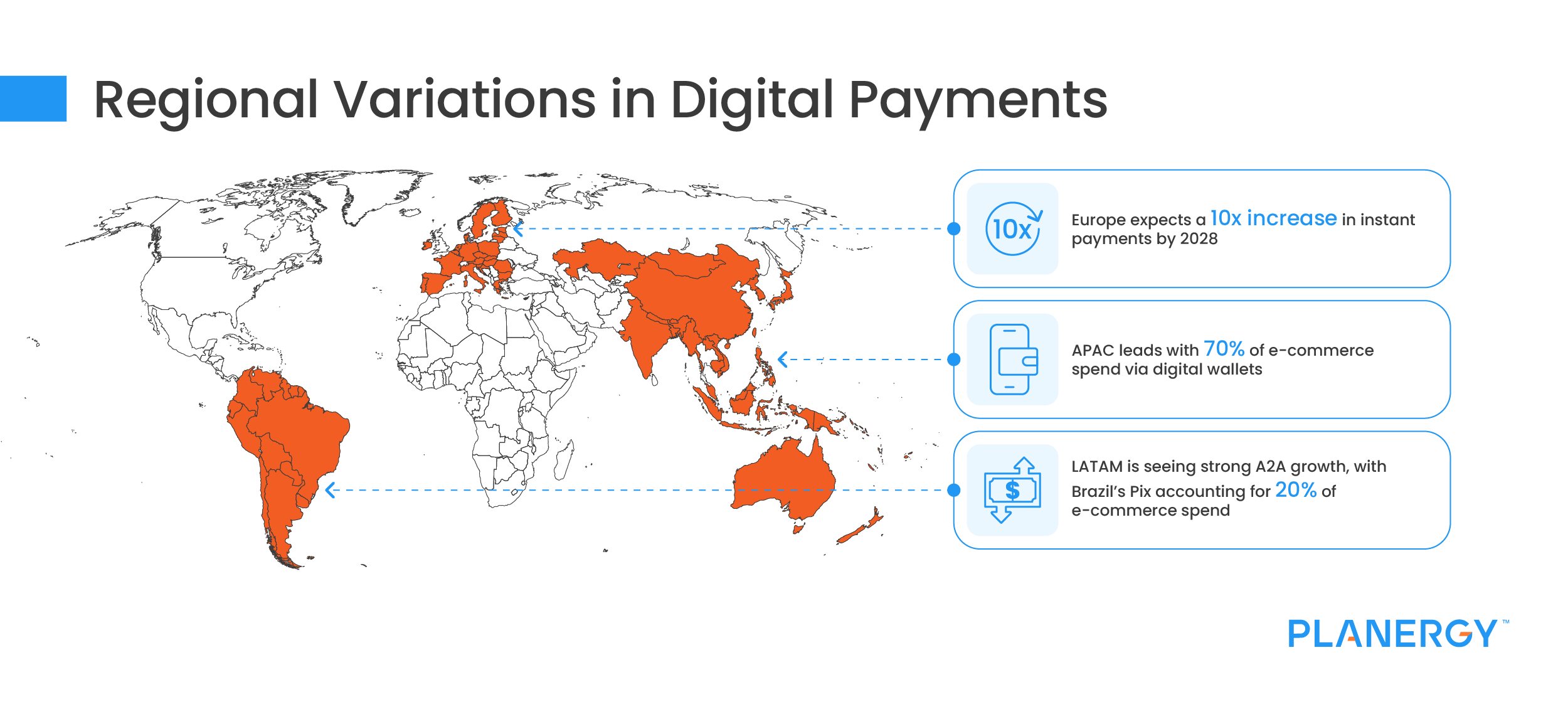

Regional Snapshots: Payment Dynamics Across the Globe

Payment habits vary widely by region—and in 2025, the differences are even more pronounced.

In APAC, digital wallets dominate. 70% of e-commerce and over 50% of POS transactions were processed via wallets in 2023.[9] India continues to reduce cash reliance, where usage is expected to fall to under 10% of consumer spending by 2028.[3]

Europe is closing the gap, with wallets accounting for 30% of e-commerce spend today and projected to grow to 40% by 2027 at a 17% CAGR.[9] Instant payments are also growing fast here, jumping from 3 billion to 30 billion transactions by 2028.[3]

LATAM is accelerating A2A adoption, with Brazil’s Pix handling 20% of all e-commerce spend.[9] In North America, card-backed wallets are growing steadily—while 52% of e-commerce and 73% of POS spend still flows through cards.[9]

In the Middle East and Africa (MEA), wallet adoption is rising rapidly, with 35% year-over-year growth, highlighting the region’s move toward modern, mobile-first payment systems.[9]

ESG and Sustainability in Payments

Environmental, social, and governance (ESG) goals are becoming central to payments innovation in 2025. Over 75% of the world’s largest 250 companies have committed to reducing carbon emissions—and payment providers are following suit.[1]

We’re seeing the rollout of eco-friendly cards, digital wallets with carbon tracking tools, and ESG-linked transaction reporting.

These features aren’t just good PR—they’re becoming part of consumer expectations.

As sustainable finance grows, payments are emerging as a way for companies to align business goals with broader environmental impact.

Green fintech solutions are gaining traction, especially in Europe and Asia, where regulators are placing sustainability front and center. In this new era, ESG isn’t just about compliance—it’s a competitive advantage.

Conclusion: The Future of Payments

Payments in 2025 are fast, smart, and increasingly seamless.

With digital wallet volume expected to reach $25 trillion by 2027[9], instant payments scaling across more than 80 countries[6], and AI making fraud detection more precise than ever, the industry is thriving.

But the path forward demands agility. Providers will need to balance innovation with regulation, invest in security, and tailor offerings to local habits.

Whether through CBDC pilots, BNPL expansion, or ESG integrations, payments are no longer just transactions—they’re a strategic lever for growth, trust, and global inclusion.

References

[1] Mastercard Services. State of Global Payments: Six Trends Shaping the Industry. Available at: https://www.mastercardservices.com/en/advisors/payments-consulting/insights/state-global-payments-six-trends-shaping-industry. [Accessed on: 20 November 2024]

[2] PayPal. 8 Payment Technology Trends 2024. Available at: https://www.paypal.com/us/brc/article/8-payment-technology-trends-2024. [Accessed on: 20 November 2024]

[3] McKinsey & Company. Global Payments in 2024: Simpler Interfaces, Complex Reality. Available at: https://www.mckinsey.com/industries/financial-services/our-insights/global-payments-in-2024-simpler-interfaces-complex-reality. [Accessed on: 21 November 2024]

[4] McKinsey & Company. State of Consumer Digital Payments in 2024. Available at: https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/state-of-consumer-digital-payments-in-2024. [Accessed on: 22 November 2024]

[5] Statista. Share of Global Payments by Currency (2024). Available at: https://www.statista.com/statistics/1189498/share-of-global-payments-by-currency/. [Accessed on: 22 November 2024]

[6] Capgemini. World Payments Report 2024. Available at: https://www.capgemini.com/insights/research-library/world-payments-report/. [Accessed on: 22 November 2024]

[7] J.P. Morgan. Payments Are Eating the World. Available at: https://www.jpmorgan.com/content/dam/jpm/treasury-services/documents/jpm-payments-are-eating-the-world.pdf. [Accessed on: 21 November 2024]

[8] Deloitte. Shaping the Future of Payments: Trends and Insights for 2025. Available at: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/financial-services/us-shaping-the-future-of-payments-trends-and-insights-for-2025.pdf. [Accessed on: 22 November 2024]

[9] Worldpay. Global Payments Report 2024. Available at: https://worldpay.globalpaymentsreport.com/en. [Accessed on: 22 November 2024]

")

")

")