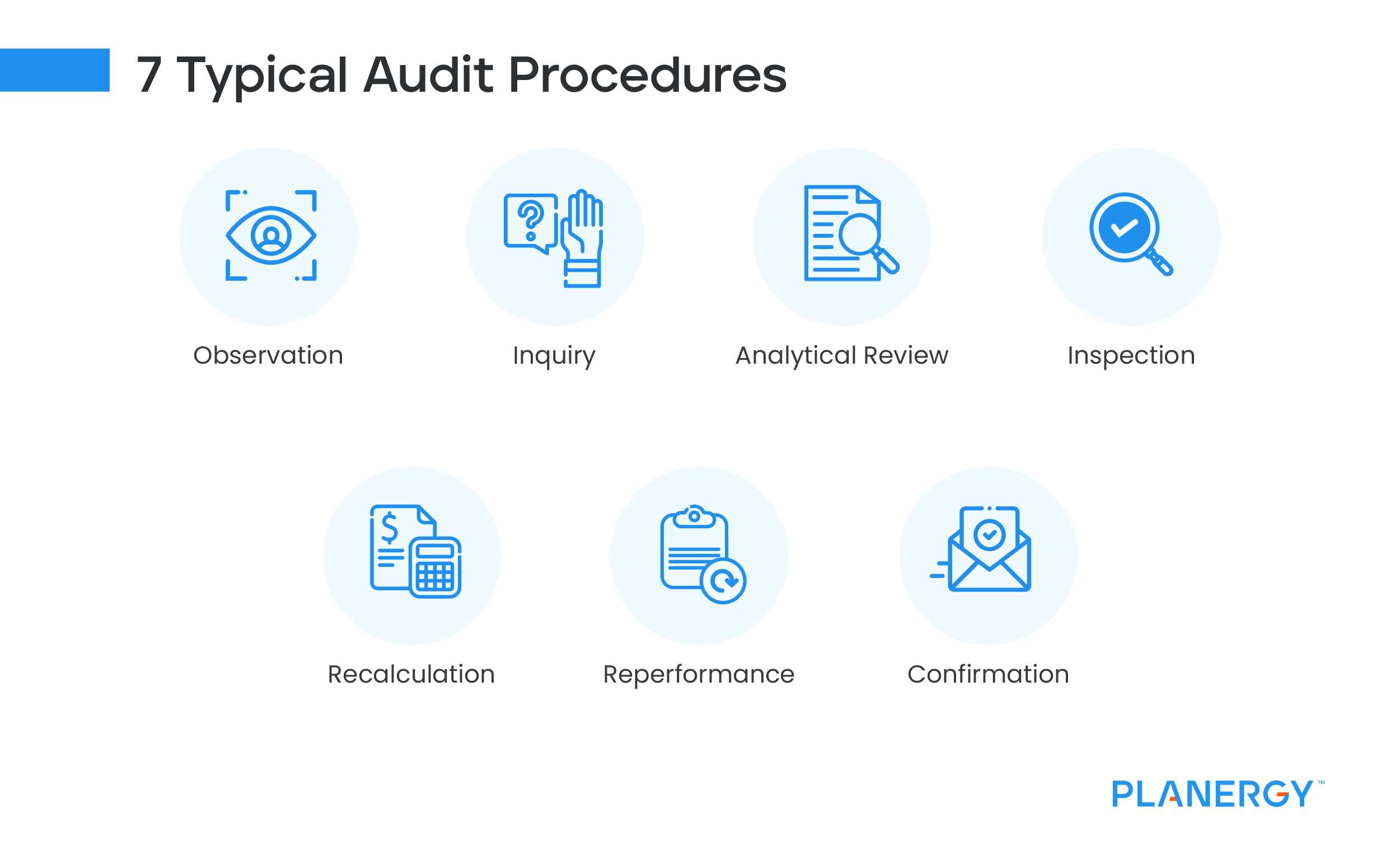

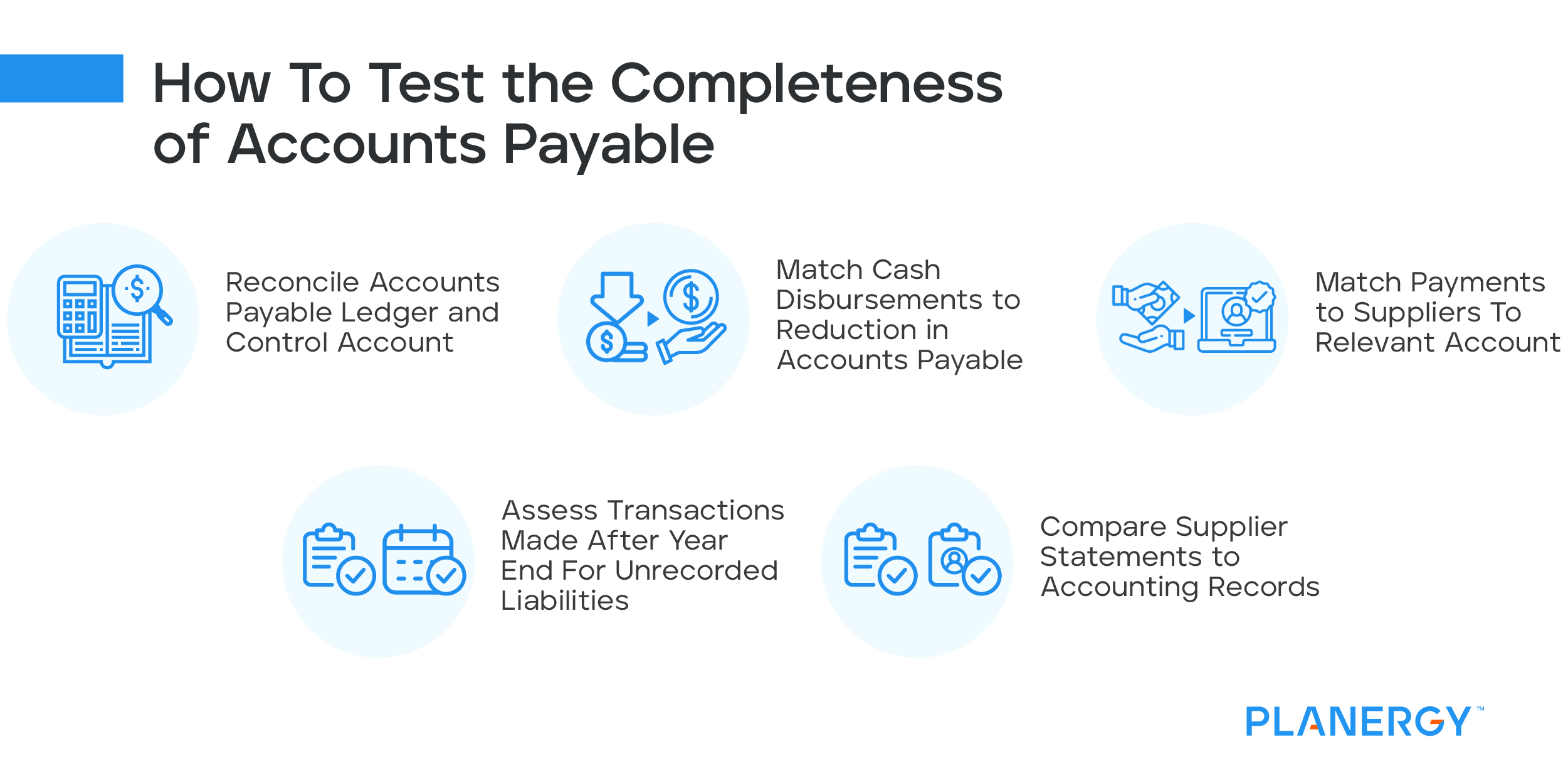

An accounts payable audit is an independent review of all accounts payable procedures and records. An accounts payable audit is a necessity for all businesses, regardless of size.

For larger businesses, an accounts payable audit isn’t an option – it’s a requirement. With the introduction of the Sarbanes-Oxley Act in 2002, if you’re a publicly held company, you are required by law to submit all appropriate records for an independent audit.

But small businesses aren’t off the hook. Even if your business is privately owned, an independent audit is a good risk assessment tool that can help you uncover potential fraud or identify other weak spots in your accounting procedures.

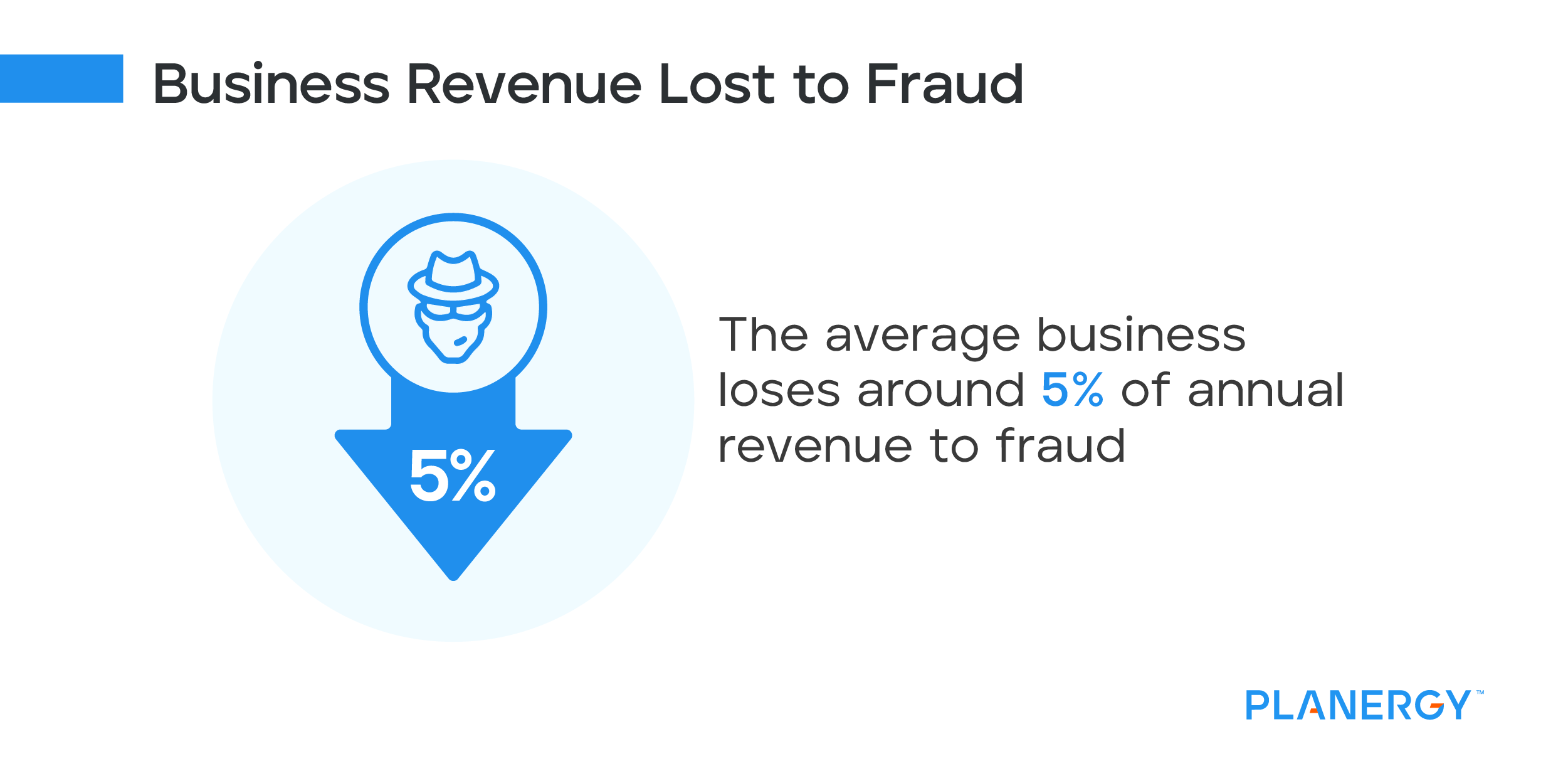

In a 2020 study, the Association of Certified Fraud Examiners found that the average organization loses around 5% of revenue to fraud. Whatever size business you work for, losing 1/20th of your profits to fraud has a huge impact.

The same study identified that lack of internal controls contributed to nearly 1/3 of all fraud. Conducting an audit regularly, even an internal audit, can keep your business financially healthy for the long term.

")

")

")