We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

GAAP ensures consistency, accuracy, and transparency in Accounts Payable by requiring standardized financial reporting and accrual-based accounting.

Accounts Payable is recorded as a current liability, increasing with credits when invoices are received and decreasing with debits when payments are made.

Strong internal controls—like segregation of duties and regular reconciliation—are essential for fraud prevention and compliance in AP processes.

Automating Accounts Payable workflows helps businesses maintain GAAP compliance while improving efficiency, accuracy, and financial visibility.

Whether you’re a small, local business or a national corporation, adhering to Generally Accepted Accounting Principles (GAAP) is essential.

Adhering to GAAP and other accounting rules like the International Financial Reporting Standards (IFRS), helps a business structure its accounts payable process to be in compliance with rules and regulations while ensuring financial statement accuracy.

What is Accounts Payable?

Accounts Payable is debt representing money owed to vendors and suppliers for materials or services purchased on credit.

The Accounts Payable balance recorded on a company’s balance sheet is considered a current liability because it is considered a short-term debt that will need to be paid by a certain date, which varies based on the credit terms provided by the vendor or supplier.

Is Accounts Payable a Debit or a Credit?

Accounts Payable is a liability account, so any new accounts payable invoice is recorded as a credit, which increases the accounts payable balance. When the invoice is paid, the Accounts Payable account is debited, decreasing the balance of the account since the invoice is no longer due and payable.

How is Accounts Payable Different from Accounts Receivable?

Accounts Payable and Accounts Receivable represent money a business owes and money a business is owed.

Mentioned earlier, Accounts Payable is a current liability, since the money owed is payable in less than one year, though typically much shorter time frame, depending on the terms provided by the seller.

Any time an invoice is recorded in Accounts Payable, it is posted as a credit and increases the balance of the account, since any addition to a liability is posted as a credit.

On the other hand, accounts receivable is the exact opposite of Accounts Payable, representing money owed to a business from its customers.

Accounts Receivable is an asset account, with balances considered current assets since they are due in less than a year, with the due date dependent on the credit terms assigned to the customer.

When a sale is made on credit, the sale is posted as a debit, which increases the balance of the Accounts Receivable account. When payment is received, the payment is credited against the Accounts Receivable account, effectively reducing the balance.

Should AR and AP be Segregated?

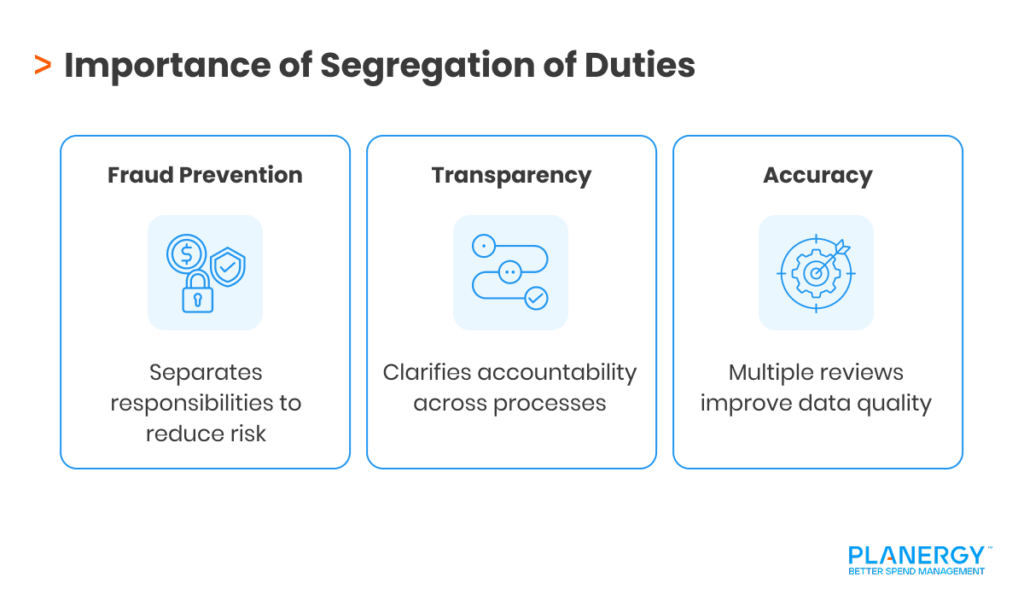

Good internal controls require segregation in both Accounts Payable and Accounts Receivable. Segregating duties helps maintain established controls, reduce fraud risk, and enhance accuracy.

Separating these two vital accounting functions means that one single employee is not responsible for both functions.

For instance, your accounts payable clerk should not also be handling accounts receivable payments from customers. Segregation should also include segregating duties within both AP and AR.

The AP employee who records invoices should not process vendor or supplier payments as well. For AR, the person who submits an invoice to a customer should not be the same person who posts the customer’s payment.

Aside from following GAAP rules, AP and AR segregation offers other benefits:

Reduces fraud since one single employee is not responsible for handling both AP and AR financial data

Increases transparency since management will know who is responsible for each transaction, making it easier to identify issues and irregularities

Having more than one person responsible for AP and AR tasks increases accuracy, since transactions will be viewed by multiple employees

What Are Accounts Payable Accruals?

Accounts Payable accruals are the recording of expenses that have been incurred in the current accounting period but have not been recorded into the accounting system.

For example, by the last week of the month, ABC Company has yet to receive an invoice from their utility company, so they accrue the expense so that it will be recorded in the appropriate month.

To record the accrual, you would debit the utility expense account and credit the accrued expense account. The following month, when the actual bill is received, you would reverse the accrual and record the payable in the correct amount.

Another example would be a plumbing service handling a clogged drain on the final day of the month.

Knowing that you won’t receive the bill until the following month, you accrue the expense to ensure that it’s recorded properly, then reverse it when the bill arrives and process the invoice accordingly.

What Are GAAP Principles?

Generally Accepted Accounting Principles, or GAAP principles, are a set of rules, standards, and procedures created to ensure consistency, accuracy, and transparency in financial reporting.

Publicly traded companies in the U.S. must follow GAAP when preparing financial statements, with the goal of having the statements, complete, consistent, and comparable across multiple businesses for all stakeholders.

To be GAAP-compliant, there are some core principles of GAAP that need to be followed:

Principle of Regularity All accounting practices and financial reporting adhere to established rules and regulations.

Principle of Consistency Accounting standards are applied consistently throughout the entire financial reporting process.

Principle of Sincerity Those following GAAP rules should be dedicated to accuracy, impartiality, and transparency.

Principle of Permanence of Methods Reporting must be completed in a consistent and permanent fashion.

Principle of Non-Compensation All aspects of a company’s financial performance is reported without debt compensation.

Principle of Prudence (Conservatism) Reporting is completed without speculation.

Principle of Continuity Asset valuation is completed with the assumption that the organization will continue to operate into the future.

Principle of Periodicity Financial reporting is completed using standard accounting intervals such as monthly, fiscal quarters, or years.

Principle of Materiality Reports are transparent and disclose the organization’s true financial health and position.

Principle of Utmost Good Faith All parties involved in producing financial statements do so with honesty, integrity, and in good faith.

The Financial Standards Accounting Board (FASB) is responsible for maintaining and updating GAAP rules, standards, and procedures for private and public businesses, and nonprofit organizations in the U.S.

What are the GAAP Rules for Accounts Payable?

GAAP compliance helps reduce several common pain points in AP, including a lack of transparency and accountability, inaccurate financial information, and fraudulent payments.

These key areas in particular are addressed in GAAP:

Financial Reporting

GAAP requires publicly held corporations to use accrual accounting and recommends that all businesses do the same. Accrual accounting records revenue when its earned and expenses when they’re incurred.

For AP specifically, that means that accounting staff is required to match revenue and expenses in the same accounting period, which provides a more accurate representation of a company’s financial position.

Classification of Expenses

Under GAAP rules, all expenses should be classified consistently from period to period. Expenses are classified by the nature of the expense and the function of the expense. For instance.

For instance, if purchasing paper for the copier, the nature of the expense would be office supplies, while the function of the expense would be administrative expenses. This classification would remain the same during each subsequent accounting period.

Internal Controls

Internal controls are essential in accounting, especially in Accounts Payable, which has access to company funds. While GAAP rules do not include specific guidelines, it does state the importance of maintaining effective internal controls, which should include:

Segregation of duties Segregation of duties requires that AP tasks such as purchase authorization, receiving goods, invoice approval, and invoice payment be assigned to multiple employees.

Implementing and adhering to document retention policies All AP-related documents, such as purchase orders, invoices, shipping receipts, and payment records should be organized and maintained properly for audit purposes.

Periodic reporting and analysis This includes regular reconciliation of vendor statements and AP account balances, along with investigation into any discrepancies.

Fraud prevention controls There should be established internal controls in place to detect and prevent fraudulent activity, which should include risk management, anti-fraud training, and developing reporting mechanisms to quickly detect potential fraud.

How are Accounts Payable Recorded Under GAAP?

Under GAAP, Accounts Payable are recorded on the double-entry or accrual basis. Under the double-entry system, every financial transaction recorded must include both a debit entry and a credit entry.

For example, if you record rent expense of $1,500, you would record it as a debit to rent expense and a credit to Accounts Payable, which would increase your Accounts Payable account balance. When the rent is paid, you would then debit the Accounts Payable account, which reduces the Accounts Payable account balance, and credit the bank account which the payment was issued from.

Other GAAP requirements for AP include:

Accrual accounting is required under GAAP, which means that you’ll record expenses when they are incurred, not when they’re paid.

Accounts Payable is recorded on the balance sheet as a current liability, since all AP is required to be paid in a relatively short period of time, usually between 30 to 90 days. AP balances are not recorded on an income statement, as they represent a financial obligation to pay, rather than an actual expense.

Disclosure of the complete Accounts Payable balance is required, including trade payables (for core business operations) and non-trade payables such as overhead costs.

Account reconciliation is also required under GAAP, with AP balances regularly reconciled with vendor invoices and supplier statements.

What is the Difference Between IFRS and GAAP?

IFRS and GAAP are the two primary accounting methods used globally. While there are some similarities, the two differ in many ways.

Function

GAAP

IFRS

Organization

GAAP is U.S.-based and uses a rule-oriented approach with specific guidance for various accounting situations

IFRS is a set of global accounting standards created to maintain consistency and transparency in reporting

Structure

Uses specific guidelines, with a specific rule created for a specific situation

Focuses on professional judgement rather than strict rules

Revenue Recognition

Recognizes revenue when earned, but has specific guidelines for each industry

Recognizes revenue when earned, but allows you to apply guidelines across industries

Inventory Valuation

GAAP rules offer multiple inventory valuation methods, including LIFO, FIFO, and weighted average

IFRS supports FIFO and weighted average, but does not allow LIFO

R & D Development

Both research and development are expensed

IFRS splits research from development, expensing the research, but allowing capitalization of development

Impairment Testing

Allows recognition of impairment losses on market-declined assets but prohibits reversal of impairment losses

Allows recognition of impairment losses on market-declined assets, but allows losses to be reversed for all assets but goodwill

Leases

GAAP rules differentiate between operating and finance leases

IFRS treats all leases similarly to GAAP treatment of finance leases

Financial Statements

Income statements must stick to a specific format, while the balance sheet must list non-current assets first

Income statement formats are flexible, while balance sheet requirements allow businesses to list current or non-current assets first

What is the Best Way to Follow GAAP Guidelines in Accounts Payable?

Accounts Payable is one of the most paper-driven areas of the accounting department, with purchase orders, invoices, shipping receipts, and proof of payment all handled manually.

Now, more companies are turning to an AP automation solution like PLANERGY, an automated AP and procurement solution that enhances productivity, reduces data entry errors, and streamlines the entire AP process, making GAAP compliance easier.

In addition, accounts payable automation allows the AP department to:

Eliminate manual data entry and paper-driven workflows

Reduce or eliminate late payments

Increase AP processing speed

Eliminate repetitive invoice processing tasks like data entry, manual three-way matching, and filing of financial records

Instantly spot invoice exceptions and speed investigation

Institute automatic three-way matching and expense categorization

Simplify vendor onboarding, including relevant tax data and payment terms

Better manage cash flow

Provide total expense management, including spend management and complete data transparency

Process accurate financial statements in real time

By upgrading to an automated accounting software application, small businesses can streamline AP workflows, eliminate costly processing delays, and manage spending in real time, while adhering to GAAP rules and regulations.

What’s your goal today?

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")