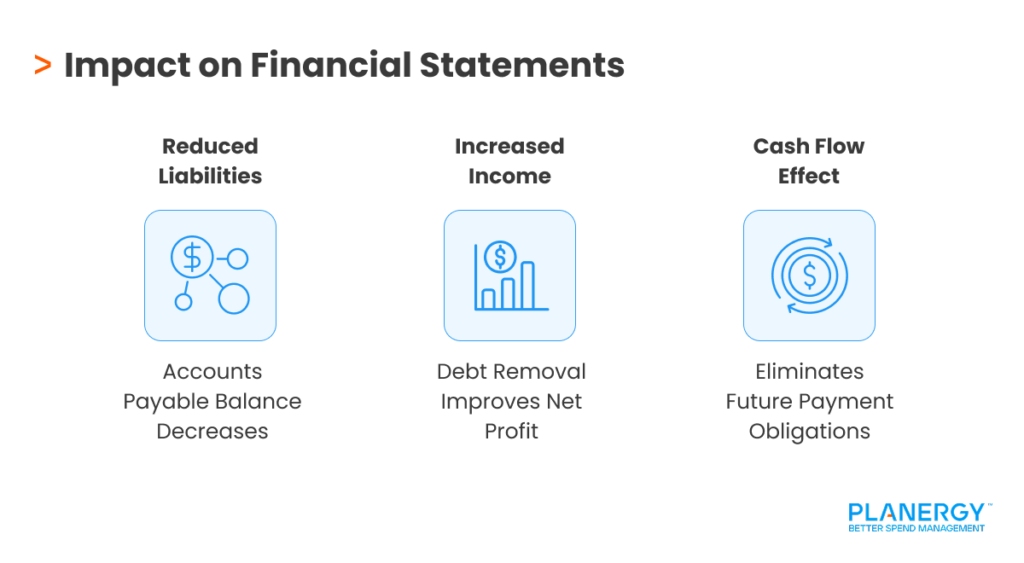

Unlike Accounts Receivable balances, which are often written off as bad debt, Accounts Payable (AP) balances are rarely written off.

However, there are circumstances when writing off AP balances is justified.

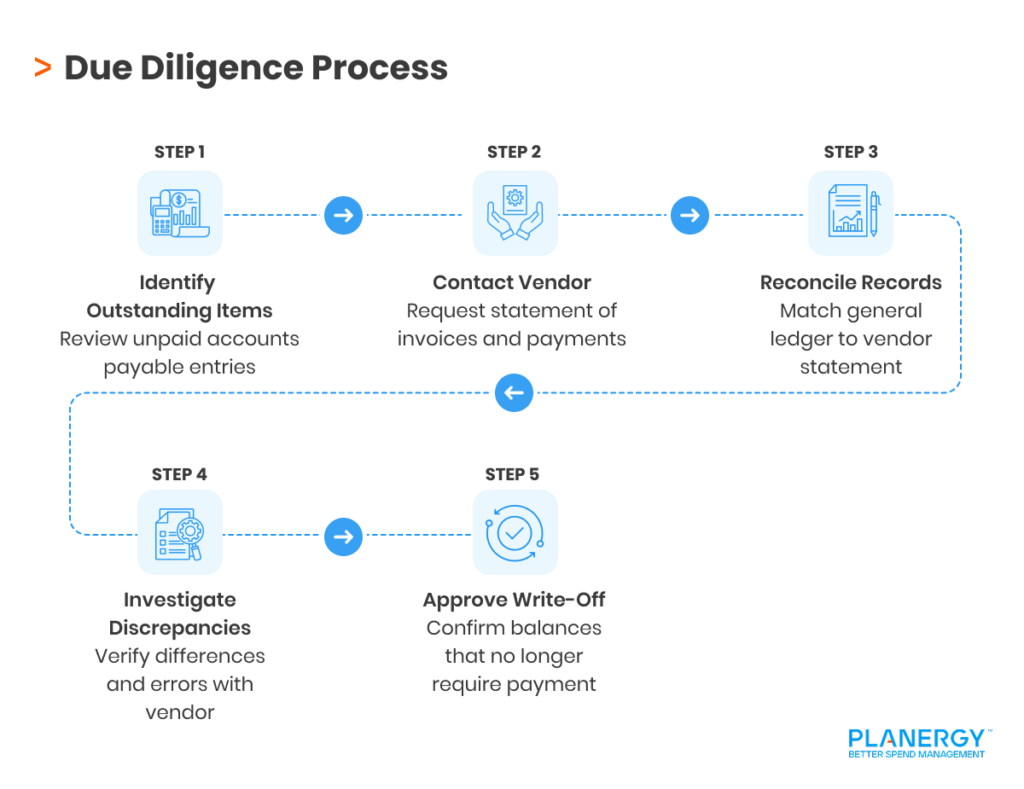

We’ll explore the reasons for writing off Accounts Payable and how it should be done.

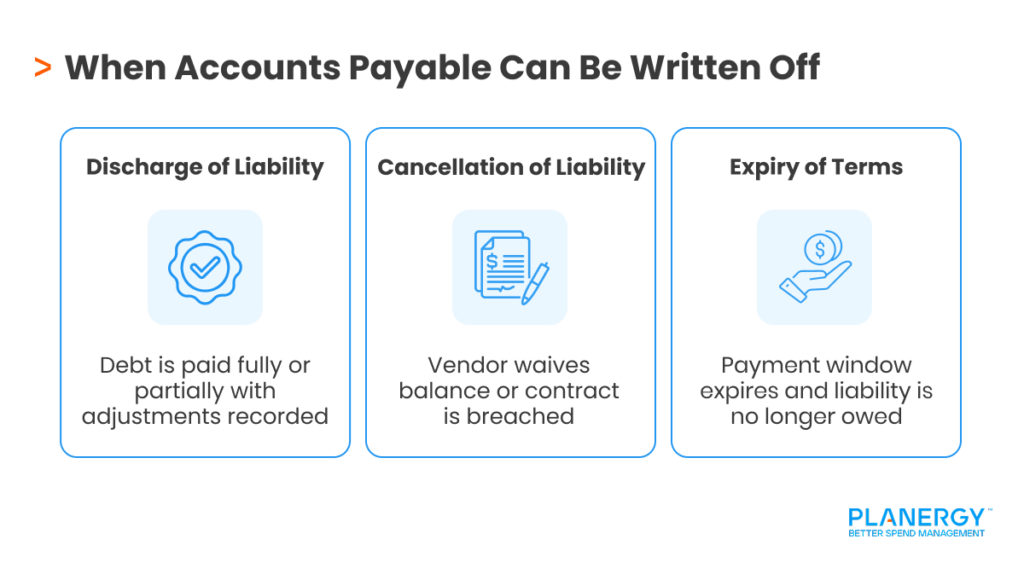

When Can Accounts Payable Be Written Off?

Both the International Financial Reporting Standards (IFRS-9) and Generally Accepted Accounting Principles (GAAP) rules have a list of criteria that must be met before any Account Payable item can be written off.

According to both organizations, Accounts Payable items should only be written off when there is a:

Discharge of Liability

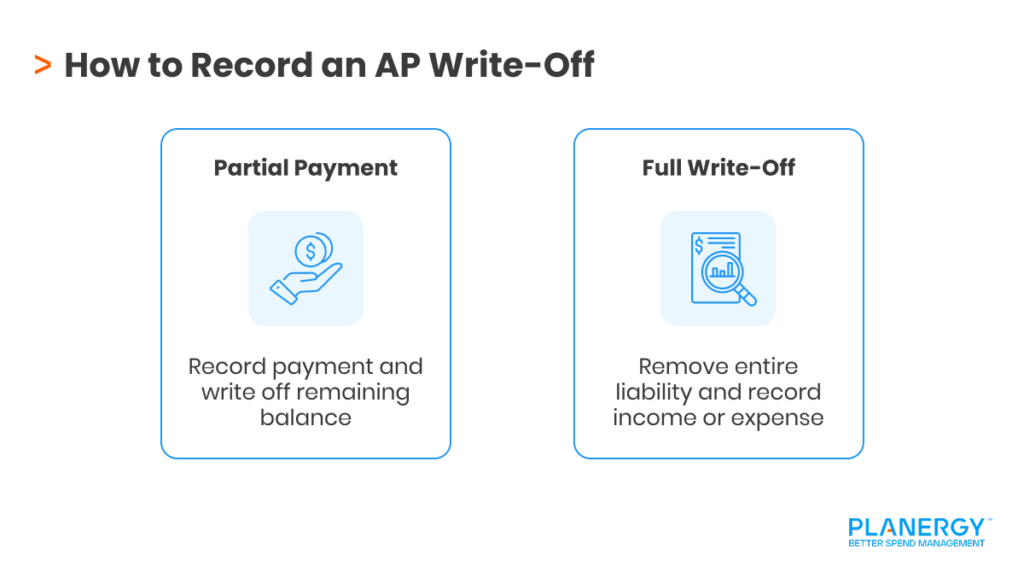

The Accounts Payable item in question has been paid in full, or in part. In turn, the liability account is reduced either by cash payment or an offset in other assets.

In either case, the company is required to recognize the gain or loss. This includes when a discount is offered by the vendor and taken by the purchaser.

Cancellation of Liability

The balance due is waived by the vendor, or the vendor breaches the terms of the contract.

Though rare, AP or trade payable amounts may be canceled either in part or in full. This happens when a vendor/creditor goes out of business, when the balance is waived by the vendor, or if a contract has been breached.

For example, if part of the contract states that a vendor will deliver an item by a certain date and the delivery does not happen, the contract has been breached.

Expiry of Terms

The terms and conditions of the invoice have expired, and the debt is no longer owed. This only applies when a contract is in place that includes a limited timeframe in which the vendor or creditor can claim the balance owed.

Once that term has passed, the balance is no longer owed and can be written off.

")

")

")