We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Whether you’re running a small business start-up or a multi-million-dollar corporation, financial statement accuracy matters. If you’re using cash-basis accounting, you don’t have to worry about accruing expenses, but if you’re using accrual-basis accounting, you’ll need to regularly accrue expenses to ensure that both income and expenses are recorded in the correct accounting period.

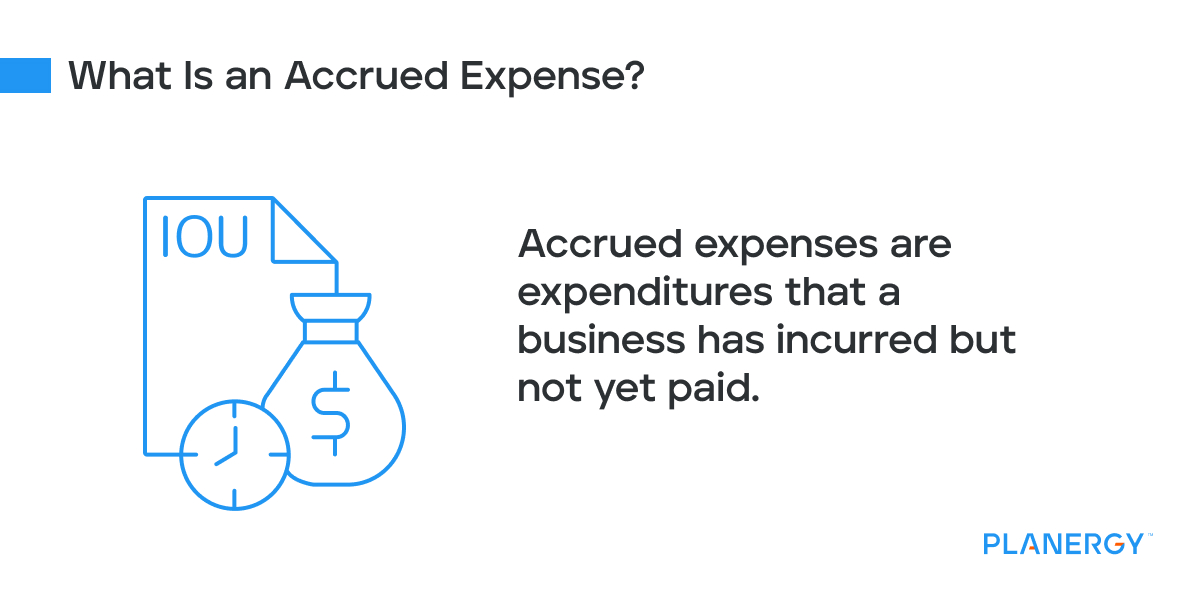

What Is an Accrued Expense?

Accrued expenses are expenditures that a business incurs that have not yet been paid for.

To record those expenses in the period when they occurred, they need to be accrued. As part of the month-end adjusting journal entry process, accrued expenses are necessary to properly account for expenses and to maintain financial statement and general ledger accuracy.

Accrued expenses become necessary when a business purchases goods and services on credit, and the product or service is delivered before the invoice has been received.

If the purchase is completed and an invoice is received in the same month, accruing expenses isn’t necessary, but if you purchase a product and service and an invoice has not yet been received, it becomes necessary to accrue the expense until invoice receipt or payment is issued.

If you’re using cash-basis accounting, there’s no need to post accrued expenses since cash-basis accounting records expenses when money changes hands.

Let’s say you receive a $100 utility bill for March but don’t pay the bill until April. In cash accounting, you would record the expense in April, when it’s paid, not in March, when the expense was incurred.

However, properly accounting for expenses becomes more complicated if you’re using the accrual method of accounting, which requires you to record the expense in the month that it’s incurred, not when the bill is paid.

Referencing that same utility bill, if you don’t receive the utility bill for March until April 1, you would need to accrue the $100 expense in March.

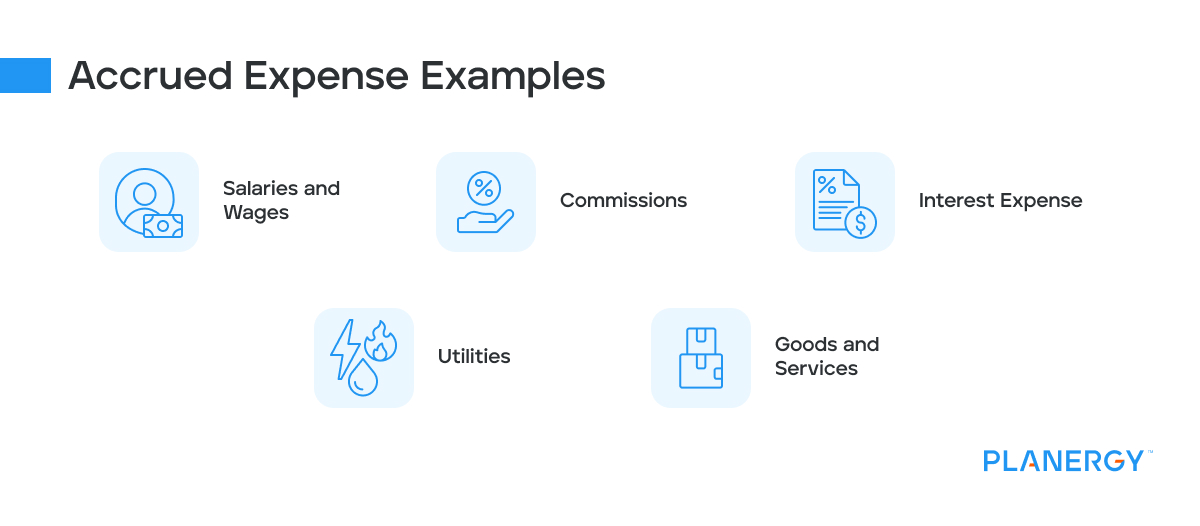

Accrued Expense Examples

Accrued expenses are typically expenses incurred for the month without a vendor or supplier invoice received but can also be expenses that will never have an invoice, such as salaries and wages or interest expenses.

Common expenses that frequently need to be accrued include:

Salaries and Wages

Payroll is a commonly accrued expense, particularly for companies that pay weekly or biweekly payroll. Accruals are often necessary for payroll because staff may typically work at the end of one month but not be paid until the following month.

Commissions

If you commonly pay commissions to salespeople, it’s highly unlikely that you’ll have the total amount of commissions due by the end of the month.

Estimating commissions at month end allows you to accrue the expense, and then later reverse it the following month when you have actual commission numbers and are ready to pay the salespeople what they’re owed.

Interest Expense

If you have a loan or line of credit, you’ll need to accrue interest that has accumulated but has not been paid.

Utilities

If your utility bill typically doesn’t arrive until the first of the month, you’ll need to accrue utility expenses for the current month.

As a general guideline, any expense incurred during the current month that has not been accounted for by the end of the accounting period should be accrued.

Where Are Accrued Expenses on a Balance Sheet?

Accrued expenses, which are sometimes referred to as accrued liabilities, are a liability account and should always be recorded on your balance sheet under current liabilities.

Accrued expenses are considered current liabilities because the account balance represents the amount that a business is currently obligated to pay its vendors and suppliers in a relatively short period.

Because accrued expenses are a liability, they should always be recorded as a credit, which works to increase the balance of the account.

When the accrual is reversed the following month, the accrued expenses account will be debited, which will reduce the balance in the account.

A typical liabilities section of a balance sheet may look like this:

Current Liabilities:

Accounts Payable

Accrued Expenses

Accrued Payroll

Tax Liabilities

Short-Term Debt

While some companies may separate accrued expenses and accrued payroll expenses, whatever method you use for your business, the accrued expenses balance will always be displayed on your company’s balance sheet.

What Is the Difference Between Accrued Expenses and Accounts Payable?

Though both are liabilities and represent money that a business is obligated to pay to a vendor or supplier, an accrued expense is an expense that a company knows must be paid but has not yet received an invoice for.

Accounts payable is the amount currently owed a vendor or supplier that has been recorded but not yet paid.

Using the utility accrual expense example cited earlier, if the utility bill had been received in March, the utility expense of $100 would have been recorded in the accounts payable account since the bill had been received.

But if the bill had not been received until the following month, the accounting department would accrue the expense for March.

In many cases, accrued expenses are estimates of how much you expect a bill to be. For example, if January and February utility bills averaged $95, it would make sense to accrue utility expenses for $95.

Once the bill for $100 is received in April, you would simply reverse the accrued expense entry and enter the actual amount as an accounts payable item.

What Is the Difference Between Accrued Expenses and Prepaid Expenses?

The major difference between accrued expenses and prepaid expenses rests on when payment is made. Accrued expenses are expenses incurred that have not yet been paid. An accrued expense is always recorded as a liability on your balance sheet.

Prepaid expenses represent payments that have been made in advance of expenses incurred. An insurance policy that is paid for the upcoming year is the perfect example of a prepaid expense.

And unlike an accrued expense, a prepaid expense is always recorded as an asset on your balance sheet.

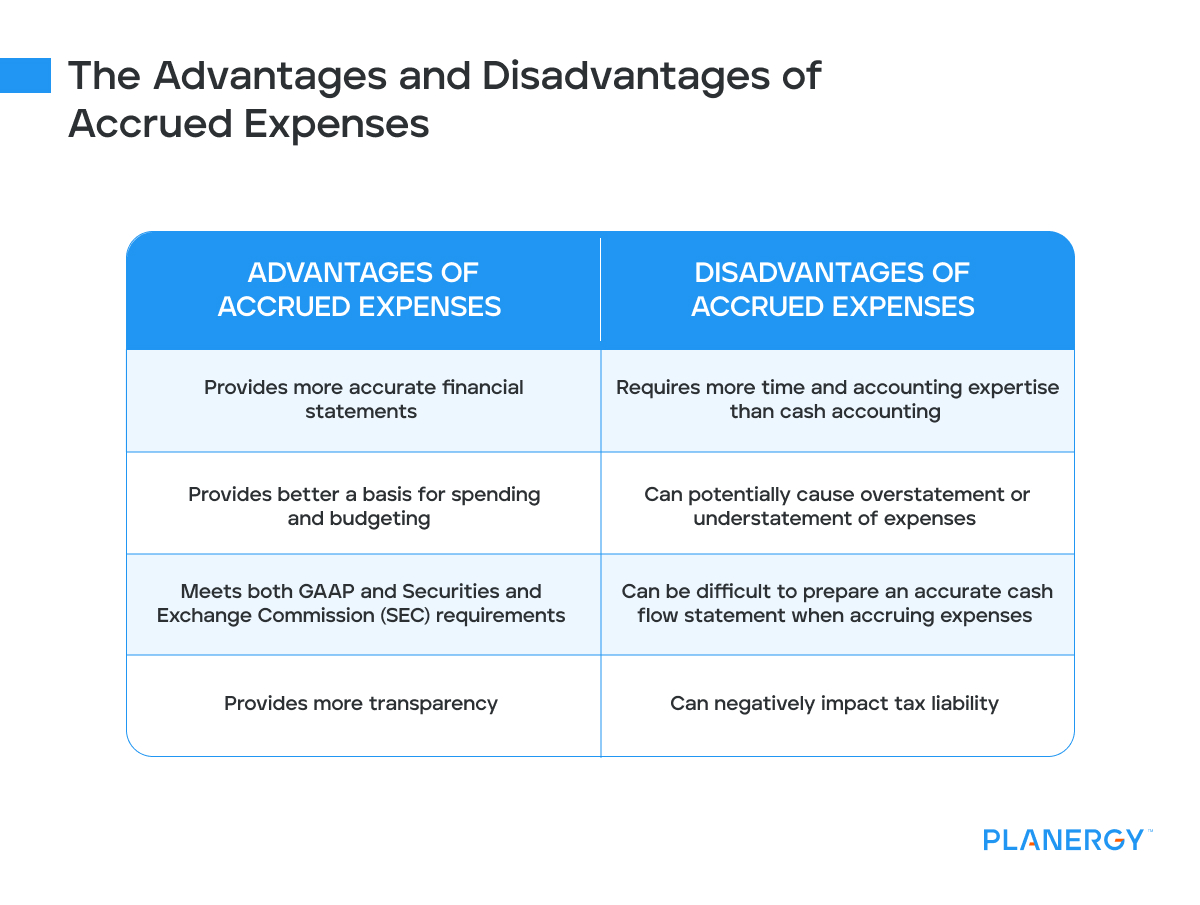

What Are the Pros and Cons of Accrued Expenses?

Accruing expenses makes your financial statements more accurate, but requires more in-depth accounting knowledge than cash accounting does. There are other advantages and disadvantages to accrued expenses that need to be considered.

Advantages of Accrued Expenses

Disadvantages of Accrued Expenses

Provides more accurate financial statements

Requires more time and accounting expertise than cash accounting

Provides better a basis for spending and budgeting

Can potentially cause overstatement or understatement of expenses

Meets both GAAP and Securities and Exchange Commission requirements

Can be difficult to prepare an accurate cash flow statement when accruing expenses

Provides more transparency

Can negatively impact tax liability

But even with the disadvantages, the results are worth the extra work, since accruing expenses provides a much clearer picture of your finances.

What Is the Journal Entry for Accrued Expenses?

There are always two sets of journal entries required when recording accrued expenses; the initial accrual for the current month, and the reversal of the accrual, which is completed the following month, or whenever an invoice is received or an expense paid.

The most difficult part of recording accrued expenses is remembering to actually complete the journal entry and then reverse it on a later date when an invoice is received or payment is made.

For instance, you order business cards for the sales department for a total of $1,700. The cards arrive the last week in April, but you have not yet received an invoice.

Under the accrual basis accounting rules, you will need to accrue the $1,700 expense for April, since that is the month that the expense was incurred.

The journal entry to do that is:

Date

Account

Debit

Credit

4-30-2023

Advertising Expense

$1,700

4-30-2023

Accrued Expenses

$1,700

When you receive the invoice on May 6, you will need to reverse the accrual, using the following journal entry.

Date

Account

Debit

Credit

4-30-2023

Accrued Expenses

$1,700

4-30-2023

Advertising Expense

$1,700

Now that the accrual is reversed, you can enter and pay the invoice through accounts payable.

What Are Important Things To Consider About Accrued Expenses?

There are repercussions if accrued expenses are not recorded properly. Consider your April financial statements. If you never accrue the advertising expense in April, the expense will be recorded in May instead.

This means that your advertising expense will be understated in April and overstated in May. And if you do record the accrued expense, but forget to reverse it once the invoice is received or a payment is made, your advertising expense will be overstated in May.

If you’re using an automated accounting software application, there is usually an option to have accruals automatically reverse.

But for businesses recording accruals manually, a good rule of thumb is to prepare the journal entry for the following month ahead of time, recording it once month-end processing is complete.

What Does It Mean When the Accrued Expenses Account Balance Is Negative?

If your accrued expenses are recorded properly, the balance should always be a credit balance, since it’s a liability.

If your accrued expenses account balance is a debit balance or a negative balance, that usually means that you’ve reversed the accrued expense journal entry from the previous month twice.

It can also mean that you never completed the original accrual entry but recorded only the reversal instead.

For example, you record a journal entry for $15,000 in accrued expenses in April. At the beginning of May, you reverse the accrual entry.

Unfortunately, your accounting clerk also reverses the accrued expense entry from April as well, leaving you with a $15,000 debit or negative balance in the accrued expenses account.

To correct the duplication, you’ll need to reverse the second journal entry that was completed in error. Once that’s completed, your accrued expenses account balance should be accurate.

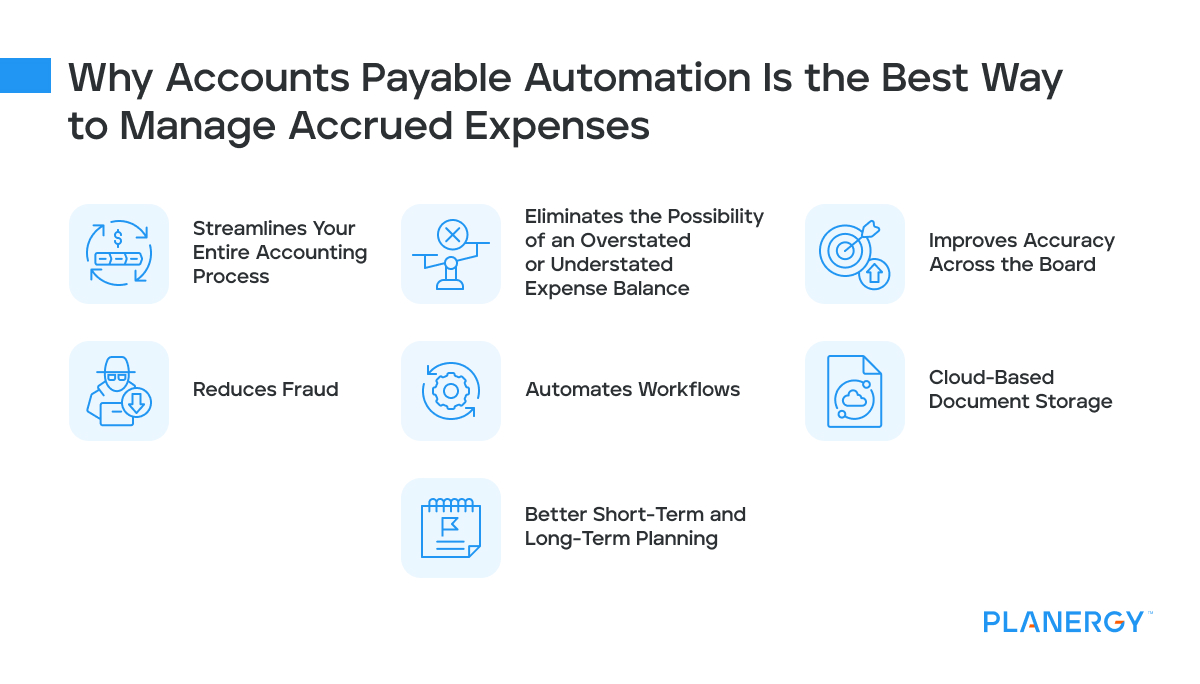

What Is the Best Way To Manage Your Accrued Expenses?

Accounts payable automation is the single best way to manage accrued expenses and all of your accounts payable tasks.

This eliminates the possibility of an overstated or understated expense balance, that will result in an inaccurate financial position for that reporting period.

In addition, AP automation offers the following benefits, including:

Improved Accuracy Across the Board

Once you eliminate manual processes, accuracy increases. No more transposed numbers, duplicate payments, or inaccurate accruals, which means more accurate financial reports available in real-time.

Reduced Fraud

Because disbursements flow directly through AP, the department is ripe for fraud. Using AP automation can effectively reduce, or even eliminate fraud.

Automated Workflows

Instead of AP staff spending hours (or days) matching invoices with purchase orders and delivery receipts, the entire process is automated from beginning to end.

In addition, custom workflows direct invoices to the correct approvers electronically, eliminating costly delays and lost invoices.

Cloud-based Document Storage

Replace paper with digitized documents and achieve an paperless accounts payable process. AP automation includes cloud-based document storage, the perfect solution for those tired of dealing with piles of paper, lost documents, and time-consuming filing.

Better Short-term and Long-term Planning

Instead of spending valuable time ensuring that financial month-end and year-end financial statements are accurate, making the move to AP automation provides you with the resources you need to better manage your business now, and for the foreseeable future.

For companies still using manual processes to manage accounting, accruing expenses can be overwhelming.

Accrual accounting can be particularly challenging if you’ve recently switched from cash accounting and can leave those less experienced in bookkeeping or accounting confused.

Forward-thinking business owners know that making the switch to using automated accounts payable software can streamline the entire workflow process, eliminate processing delays, and help ensure that accrued expenses are an accurate reflection of their business’s financial health.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")