We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Year-end accounting requires a full review of financial records, reconciliations, adjustments, and final financial statements, regardless of whether you use a fiscal or calendar year.

Preparation is critical—checklists, timelines, and task ownership help reduce stress, avoid errors, and keep the process on track.

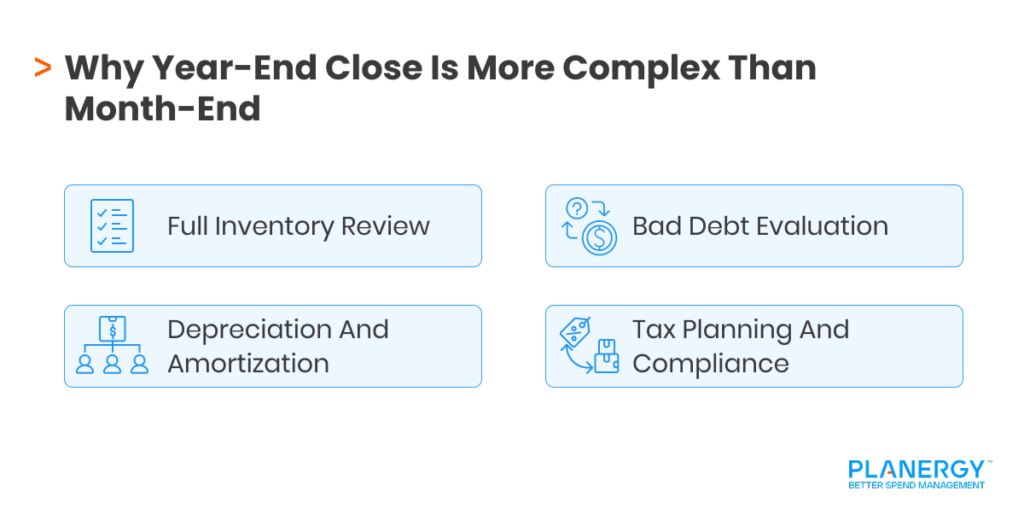

Key year-end tasks include reconciling bank accounts, inventory, AP/AR, accruals, payroll, and fixed assets, along with closing temporary accounts.

Accrual accounting provides a more accurate picture of financial performance by recording revenue when earned and expenses when incurred, not when cash changes hands.

Accurate year-end financials support tax compliance, audits, forecasting, budgeting, and informed business decisions for the year ahead.

Using automated accounting tools simplifies reconciliation, improves accuracy, maintains audit trails, and helps finance teams close the year more efficiently.

The accounting process is not stress-free, but the year-end closing process can create a whole new set of stressors for small business owners.

Fortunately, it doesn’t have to be that way. Having the right tools and preparation can make all the difference when it comes to surviving the all-important year-end closing.

What Year-End Closing Means for Accounting and Finance Teams?

Every business operates on either a fiscal year or a calendar year.

For example, some businesses may opt to operate on a fiscal year, which means that if the beginning of your fiscal year is November 1, your year-end would be October 31 of the following year.

Other businesses prefer to follow a calendar year, with year-end on December 31 of each year. It doesn’t matter whether you use a fiscal year or calendar year for your business, you’ll still need to be prepared to close out the year.

For accounting and financial team members, this means undertaking a complete review and reconciliation of all appropriate accounts, preparing adjusting entries when needed, and preparing year-end financial statements.

How Do You Prepare for Year-End Financial Reporting?

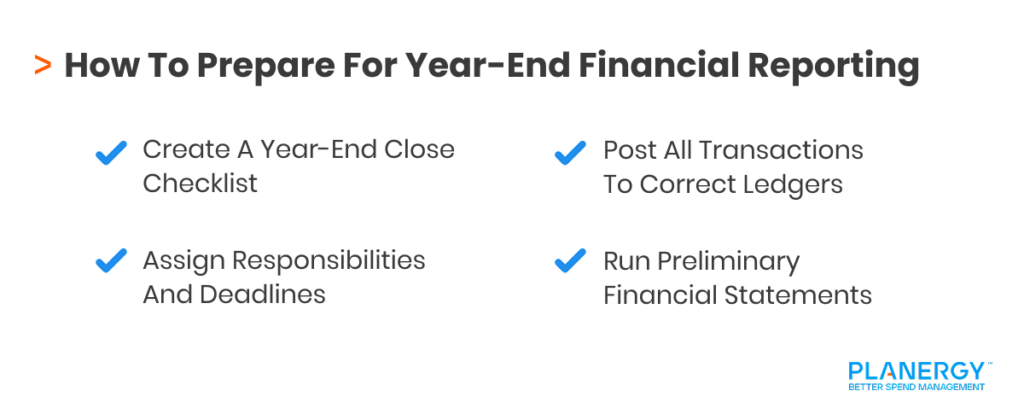

One of the best things you can do in preparation for year-end is to create a year-end accounting checklist of items that need to be completed, starting with a schedule of steps needed to complete the closing process.

When preparing the schedule, you can assign individual steps to team members along with deadlines. This will help expedite the closing process while ensuring that no critical steps are skipped.

Before beginning the year-end closing process, you’ll want to make sure that all financial transactions have been posted to the correct ledgers.

You’ll also need to run a preliminary set of financial statements that can be used during the review and reconciliation process.

How Do I Prepare My Small Business for Year-End?

The best way to prepare for year-end is to give your staff the time and resources needed to complete all the required steps.

If you’re still using a manual accounting system, consider investing in accounting software that can automate the year-end closing process.

Using an automated system eliminates the need to manually enter transactions, makes it easier to see issues or discrepancies, and keeps your data in a centralized location with a complete audit trail.

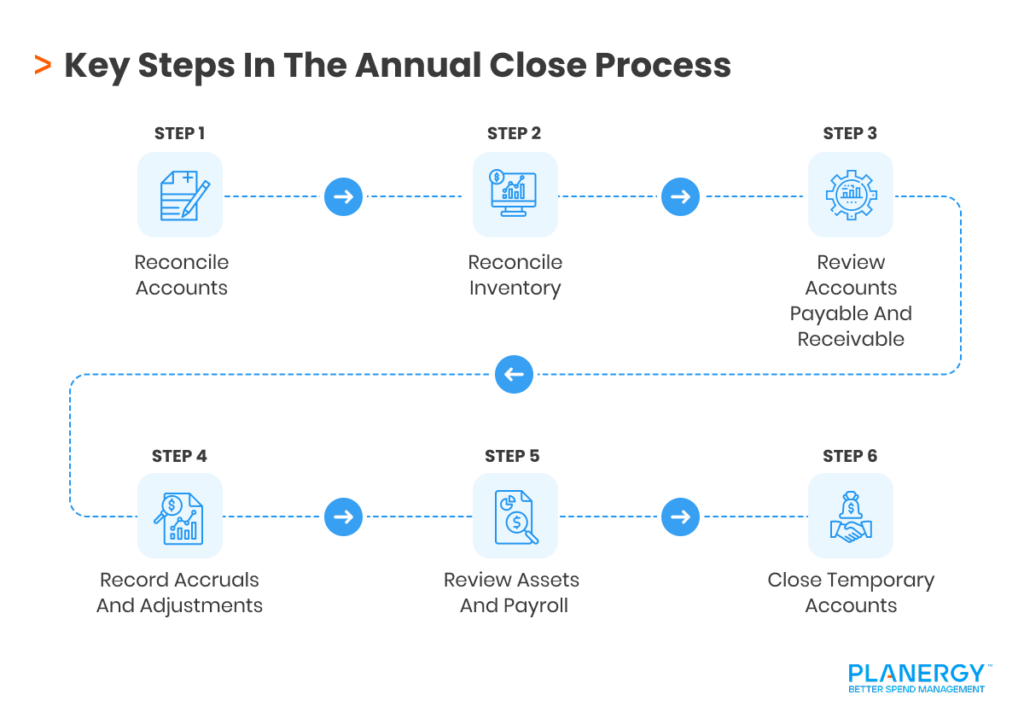

Steps for the Annual Close Process

There are numerous steps that you’ll need to complete during the annual closing process.

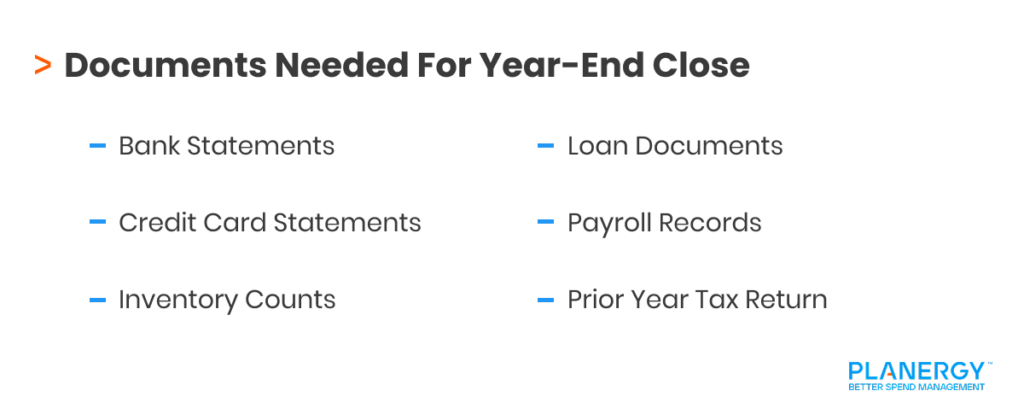

Gather the necessary financial documents

To begin the closing process, you’ll need to have the following financial records handy:

Bank statements

Credit card statements

Inventory counts

Loan documents

Payroll journal

The previous year’s tax return

Reconcile account balances

Before you can close the year, you’ll need to reconcile your account balances against your bank statement and credit card statement.

This process helps identify missing transactions, credit card expenses not recorded, outstanding checks, and bank account fees not yet posted to the general ledger.

Reconcile inventory

A physical count of your inventory for year-end helps ensure that the quantities on hand match the value of the inventory recorded in the general ledger.

Year-end is also the time to make adjustments for inventory that is obsolete, damaged or is otherwise unsellable.

Review accounts payable and accounts receivable totals

Ending accounts payable and accounts receivable balances should be reviewed for accuracy and adjustments made when needed.

For instance, if your accounts payable balance still includes an outstanding invoice that you know has been paid, you’ll need to adjust the ending balance to reflect the payment.

For accounts receivable, you’ll need to review open balances for accuracy, paying close attention to past-due accounts to determine whether they’re still collectible or if you’ll need to record them as bad debt write-offs.

Review accruals and adjustments

One of the most important steps in the year-end closing process is making sure that all the necessary accruals have been recorded, including frequently accrued expenses such as payroll and utilities.

You’ll also want to accrue expenses or revenue that has been delivered or earned but not yet recorded. During the review process, you’ll also want to review and reverse previous accruals if necessary.

Any adjustments needed as a result of the reconciliation process will need to be recorded at this time.

For example, if you have bank fees of $35 in December, you’ll need to make sure that the fee is also recorded in the general ledger, or your ending general ledger balance will be overstated.

Review assets

Review all of your fixed assets listed on the balance sheet for accuracy. This includes reviewing the current value stated for accuracy and calculating depreciation and amortization expenses.

If you’ve been calculating depreciation every month, you’ll only have to record depreciation for the last accounting period, but if not, you’ll need to calculate and record depreciation and amortization expenses for the entire year.

Part of the asset review should also include accounting for any assets that have been sold but the sale not recorded.

Review payroll

Another area that needs to be reviewed before year-end is payroll. The payroll review should include verification that accrued payroll entries have been recorded and later reversed.

The payroll review should also include a review of the appropriate general ledger accounts to verify that all payroll and related expenses have been properly recorded.

Review and close temporary accounts

If you’re still using a manual accounting system, you’ll have to close all of your temporary accounts such as your expense and revenue accounts to an income summary account.

You’ll also have to transfer net income or loss to a retained earnings account. If you’re using an automated accounting software application, this process is completed for you.

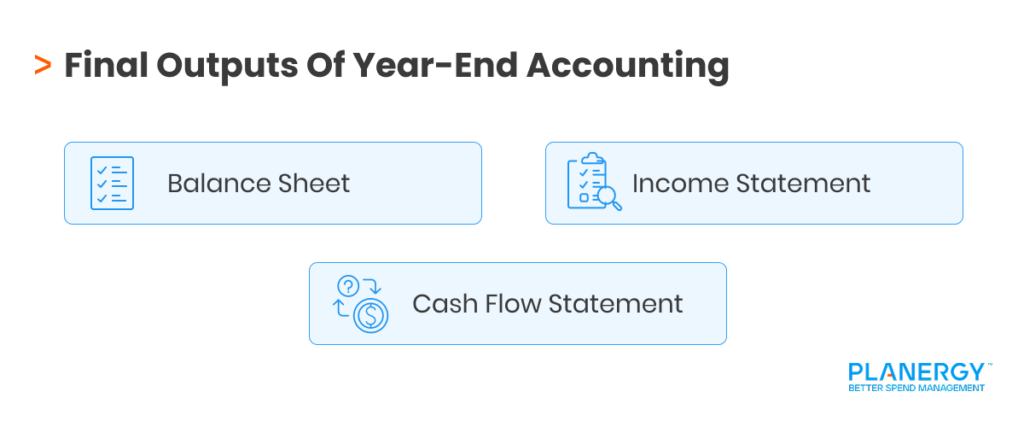

Prepare final financial statements

When all of the necessary reconciliations and resulting adjustments have been made, you can run your year-end financial statements. This includes the following reports:

Balance sheet

Income statement

Cash flow statement

There may be other financial statements you wish to run, but these are the main three that you’ll need to complete the year-end process.

Complete the tax planning process

Tax planning is essential to the year-end close. This includes:

Reviewing tax-related documents for accuracy

Preparing the necessary tax forms

Reconciling your tax liability with your general ledger

Gathering this information at year-end expedites the tax filing process for businesses while also avoiding penalties and interest.

Once you complete these steps, you can move on to internal or external audit preparation by reviewing current processes including verifying that your internal processes include an adequate audit trail.

You’ll also want to use your year-end close to begin planning and budgeting for the upcoming year.

You can use the results to more accurately forecast upcoming expenses and revenue, while also setting more realistic financial goals for your business.

What Accounts Are on a Year-End Statement?

The following accounts are found on year-end statements:

Assets, liabilities, and equity accounts which are found on a balance sheet

Income, expenses, revenues, costs, and profit and loss, which are found on an income statement or profit and loss statement (P&L)

Cash flow from operations, investments, and financing, which are on the cash flow statement

During the year-end closing process, all of these accounts should be reviewed for accuracy, and adjustments made as needed.

How Accrual Accounting Helps Your Business at Year-End?

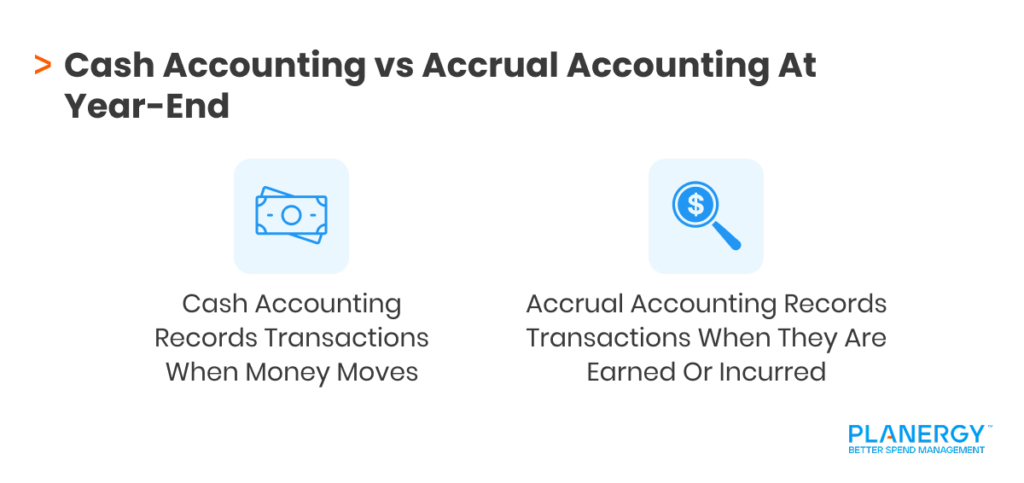

When setting up your business for the first time, you have the option to choose from cash or accrual accounting.

Cash accounting records revenue when it’s received and expenses when it is paid.

For example, a company using the cash accounting method would record a sale only after the customer has paid their invoice, not when the invoice was issued.

Using cash accounting, you would also record an expense when it’s paid, not when it’s incurred.

Accrual accounting records revenue when it’s earned (when a sale is made) and expenses when they are incurred.

For example, if your business uses the accrual accounting method, you would record a sale when it happens, not when the customer pays you.

You would also record an expense such as goods and services, when the item or service is purchased, not when you pay the invoice.

While cash accounting is an acceptable method for very small businesses with limited transactions, if you have employees, manufacture and sell products, or sell to customers on credit, you will be required to use accrual accounting.

Using accrual accounting provides many benefits to businesses, offering a path to success that may not be available if you’re using cash accounting.

For instance, using accrual accounting allows you to sell to your customers on credit, which can expand your customer base.

Using accrual accounting also provides creditors, loan officers, and potential investors with the financial data they require to invest in, or loan funds for business growth and expansion.

There are other benefits for your business if you use accrual accounting, including:

A More Realistic View of Your Finances in Real-Time

Accrual accounting factors in expenses that you owe that haven’t been paid and revenues earned that haven’t been received. This provides a more accurate view of your business finances for all the necessary stakeholders.

A More Accurate Way To Measure Profitability

It’s difficult to measure how profitable your business is if your financial statements only show funds paid or received.

By using accrual accounting, you can see exactly how much you owe to vendors and suppliers and how much is owed to you from your customers. This information in turn can be used to accurately measure profitability and if there’s a need for improvement.

Tax Law Compliance

Various tax agencies have requirements that businesses use accrual accounting once they hit a revenue threshold. But you don’t have to wait until you’re earning tens of millions of dollars to use accrual accounting for your business.

MoreEffectiveForecastingandDecision–Making

Using accrual accounting provides you with the financial information you need to make more accurate budgets and forecasts. It also provides the information necessary to make crucial business decisions such as investing and expansion.

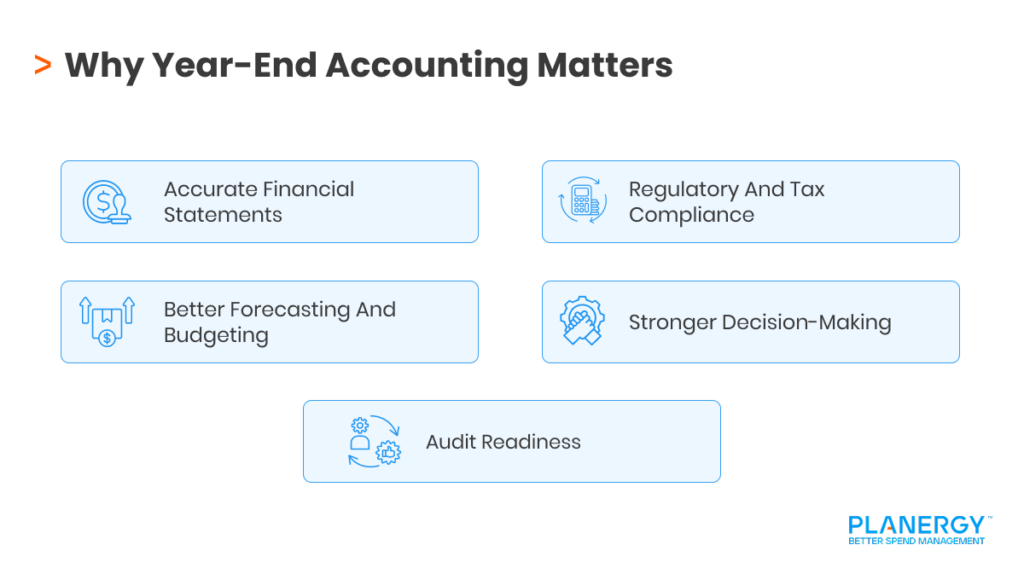

Why Year-End Accounting Matters

Whether you’re the CFO of a Fortune 500 company or managing a small, one-person business, year-end accounting matters.

Year-end closing helps maintain the accuracy of financial statements while providing an in-depth look at the financial health of a business.

The year-end process also provides the basis for more accurate and in-depth decision-making while identifying trends and locating potential trouble spots.

Year-end close also provides a blueprint for creating an accurate budget or forecast for the next year.

Year-end accounting also provides company stakeholders such as investors with a clear look at company performance while ensuring that the business complies with rules and regulations.

Accurate year-end financial statements also provide the information needed to file and pay taxes, sets the stage for both internal and external audits, and provides a clear basis for resource allocation and cost-cutting measures when needed.

The year-end process can be complex and time-consuming, but the right tools make it manageable. With them, you can quickly review transactions, reconcile accounts, and produce accurate financial statements to start the new year strong.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")