We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Inter-company accounting ensures accurate recording of transactions between entities within the same organization, preventing misstatements in consolidated financial statements.

Every inter-company transaction must be recorded by both parties to maintain balance and avoid discrepancies during reconciliation.

Common transaction types include asset transfers, loans, sales, cost allocations, and management fees, all of which require careful tracking and elimination during consolidation.

Centralized systems, standardized policies, and automation are key to improving visibility, reducing errors, and streamlining inter-company processes.

Business owners, CFOs, and accountants are all familiar with key accounting processes, including the standards used for posting accounting transactions.

Yet those standards can become somewhat muddled when dealing with multiple entities, or multinational companies that operate in several jurisdictions.

Anytime a company has multiple locations or multiple entities operating under a parent company, inter-company accounting processes should be used.

Though some inter-company transactions are simple, they can quickly become complicated if not managed properly.

What Is Inter-company Accounting?

Inter-company accounting refers to the proper recording of internal transactions that occur between branches, subsidiaries, or other legal entities of a parent company.

While inter-company accounting is more frequently used in large corporations, small businesses may also need to employ inter-company accounting for certain financial activities.

For example, if a business opens a second location, inter-company accounting can track internal transactions between locations, such as an employee working at the second location to fill in for another employee.

What Is an Inter-company Transaction?

An inter-company transaction is a financial transaction that is recorded as a journal entry by both parties.

For example, ABC Electrical sells electrical equipment. The company has five different entities and often shares inventory between locations.

For inventory levels to remain accurate at both locations, the providing location must record an adjustment that lowers its inventory. The receiving location must record the incoming inventory to reflect a corresponding increase.

In another example, if a parent company pays the expenses of a subsidiary company, both the parent company and the subsidiary will need to record the payment.

Many companies use a due to/due from account for recording transactions. When it comes time to reconcile between entities, the due to/due from accounts should always be in balance with the other entities.

When financial consolidation is complete, these entries are eliminated by offsetting each other. If an inter-company transaction is recorded in only one company’s books, revenues or expenses may be incorrectly stated, resulting in inaccurate financial statements.

What Are the Basics of Inter-company Accounting?

The purpose of inter-company accounting is to record a transaction that takes place between the parent company and a subsidiary or between two subsidiaries.

There are three main types of inter-company transactions that businesses may need to track. Recording all of these accurately is important for a variety of reasons including the following:

It eliminates double recording of activity that may take place between entities.

It provides accurate totals for tax regulations.

It is required for compliance with Generally Accepted Accounting Principles (GAAP) and Securities and Exchange Commission (SEC) rules for financial reporting.

What Are the Challenges of Inter-company Accounting?

Though necessary, inter-company accounting is not without challenges. Challenges vary from business to business and can include the following:

Transaction Matching

Matching transactions can be complicated if a transaction is not handled correctly at both ends. For example, if the parent company records a loan and the subsidiary company does not, it will be impossible to reconcile the inter-company accounts.

Disparate Accounting Systems

This is a common issue between parent companies and subsidiaries. A lack of uniformity between accounting software and the inability to integrate systems properly leads to manual reconciliation, which is time-consuming and error prone.

Lack of Visibility

All parties concerned should have access to inter-company transactions. Using a centralized system that provides access to all parties helps ensure that transactions are recorded in good time and accurately while eliminating double-counting of revenue and expenses.

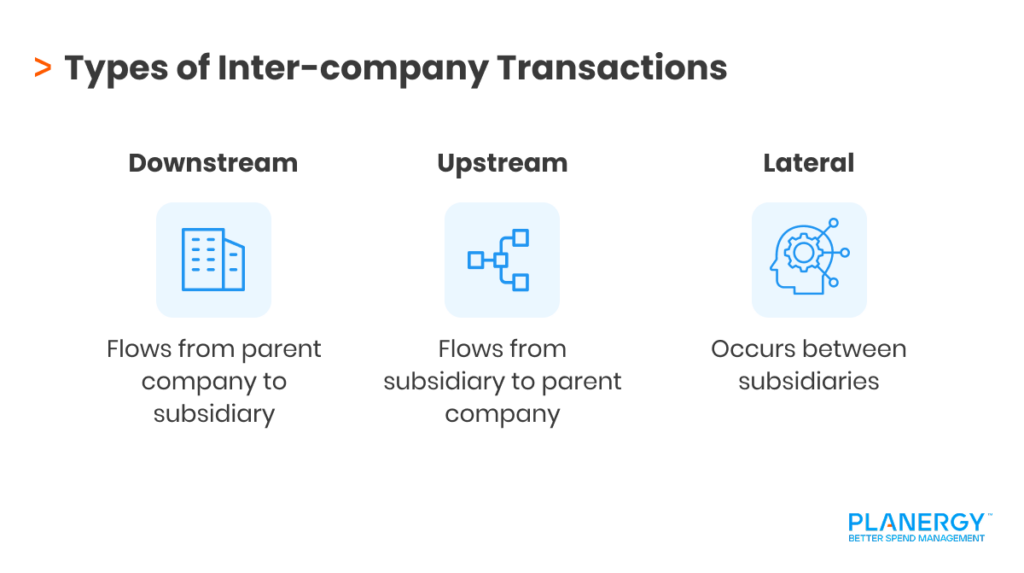

What Are the Three Main Types of Inter-company Transactions?

1. Downstream

Downstream transactions refer to any inter-company activity that flows from a parent company to a subsidiary or branch, such as providing a loan or selling assets to a subsidiary.

The parent company is responsible for tracking and recording downstream transactions.

If the parent company provides a loan to a subsidiary, that is considered a downstream transaction.

2. Upstream

Upstream transactions refer to any inter-company transactions that flow from the subsidiary or branch to the parent company.

If a branch office sends one of its employees to work at the home office, that is considered an upstream transaction.

3. Lateral

Lateral inter-company transactions take place between two subsidiaries and do not involve the parent company.

If one location provides additional inventory to a second location, that is considered a lateral transaction.

What Is an Inter-company Transactions List?

An inter-company transactions list is a list of all the inter-company transactions that have been recorded during an accounting period.

The list should include the day the transaction was recorded, the amount of the transaction, and the account where it was recorded.

For instance, if a parent company loans a subsidiary $10,000 on December 15, the transactions list will include the date of the loan, the amount of the loan, and the accounts(s) that the transaction was posted to.

Running an inter-company transactions list is a helpful tool in the account reconciliation process.

What Types of Inter-company Transactions Should Companies Record?

Any time a transaction takes place between a parent company and a subsidiary or two subsidiaries, it has to be recorded. The types of transactions normally recorded include:

Asset Transfers

Any time that an asset such as equipment, land, or buildings is moved between subsidiaries should be recorded as an inter-company transaction.

For example, if a parent company moves a company car to a subsidiary, that transaction will need to be properly recorded.

Loans

If the parent company provides a loan to a subsidiary, it must be recorded as an inter-company transaction.

Sales of Goods

If a parent company or a subsidiary sells inventory or other goods to another subsidiary, it must be recorded as an inter-company transaction.

Cost Allocations

Cost allocations involve the distribution of expenses between the parent company and its subsidiaries, or between two subsidiaries.

For instance, if the parent company pays the rent for all subsidiaries in a single payment, the rent expense for each subsidiary location will have to be recorded as an inter-company transaction.

Royalties

Royalty payments made to the parent company from a subsidiary for the use of intellectual property will need to be recorded as an inter-company transaction.

Management Fees

Management fees charged by the parent company to its subsidiaries should be recorded as an inter-company transaction.

For example, a real estate company that owns several properties may charge each property a monthly management fee, which will need to be accounted for each month.

Employee Transfers

Any time an employee works at another location, the cost will need to be recorded as an inter-company transaction.

For example, if the parent company sends an administrative employee to a subsidiary to fill in for a week, the salary for that employee will need to be recorded.

The Three Types of Inter-company Eliminations and How They Are Processed

According to Wolters Kluwer, there are three types of inter-company eliminations.

Inter-company Debt eliminates loans that are made between subsidiaries.

Inter-company Revenue and Expenses eliminate sales between subsidiaries.

Inter-company Stock Ownership eliminates the parent company’s interest in its subsidiaries.

Eliminating inter-company transactions is a process that is completed when creating consolidated financial statements.

The best way to process these eliminations is to use a centralized Enterprise Resource Planning (ERP) system that can flag inter-company transactions that will need to be eliminated.

Steps to Streamline Your Inter-company Process

There are a variety of things you can do to streamline the entire inter-company practice. Some essential steps are listed here:

`

Create Standardized Global Policies Across Your Organization

This includes the standardization of data management, including creating a global chart of accounts that can be utilized during the inter-company posting process.

These global policies should also include integrated transact level pricing and analytics, including processing inter-company transactions using ‘arm’s length pricing,’ which is using the same pricing for inter-company transactions as for an unrelated party.

Policies for companies dealing with foreign exchange and currency will also have to be clearly stated so that the accounting department uses the correct guidelines when posting foreign transactions and creating accurate financial statements.

Develop a Master Data Management Program to Oversee the Execution of Policies

Once the policies have been created, developing a master data management program can help integrate transactions across multiple ERP systems if necessary.

A data management program may include creating an accounting hub for central processing of all accounting transactions or the use of automation to perform routine tasks such as transaction routing, invoice productions, and three-way matching.

Organize a Group of Experts

For larger companies that routinely process complex inter-company transactions, organize a group of experts in areas such as finance, tax, IT, and treasury.

This will help ensure that all policies created for inter-company transactions follow best practices and that required standards are met.

Create a Usable Cash Management Strategy to Net and Settle Transactions

If your company routinely deals with foreign currency, you may want to consider implementing a netting program that nets each entity’s Accounts Payable total against its Accounts Receivable total to determine the net settlement amount necessary.

The netting process provides consistency when using exchange rates while reducing bank fees. The netting process also provides better cash management opportunities for businesses when managing both expenses and revenue from multiple sources.

Settle Inter-company Accounts Monthly

Reconciling and setting inter-company account balances monthly makes it easy to keep your financial statements accurate.

If accounts are left to accumulate balances over several months, it can lead to a more complicated inter-company reconciliation process and an increase in discrepancies.

As a reminder, the financial close process should always include inter-company account reconciliation.

Use Automation to Match Transactions

If your business regularly processes inter-company transactions, having the proper technology in place can save significant staff time, improve financial statement accuracy, and ensure that transactions are matched and processed properly.

In a perfect world, each entity would use the same ERP software system, eliminating the need to manually match transactions from multiple systems.

If this is not possible, using a software application designed to match transactions from multiple systems can save a significant amount of time and improve accuracy.

Conclusion

Whether you’re a small business with multiple locations or a multi-national corporation conducting business globally, tracking your inter-company transactions is a must.

Making the decision to centralize your accounting software system across all entities is the best way to reduce errors and ensure consolidated financial statements are always accurate and available

What’s your goal today?

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

`

`