We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Running a successful business means keeping track of your financial obligations. That’s why preparing balance sheet entries is so important.

If you’re using double-entry accounting, your balance sheet provides you with detailed information on assets and liabilities, including accounts payable.

But what is the relationship between a balance sheet and accounts payable?

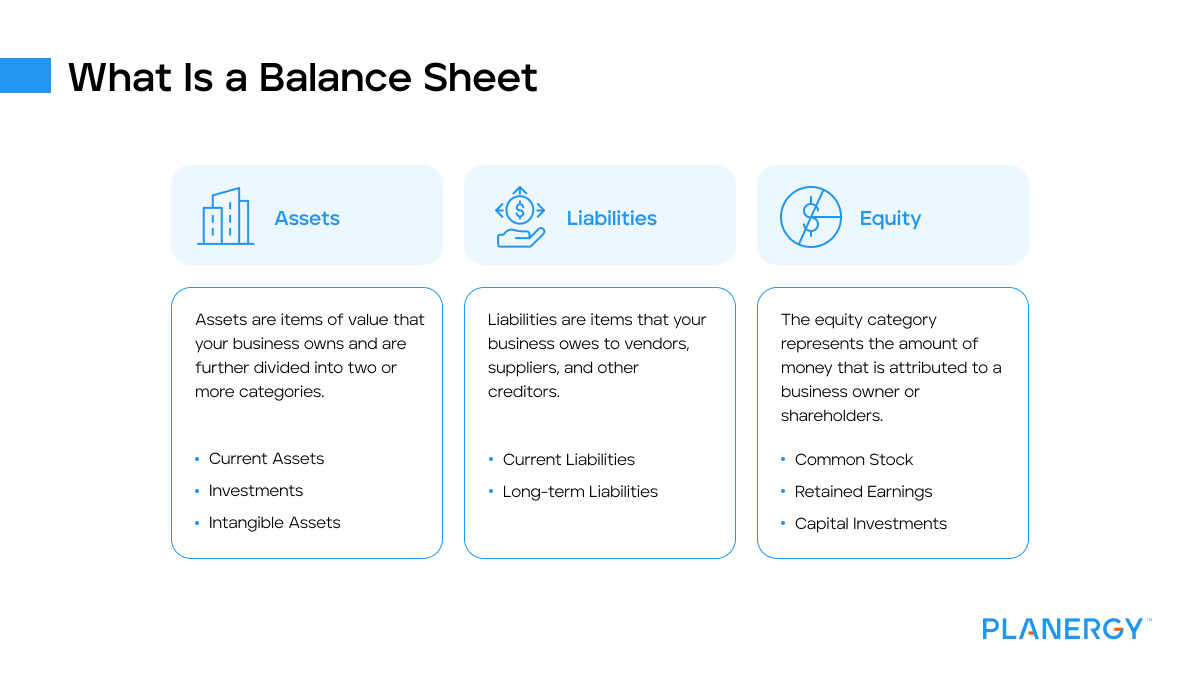

What Is a Balance Sheet?

Your company’s balance sheet is divided into three categories.

Assets

Assets are items of value that your business owns and are further divided into two or more categories. Assets include:

Current Assets

Cash and cash equivalents

Petty cash

Accounts receivable (money owed to the business from customers and others)

Inventory

Marketable or short-term securities

Investments

Land

Buildings

Equipment

Intangible Assets

Goodwill

Trade names

Liabilities

Liabilities are items that your business owes to vendors, suppliers, and other creditors. Both long-term and short-term obligations are further divided into multiple categories:

Current Liabilities

Accounts payable

Notes payable

Wages payable

Interest payable

Short-term debt

Long-Term Liabilities

Notes payable

Long-term debt

Equity

The equity category represents the amount of money that is attributed to a business owner or shareholders. Equity categories include:

Common stock

Retained earnings

Capital investments

Once you understand the structure of a balance sheet, you’ll be able to manage it better.

What Are Accounts Payable on a Balance Sheet?

Since accounts payable represents payments owed to vendors and suppliers, it is always found on a balance sheet under current liabilities or short-term liabilities.

Current liabilities are debts owed within a year, and since accounts payable invoice amounts are usually due within ninety days or less, they will always be listed on the balance sheet as a current liability.

Because adequately managing the accounts payable process is essential for businesses of any size, all AP transactions must be posted to the balance sheet.

If you’re using an automated AP software application, this is done for you, but for those using a manual accounting system, keeping the balance sheet accurate requires additional work.

Are Accounts Payable an Asset on a Balance Sheet?

Accounts payable is not an asset, since it represents money owed, not something owned.

If your accounts payable balance is reflected on the balance sheet as an asset or has a debit balance, that indicates that there is an entry that has been incorrectly posted or a payment that has been made in error.

For example, when you record an invoice in accounts payable, you’re crediting your accounts payable account, which will increase the balance of the AP account in your balance sheet.

Once that invoice is paid, you’ll be debiting your AP account, reducing the balance displayed on your balance sheet since the invoice has been paid.

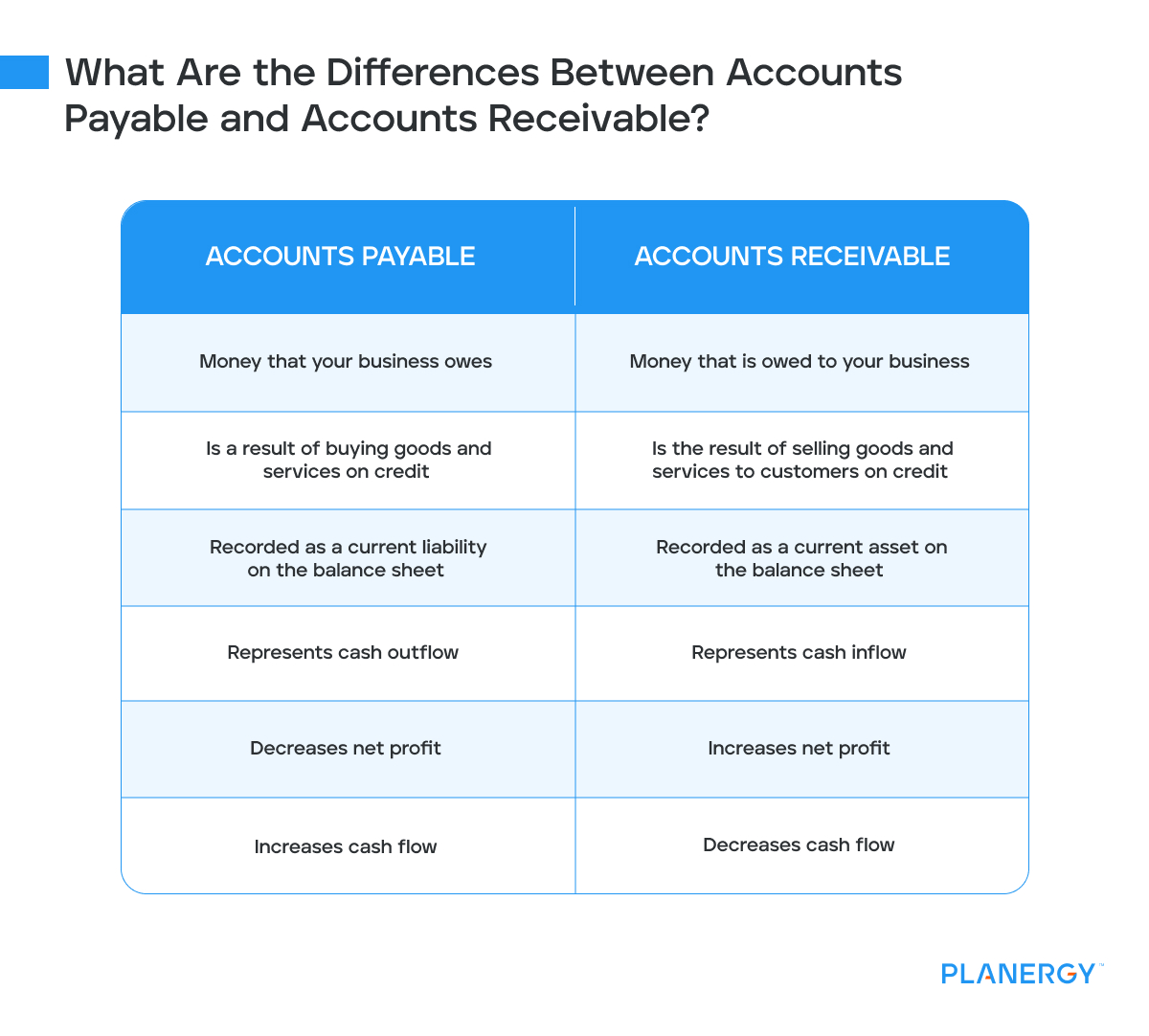

What Is the Difference Between Accounts Payable and Accounts Receivable?

Accounts Payable, or AP, represents the amount of money that a business owes vendors, suppliers, and other creditors. Accounts payable is always a liability account and should have a credit balance since it represents money that will be leaving the business.

For example, ABC Printing purchased $1,500 worth of office supplies. The journal entry to record the invoice would be as follows:

Date

Account

Debit

Credit

7-15-2023

Office Supplies

$1,500

7-15-2023

Accounts Payable

$1,500

Because office supplies are an expense account, we debit it, increasing its balance.

We then credit the accounts payable account, because it’s a liability account, and a credit entry increases the balance.

When we pay the invoice, we would complete the following journal entry:

Date

Account

Debit

Credit

7-31-2023

Accounts Payable

$1,500

7-31-2023

Checking Account

$1,500

We credit accounts payable when we pay the invoice because we want to reduce the AP account balance since the invoice is being paid.

We’re also reducing the checking account balance when we pay the bill since we’re reducing the balance of the checking account, which is an asset account.

Accounts receivable or AR represents the money that is owed to your business from your customers.

The AR account is always an asset account and should have a debit balance because it represents something of value that your business owns.

For example, ABC Printing sold $1,700 worth of printing services to their customer. To record the sale, you would complete the following journal entry:

Date

Account

Debit

Credit

7-10-2023

Accounts Receivable

$1,700

7-10-2023

Sales-Printing

$1,700

Because we want to increase the AR account balance, we debit it, since accounts receivable is an asset account.

We then credit the sales account, because the sales account is a revenue account, which is increased by posting a credit.

When our customer pays the invoice, we’ll complete the following entry:

Date

Account

Debit

Credit

7-25-2023

Checking Account

$1,700

7-25-2023

Accounts Receivable

$1,700

We also need to credit the accounts receivable account once the customer has paid, reducing the accounts receivable balance.

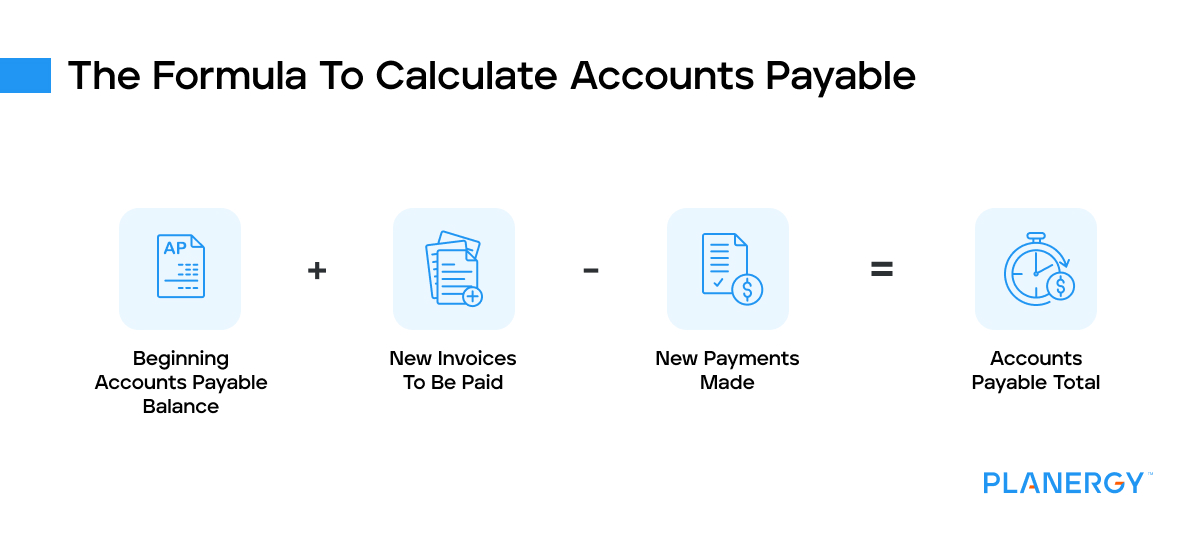

What Is the Formula for Calculating Accounts Payable?

Every time you record a supplier or vendor invoice or make a payment, you’re changing your accounts payable balance.

To calculate your accounts payable total, you’ll need to take your beginning accounts payable balance for the accounting period, add in all new invoices that have yet to be paid, and then subtract all payments that have been made.

All accounts payable transactions should be posted in a subsidiary ledger account, with the balance of the subsidiary ledger account matching the amount recorded on the balance sheet.

If the two amounts are not in balance, you’ll need to review the subsidiary ledger for possible errors.

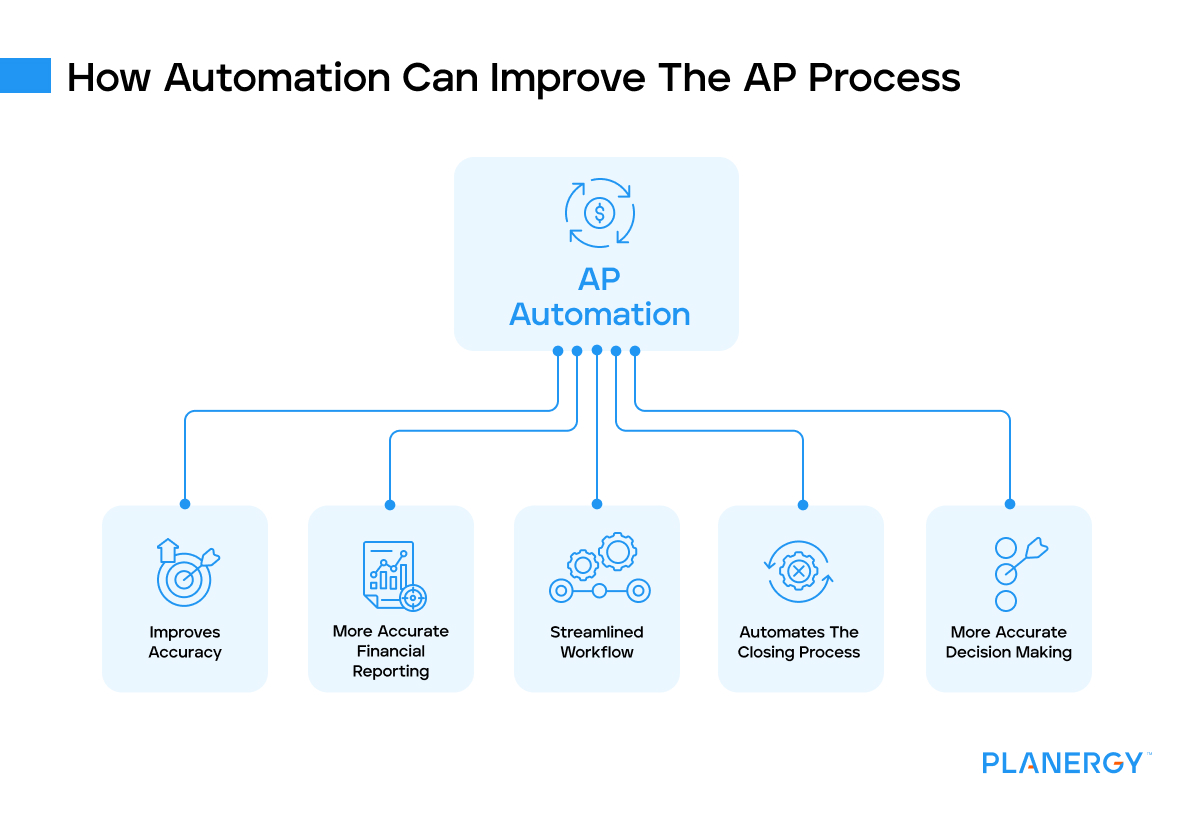

How Automation Can Improve the AP Process

For centuries, accountants and bookkeepers have kept their books manually, using paper and pen.

This process was made simpler with the invention of spreadsheet software applications like Microsoft Excel.

While paper and pen may seem like a viable method to keep your books for very small businesses with limited transactions, any business that wishes to be competitive in today’s market will need to invest in an accounts payable automation solution, like PLANERGY, which helps streamline the entire full cycle AP process from purchase order to invoice payment.

Here are just a few of the reasons why automation can streamline the entire AP payment process.

Improves Accuracy

Accuracy is essential for accounting and bookkeeping. An automated system helps eliminate data entry errors, reduces payments made in error, and eliminates costly invoice processing delays.

This allows you to take advantage of early payment opportunities while abiding by payment terms and payment due dates.

Provides More Accurate Financial Reporting

Financial statements like your balance sheet, income statement, and cash flow statement play an important role in your company’s finances.

Inaccurate input, transposing numbers, and forgetting to post journal entries mean that your reports are inaccurate as well.

For example, not recording a single AP transaction in your general ledger means it won’t be recorded on your balance sheet either, resulting in an understatement of both expenses and accounts payable.

Streamlines Workflows

Payable departments using a manual AP process often face delays in invoice approval and payment.

If you’ve ever routed an invoice to an approver, only to have it sit on the approver’s desk while they’re traveling, you know how time-consuming the invoice approval process can be.

At other times, invoices can be routed to the wrong individual or department, where they simply disappear, leaving you with costly late payment fees and a lot of unhappy vendors and suppliers.

AP automation streamlines the entire approval process, allowing approvers to review and approve invoices from anywhere.

On the other hand, manual closing can take days with limited safeguards in place to prevent mistakes and data omissions.

Using automation, AP accruals, and adjusting entries are recorded when needed. When combined with the right accounting software; imbalances are immediately flagged for further investigation and bank account reconciliations are completed for you.

More Accurate Decision Making

It’s difficult to make good decisions if tools and resources are inaccurate.

Switching to automation ensures that budgets, forecasting, decision-making, and strategic planning are completed using the most accurate data available.

Financial health is vital to your business’s success.

If you’re struggling with a manual accounts payable process, making the move to automated accounts payable software makes sense for your internal controls in accounts payable and your bottom line.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")