We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Whether you’re a small business owner or run a global entity, there are certain financial processes your finance team is tasked with.

One of the most important is month-end closing. The month-end closing process helps ensure that all revenue and expenses are properly accounted for and that financial statements are accurate.

Finance professionals have dreaded the month-end closing process, and there’s no denying that it is a time-consuming process that must be done accurately and timely.

However, by using a checklist and utilizing the latest technology, the monthly closing process can be completed in mere hours instead of days.

What Is Month-End Closing?

While the year-end financial close is the most comprehensive and typical closing process, most accounting departments also complete a close for each accounting period.

This consists of a series of steps completed at the end of every month to ensure that all financial transactions have been properly accounted for.

To complete the month-end close, a complete review of financial data including accounts payable and accounts receivable accounts and bank statement reconciliation is necessary.

The month-end closing process can be long and complex for those still using a manual accounting system and manual processes in procurement, but with the use of automated accounting software, most of the month-end closing process is completed automatically.

What Is the Purpose of Month-End Closing?

Throughout the month, the accounting department spends the majority of its time recording financial transactions, posting payments, and paying bills.

The month-end close provides an opportunity to review these and other financial records for accuracy and produce a complete set of financial statements.

Why Is Month-End Closing Important for Your Business?

Month-end close is important for several reasons. The most important reason is that without properly closing the month, your financial statements will not be accurate and can negatively impact the company.

For example, if you don’t accrue payroll for the month then your payroll expenses for the closed month and the following month will be inaccurate.

Next, an understatement or overstatement of expenses will directly impact your net profit and may influence subsequent decision-making based on that net profit.

If your payroll expenses are not accrued for June, your profit margin will be much higher than it would be if those expenses were included in June.

That information can lead to overspending based on the reported net profit, which may prove disastrous for your business.

For example, Nancy forgets to accrue payroll for June, which totals $450,000. Because of that omission, when Nancy prints her profit and loss statement for June, her net profit will be overstated by $450,000.

Understated Net Profit

Actual Net Profit

$895,000

$445,000

If Nancy makes a purchase for $600,000 in early July based on the erroneous net profit total, her business could be in serious trouble.

Accurate financial statements are also needed to prepare a budget for your business, and accuracy in financial reporting is an absolute must for tax compliance.

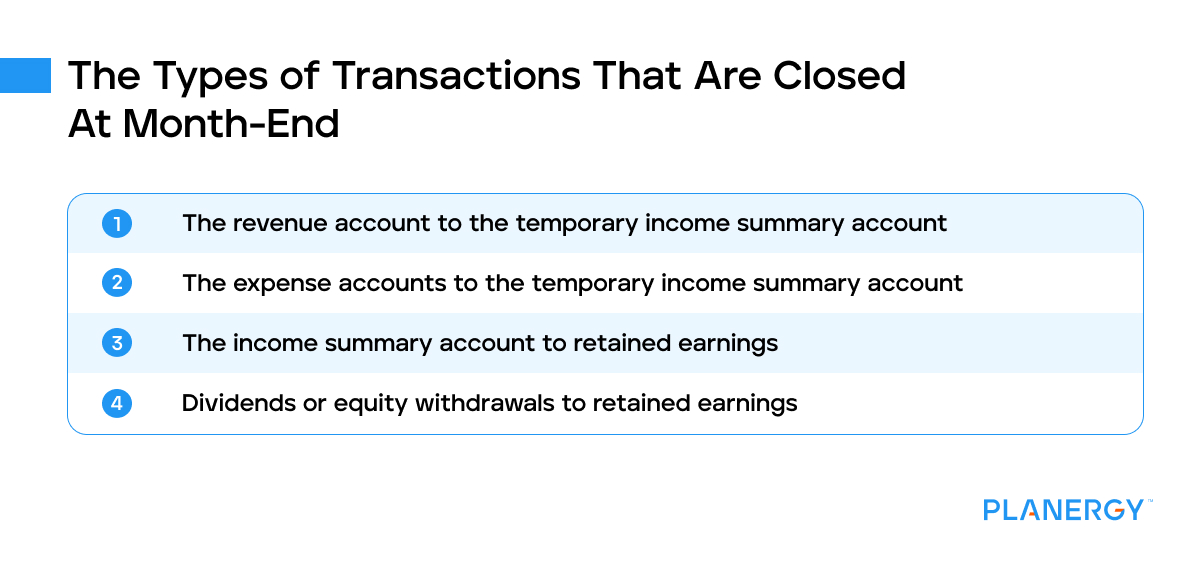

What Are the Types of Transactions That Are Closed at Month-End?

To properly close your books for the month, you’ll need to close out both revenue and expenses. Doing so ensures that next month’s balances are accurate in the general ledger.

To zero out current revenue and expenses, follow these steps:

Close the revenue account to the temporary income summary account

Close the expense accounts to the temporary income summary account

Close the income summary account to retained earnings

Close dividends or equity withdrawals to retained earnings

These tasks are performed automatically if you’re using an automated accounting application, but for those using a manual system, you’ll need to record these transactions manually in your general ledger.

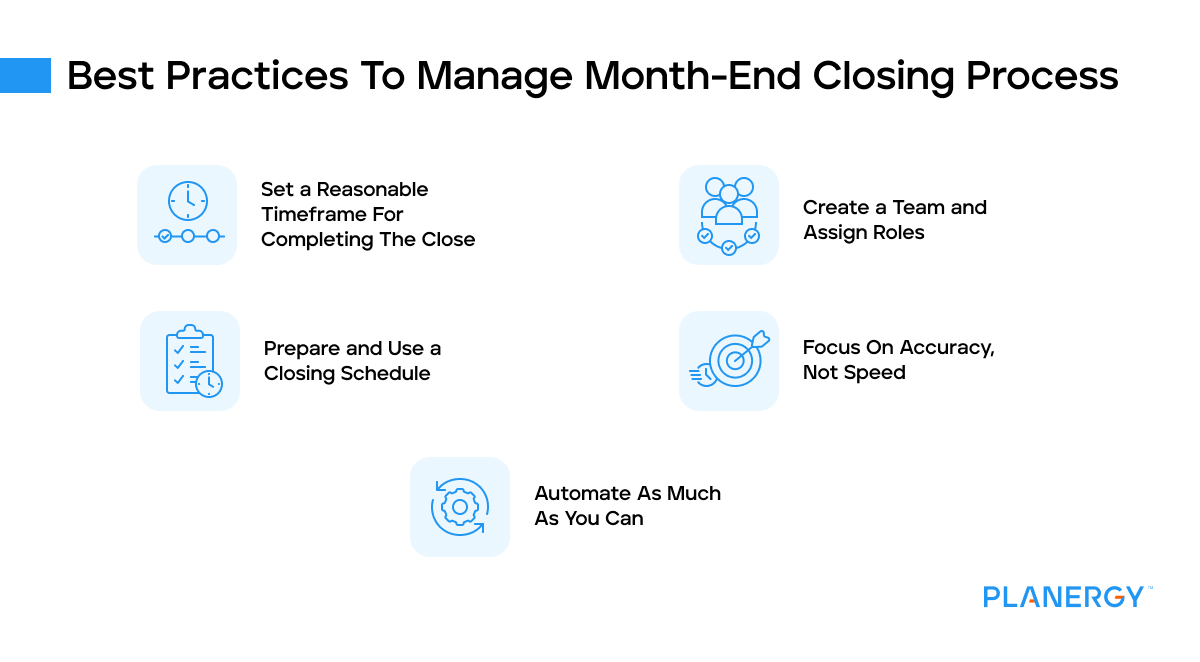

Best Practices To Manage the Month-End Closing Process

The best way to manage financial close at month-end is to implement best practices around the month-end closing process. These best practices should include the following.

Set a Reasonable Timeframe for Completing the Close

Leaving the closing process open-ended can be confusing. Set a closing date along with a timeframe for completing the month-end close and adhere to it.

If the department exceeds the established timeframe, figure out why and make the necessary changes so the timeframe can be adhered to in future months.

Create a Team and Assign Roles

If you’re a one-person accounting department, you can skip this step. But for larger businesses with active accounts receivable and accounts payable departments, assigning specific roles and workflows to the accounting team can expedite the closing process.

It’s impossible to complete the month-end close on time if you haven’t received the appropriate documentation from the various departments.

If closing begins on the 15th of the month following the month being closed, creating a deadline for having journal entries completed, accounts reconciled, and expenses accrued will streamline the entire closing process.

Focus on Accuracy, Not Speed

While you may want to complete the month-end closing process as quickly as possible, in this instance, accuracy is much more important than speed.

While staff must complete journal entries and reconcile accounts in a timely fashion, it’s more important that those reconciliations are an accurate reflection of your business. If you are going to carry out financial analysis on the data and make decisions it needs to be correct.

Encouraging staff to complete journal entries and reconciliations quickly can lead to errors that may not be found until months later.

By implementing automated systems, business processes such as the month-end closing are completed automatically, allowing your staff to complete their work promptly while providing more accurate data.

What Steps Should Be Included in the Month-End Checklist?

A month-end close checklist template can be helpful during the closing process and should be relevant for each individual business.

For example, if you operate a company that provides a service, your month-end checklist will be different from that of a company that manufactures products and manages inventory.

Before you get started, you’ll need access to the following financial activity:

Total revenue for the period

Bank account information

Inventory numbers (for those that have inventory)

Petty cash fund totals

Financial statements including a balance sheet, income statement, and cash flow statement

Fixed asset totals

Revenue and expense account totals

General ledger

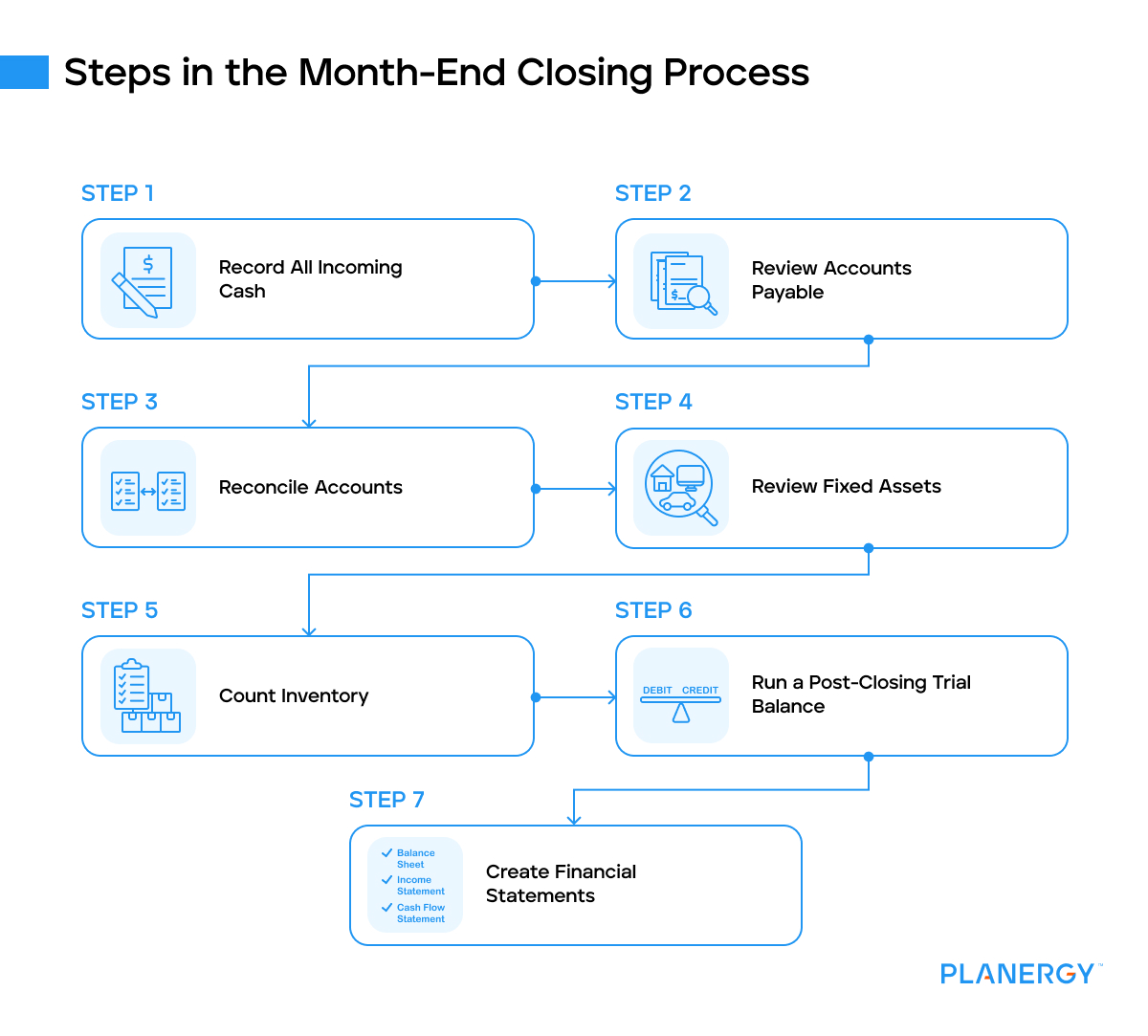

Once this information is gathered, you can begin the month-end closing process, following these steps.

Record All Incoming Cash

Be sure that you’ve recorded all of your incoming cash for the month, which can include petty cash deposits, cash for miscellaneous expenses, and accounts receivable payments.

This is also a good time to see if there are any credit memos issued to customers that need to be addressed before closing.

Review Accounts Payable

The AP review should include a review of all purchase orders to determine whether an invoice has been received.

If a product or service has been ordered, but the invoice has not yet been received, it will need to be accrued as an expense.

One of month-end closing’s most important tasks is reconciling your bank accounts and credit card statements.

Most accounting software applications complete much of the accounting reconciliation process, but if your business is using a manual accounting system, you’ll need to reconcile your bank account balance with your general ledger balance.

This includes identifying and recording any outstanding checks against your bank balance and accounting for unrecorded deposits or other discrepancies that appear in the bank.

In addition to bank reconciliations, you’ll also want to reconcile prominent accounts like accounts receivable and accounts payable (mentioned earlier), and prepaid accounts to ensure that ending balances are accurate and all income and outgoing cash is properly accounted for.

Review Fixed Assets

If you currently manage multiple fixed assets, they should be reviewed at month end to determine whether assets have been added or disposed of.

Fixed assets can include buildings, equipment, furniture and fixtures, land, machinery, and computer hardware or software.

When reviewing fixed assets, you’ll also need to manage any corresponding depreciation schedules and accumulated depreciation balances, making sure that a journal entry is completed for any monthly depreciation expenses.

Count Inventory

Companies that actively manage inventory should reconcile inventory with their trial balance to ensure that inventory is properly accounted for.

In addition, you should also do an inventory count and make any inventory adjustments before the month-end close.

Run a Post-Closing Trial Balance

The post-closing trial balance is run after all transactions have been posted. The purpose of the trial balance is to ensure that debits and credits balance.

If they don’t balance, there’s likely a posting error that needs to be addressed.

Create Financial Statements

One of the final steps in the month-end closing process is the preparation of financial statements.

Used as a measuring tool to ensure that all transactions have been properly posted into your general ledger, you’ll want to create the following financial statements.

Balance Sheet

Your balance sheet follows the accounting equation of Assets = Liabilities + Equity. Balance sheet accounts include assets, liabilities, and equity.

Income Statement

Your income statement provides a detailed look at income and expenses for the month, both before and after depreciation, amortization, and taxes have been factored in.

Your income statement is one of the most valuable financial statements you can run.

Cash Flow Statement

Your cash flow statement provides detailed information on incoming and outgoing cash for the month.

Divided into three sections, the cash flow statement lets you see exactly what areas of the business are bringing in or spending the most cash.

Once your statements have been prepared, reviewing financial information for accuracy is important. It’s also helpful to have another staff member review the completed statements, identifying any potential issues.

Is Month-End Close Hard?

More time-consuming than difficult, for business owners without a bookkeeping or accounting background and using a manual accounting system, month-end closing can be overwhelming, often taking more than ten days to complete.

Using automated accounting software can cut that time down by half or more, automating most of the processes that those using manual accounting struggle with, including closing revenue and expense accounts to the income summary account and then adjusting those totals in the retained earnings accounts.

As an added bonus, most accounting software applications automatically import bank transactions into your general ledger in real time, cutting down on the amount of time needed to reconcile both bank and credit card accounts.

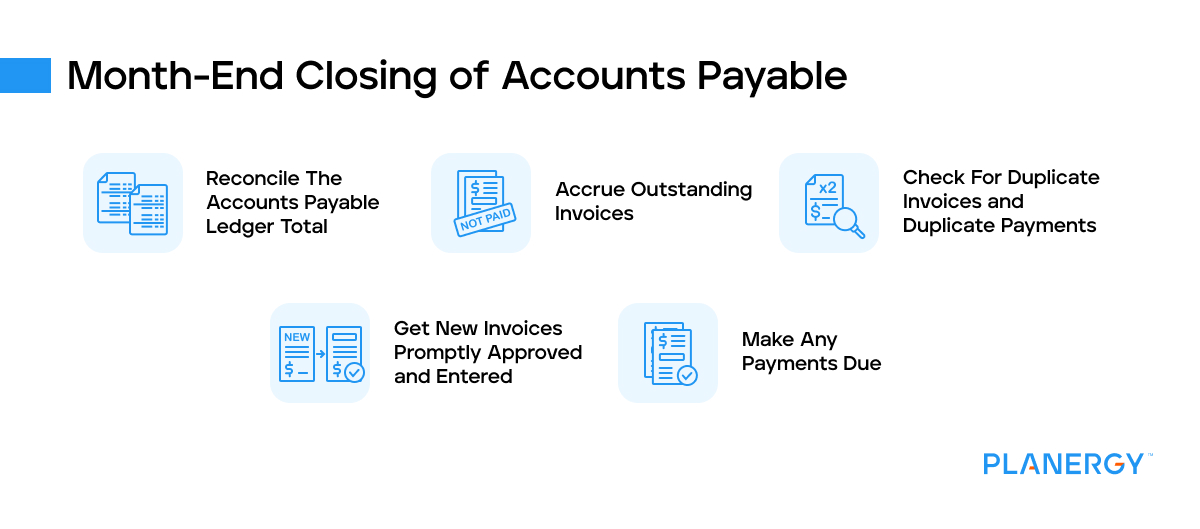

The Month-End Closing of Accounts Payable

Closing accounts payable is part of the month-end closing process.

Reconciling the accounts payable ledger includes comparing open AP amounts against current invoices and adjusting the balance accordingly.

Accrue Outstanding Invoices

Review purchase orders and shipping receipts for items ordered that you have not yet received an invoice for. Those orders will have to be accrued.

Check for Duplicate Invoices and Duplicate Payments

Month-end closing is a good time to look for duplicate invoices recorded in the general ledger along with any duplicate payments that may have been made.

Get New Invoices Promptly Approved and Entered

If you have a stream of invoices arriving at the end of the month, try and expedite the invoice approval process so those invoices can be entered prior to closing the month.

Make Any Payments Due

If you have vendor payments due at the end of the month, paying them now will ensure a more accurate accounts payable balance at month-end as well as more accurate financial statements.

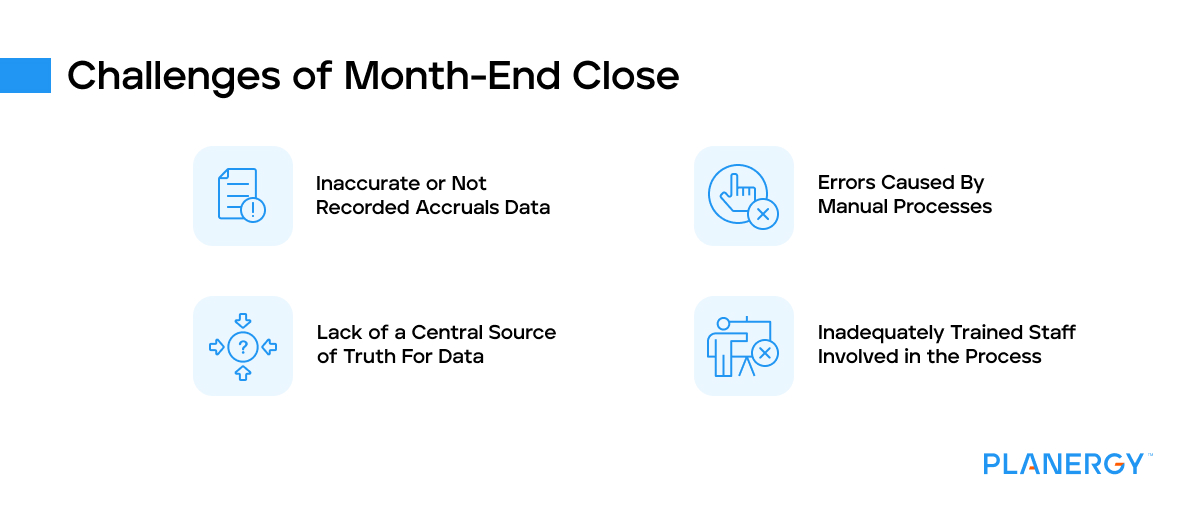

The Challenges of Month-End Closing

Like any accounting process, month-end closing is not without its challenges. However, many of the challenges stem from using manual accounting processes.

Inaccurate or Not Recorded Accruals Data

Nowhere is this more obvious than when accruing month-end expenses or managing spending totals for the month.

Without an automated process in place, accruals can be inaccurate or not recorded at all, while the lack of automation also makes it difficult to properly account for current spending levels.

Errors Caused by Manual Processes

Manual processes also mean more errors. While it’s important that you receive reconciliation documents promptly, it’s just as important that those documents are accurate.

It’s accurate to say that a careful review of documents can spot some errors in financial data, but the best way to avoid errors is to use an automated accounting software application.

Lack of a Central Source of Truth For Data

Challenges can also arise when using multiple systems for accounting.

Pulling data from systems that don’t communicate with each other or using multiple spreadsheets to track cash balances results in more time spent transcribing information from multiple applications.

The best way to avoid that is to use an automated accounting software application that does most of the work for you.

Inadequately Trained Staff Involved in the Process

Other challenges you may encounter during the closing process include inadequately trained staff that don’t understand the closing process.

Before handing over the month-end closing process to a staff member, make sure that they are properly trained and provided with the proper tools and resources to complete the process.

If these challenges aren’t addressed, the result will be inaccurate financial reporting, an increased risk of fraud, and the inability to accurately budget and forecast.

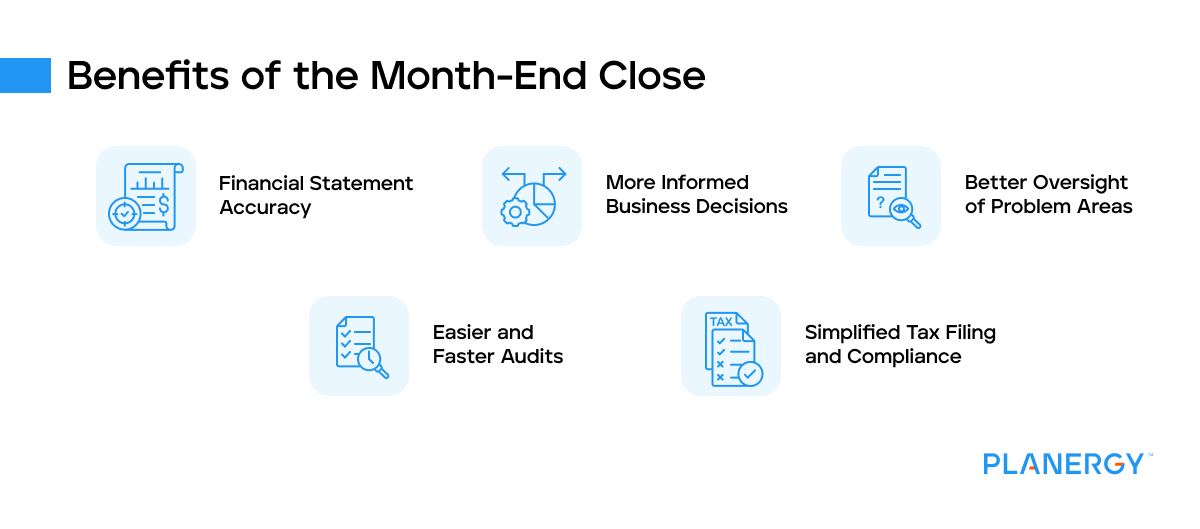

The Benefits of the Month-End Close

While financial statement accuracy is the biggest benefit to a proper month-end close, there are other benefits to be had as well including:

The ability to make more informed business decisions

Simplified tax filing and compliance

Ability to spot and correct potential trouble areas

Easier and faster audits

Accurate month-end closing is also a must for other stakeholders such as investors and financial institutions.

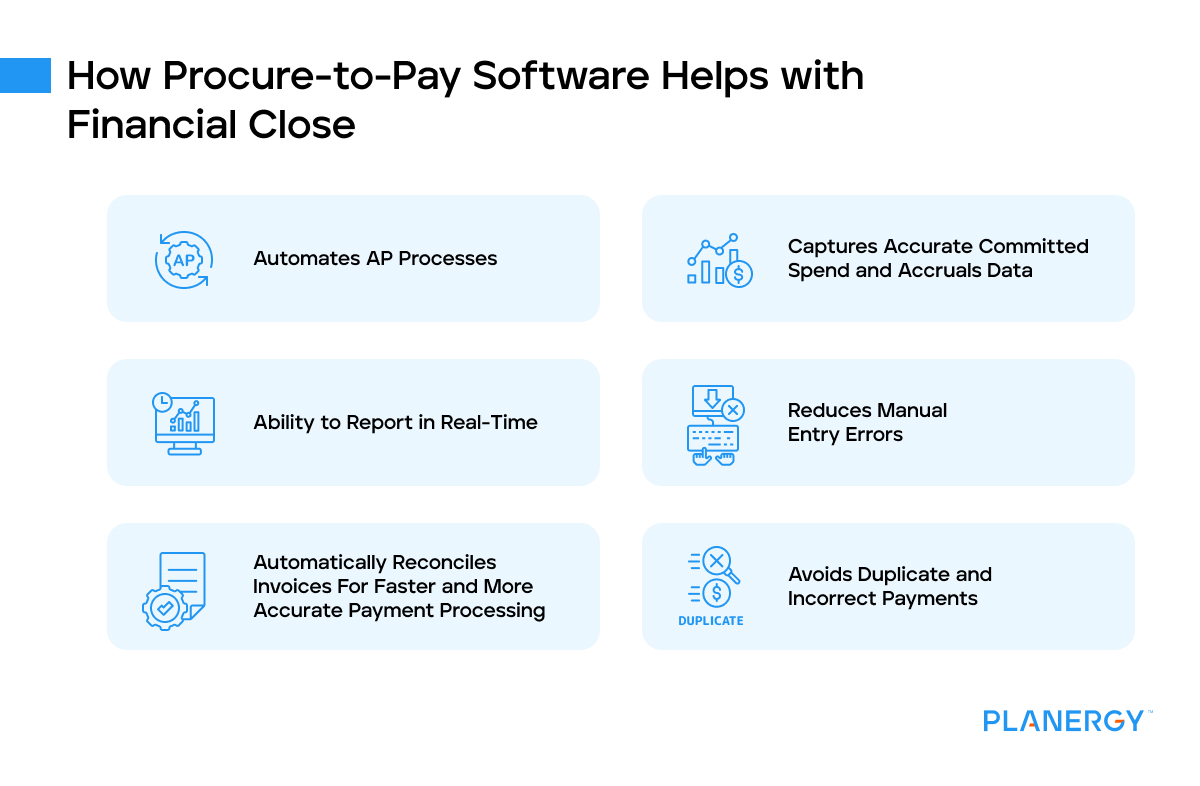

How Procure-to-Pay Software Helps with Financial Close

The best solution to an unwieldy financial close process is to implement an automated procure-to-pay application, like PLANERGY, which helps streamline the entire month-end closing process by eliminating manual systems.

When using a procure-to-pay application, like PLANERGY, time-consuming tasks such as manual data entry, three-way matching, and account reconciliation are completely automated, while spending levels remain transparent, resulting in more accurate accruals and real-time reporting.

In addition, duplicate invoices and payments become a thing of the past, freeing up your accounting staff to handle more important tasks.

Month-End Processing is Part of Doing Business

The bottom line is that month-end closing is a necessity for businesses of just about any size. The key to handling closing is to use the best tools and resources possible to achieve more accurate outcomes in the least amount of time.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")