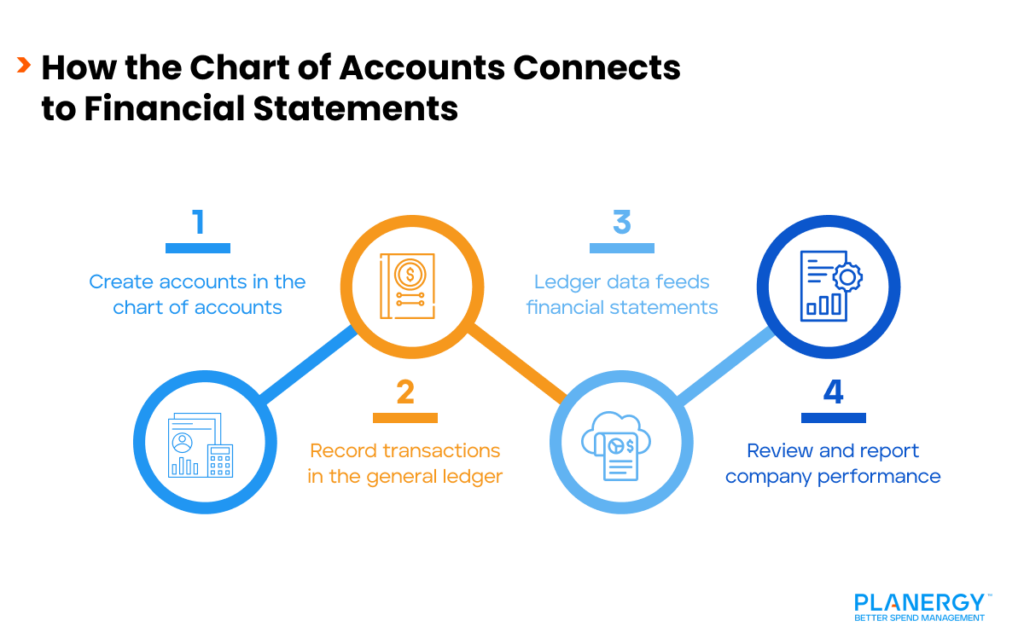

Every time you post an invoice, record a customer payment, or pay a credit card bill, you record those transactions to your general ledger, which contains a list of specific accounts that encompass your chart of accounts.

But what exactly is a chart of accounts?

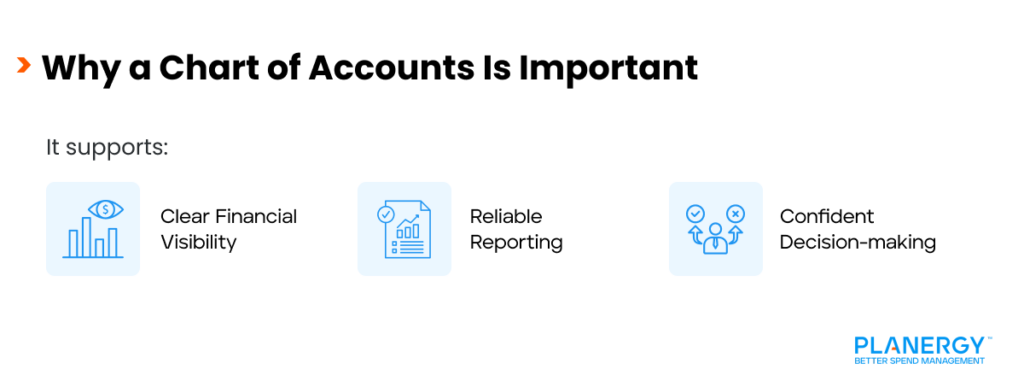

We’ll explain exactly what the chart of accounts is, why it’s so important, and how to prepare one for your business.

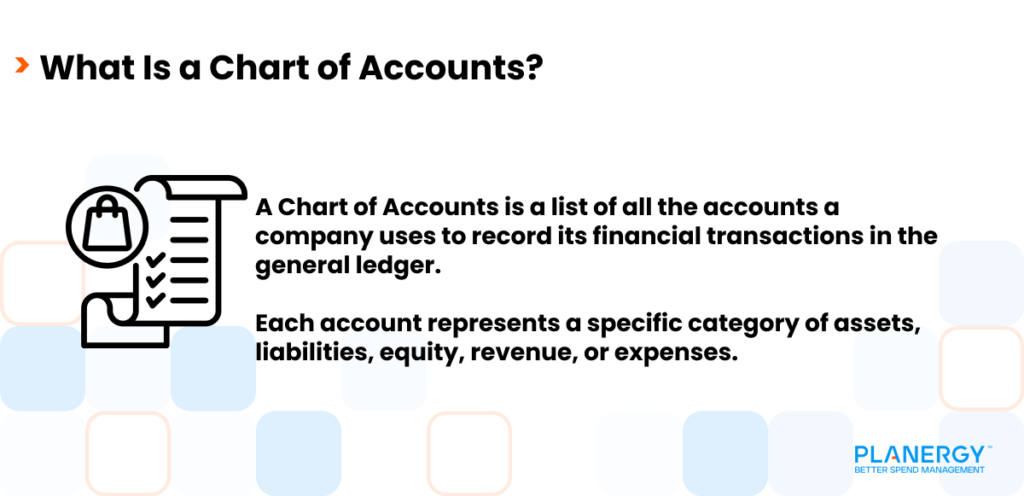

What is a Chart of Accounts?

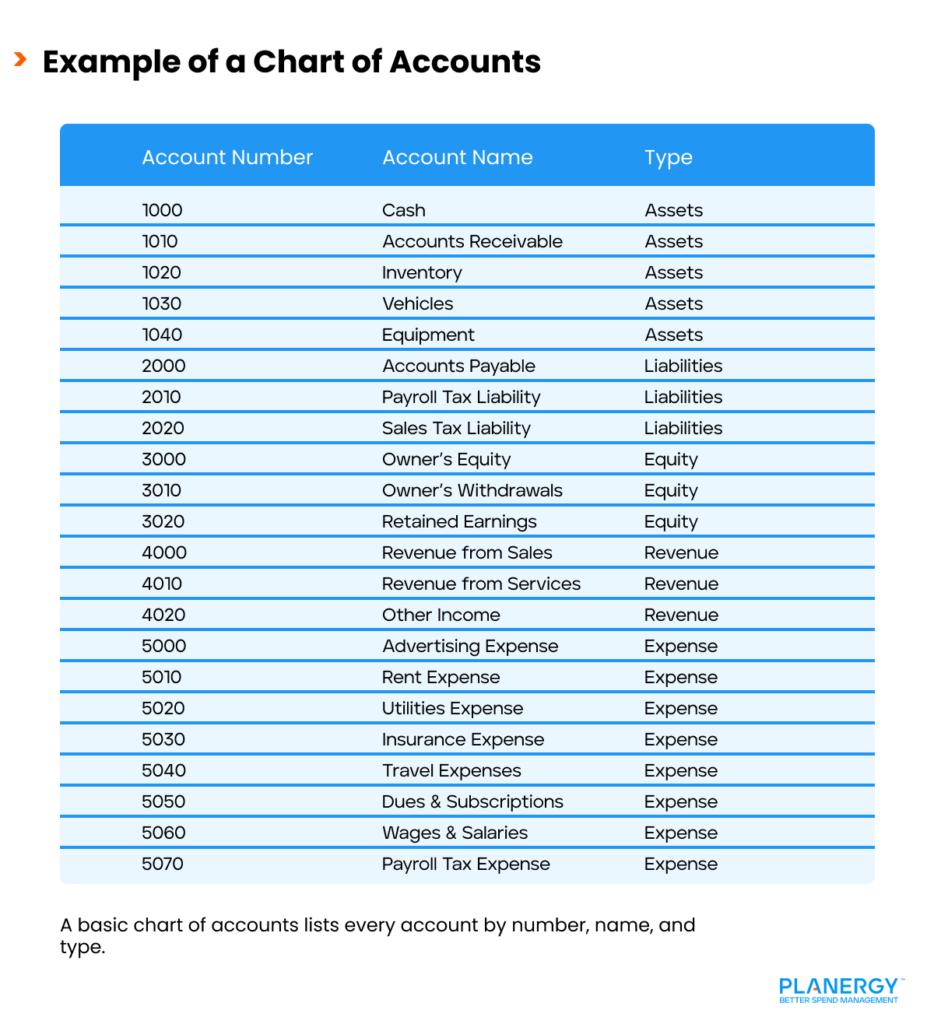

The chart of accounts is the repository for all of your financial accounts because every bookkeeping transaction made in your business is assigned to an account in your chart of accounts.

While your general ledger may serve to ‘house’ all of your company’s financial transactions, the chart of accounts is the foundation for that house.

")

")

")