We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

As a business owner, part of your responsibility is choosing the right method of accounting for your business.

In many cases, small business owners choose the cash accounting method because it resembles a process that they’re familiar with.

However, if you plan on adding employees, growing your business, obtaining a business loan, or seeking out investors, the accrual accounting method may be the better accounting method for your business.

First, let’s discuss what cash accounting and accrual accounting are, and how they differ.

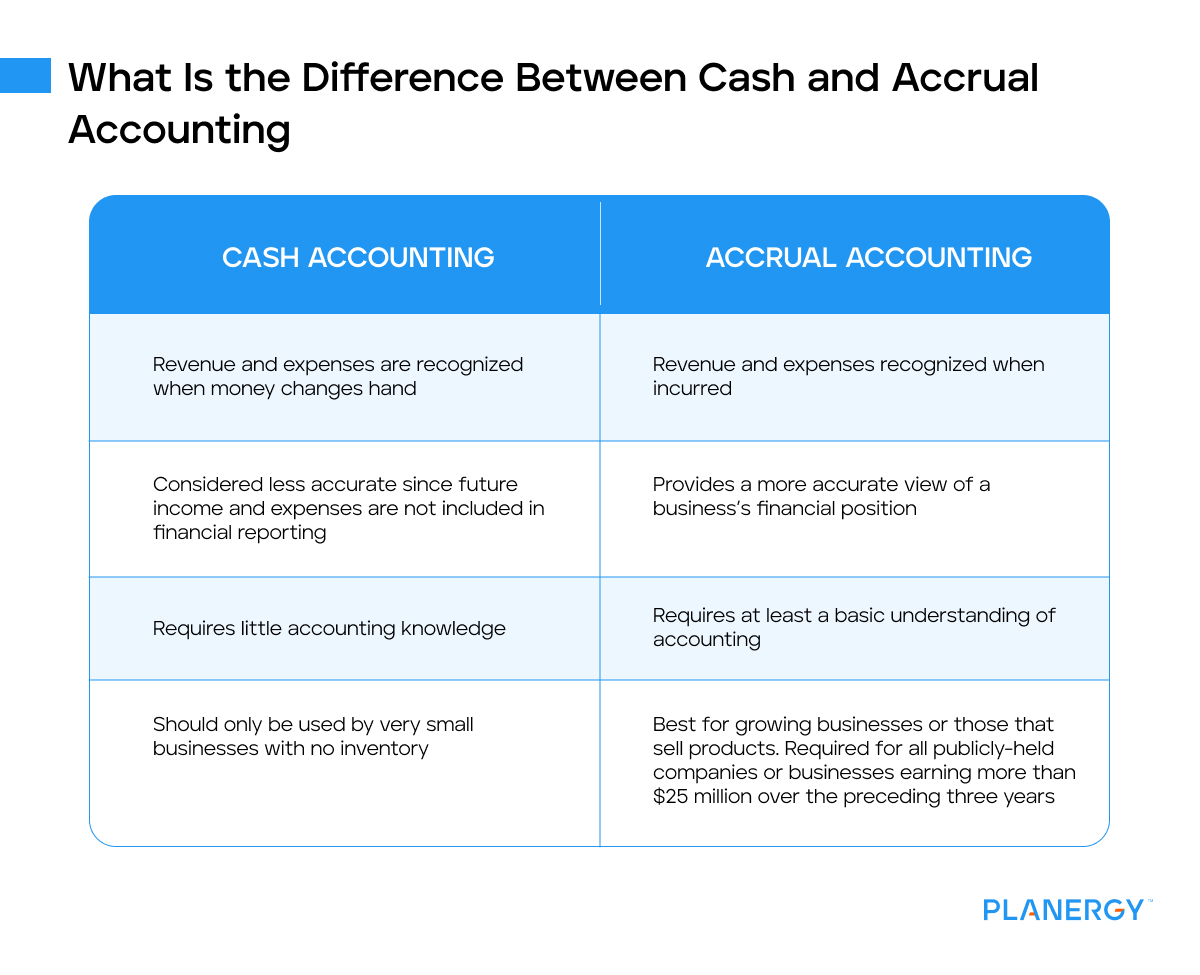

What Is the Difference Between Cash and Accrual Accounting?

New business owners are likely more familiar with the cash basis method since it’s used to handle personal finances.

With cash accounting, revenue and expenses are recognized when cash changes hands.

For example, if your business uses cash accounting and you receive your utility bill in the mail, you would only record the expense when the bill was paid.

Cash accounting only records a single entry, much like you do when you manage your personal bank account.

For example, when a customer pays you for a service, you would record it as a deposit when the funds are received, not when the services are rendered.

For larger businesses or small businesses looking to grow, the better option is accrual accounting, which recognizes revenue and expenses when they’re earned, not when money is received or a bill is paid.

Using the utility bill as an example, in accrual accounting, you would record the expense in the month the bill is received, even though it won’t be paid until the following month.

Accrual accounting requires you to use double-entry bookkeeping, which means that you will have two entries for each transaction.

In double-entry bookkeeping, you would record your customer payment to two accounts, a cash account and a sales account. Double-entry bookkeeping allows you to record transactions when they occur, not when money changes hands.

Accrual accounting entries displayed on your balance sheet under accounts payable, accounts receivable, wage and salary expenses, and tax expenses.

The following chart represents some of the major differences between cash and accrual accounting.

Cash Accounting

Accrual Accounting

Revenue and expenses are recognized when money changes hand

Revenue and expenses recognized when incurred

Considered less accurate since future income and expenses are not included in financial reporting

Provides a more accurate view of a business’s financial position

Requires little accounting knowledge

Requires at least a basic understanding of accounting

Should only be used by very small businesses with no inventory

Best for growing businesses or those that sell products. Required for all publicly-held companies or businesses earning more than $25 million over the preceding three years

Because of its complexity, it’s recommended that anyone using accrual accounting in their business have some basic accounting knowledge.

If you’re using double-entry accounting, you’re automatically recording an accrual each time you sell to a customer on credit or record a utility bill in the month the service took place but is paid the following month.

Accrual accounting uses the matching principle, part of GAAP rules, which states that revenues and expenses should be recognized in the same period.

Aside from these standard accruals, accruals are also used to properly account for revenue, prepaid expenses, payroll expenses, and other general expenses that are expected for the accounting period but have not yet been received.

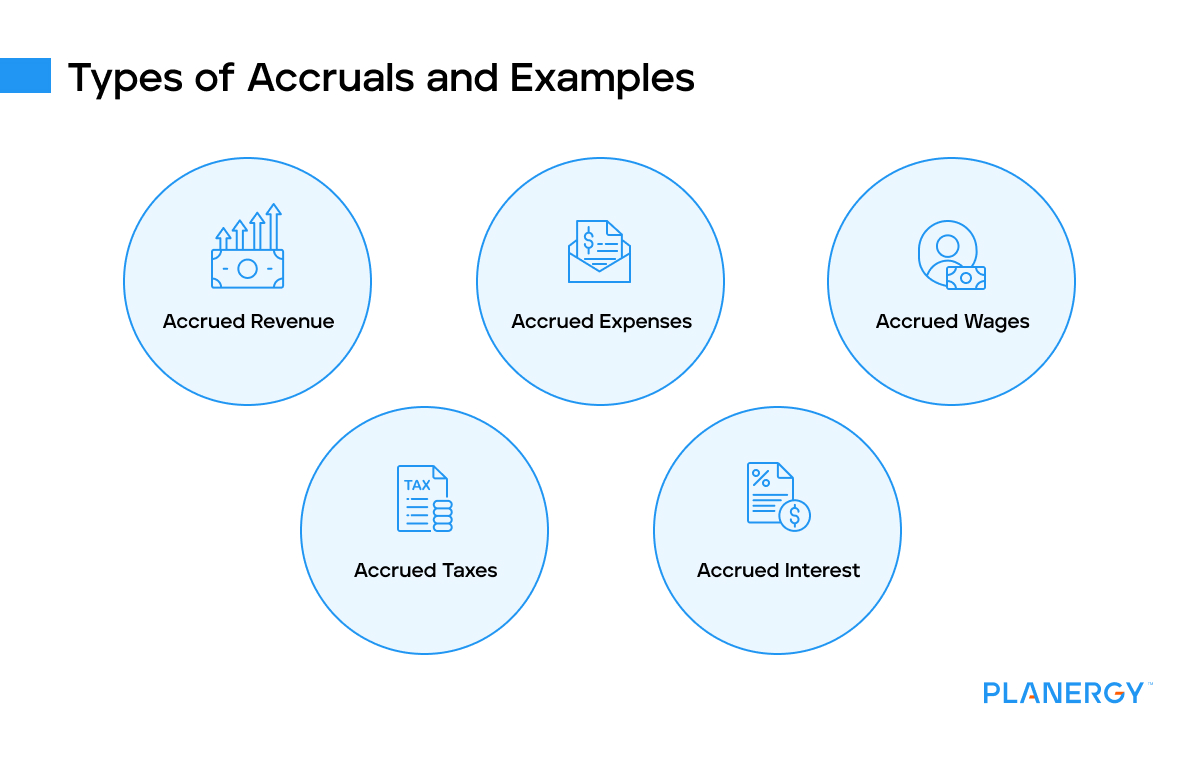

Types of Accruals and Examples

The two most common types of accruals are accrued revenue and accrued expenses, but businesses will also need to account for accrued wages and accrued taxes.

Accrued Revenue

When accruing revenue, you record revenue when it’s been earned but funds have not yet been received.

Any time you sell a product or service to a customer on credit, that revenue is recorded in the month that the sale took place. Accrued revenue is recorded as a receivable.

For example, your company provides consulting services to a client on October 19, 2023.

Because you have payment terms with your client, they do not have to pay for the consulting services until November.

But you’ll need to account for the sale of the services in the month they were incurred which is October, so you’ll debit your accounts receivable account and credit your sales account.

Accrued Expenses

Accrued expenses are expenses that need to be accounted for in a specific accounting period.

Like accrued revenue, accrued expenses should be recorded in the period that they’re incurred, not the period that they’re paid.

Several types of expenses are commonly accrued each accounting period, including the following.

Accrued Wages

Payroll is an area where accruals are fairly common, particularly for those with weekly and bi-weekly pay periods.

Recording accrued wages allows you to account for payroll expenses in the correct period, even if the employee is not paid until the following week.

For example, you pay your employees bi-weekly, with their last paycheck on October 27. But there are still two days left in October that will have to be accounted for.

To do that, you would need to accrue payroll for those two days to ensure that October payroll totals are accurate.

Accrued Taxes

Whether it’s payroll taxes or sales tax, taxes will need to be accrued until the tax is due. In some cases, that may be monthly, quarterly, or annually.

Whatever the case, accruing the taxes ensures that the expense is recorded when incurred, not when the taxes are paid.

If you charge sales tax on purchases, you will need to accrue the sales tax due as a payable item until you pay taxes.

Accrued Interest

Accrued interest can be an expense or revenue. For example, if you purchase a bond that pays interest quarterly, you will need to accrue the interest that will be paid each month by recording it as a credit to your interest revenue account and debiting the interest receivable account.

If accrued interest represents interest that you’re paying, such as for a loan, the interest amount will be credited to accrued liabilities and debited to the interest expense account.

For example, accruing revenue will be completed whenever you bill a customer for a credit purchase.

This holds for bills received but not due until the following month. When those bills are entered into your software application, the amount you owe will be automatically accrued.

But there are still some accruals that you will need to create a journal entry for. For example, let’s say you normally receive your electric bill by the end of the month.

However, it’s October 31, and you haven’t received the bill yet. If you want to properly account for all expenses incurred in October, you’ll have to accrue the expense.

Since you don’t have the electric bill, you’ll have to estimate the amount that will be due, which will be corrected later when the bill is due.

To accrue your electric bill, you’ll have to complete the following journal entry:

Date

Account

Debit

Credit

10-31-2023

Electricity Expense

$195

10-31-2023

Accrued Expenses

$195

When the electric bill arrives in November, the actual amount of the bill is $201.

To properly record the bill for payment, you will first need to reverse the October accrual for $195.

Date

Account

Debit

Credit

11-01-2023

Accrued Expenses

$195

11-01-2023

Electricity Expense

$195

Once the reversal is complete, you’ll then post the bill for the actual amount.

Date

Account

Debit

Credit

11-05-2023

Electricity Expense

$195

11-05-2023

Accrued Expenses

$195

Most accounting software applications offer automatic accrual reversals, which eliminates the need to reverse the prior month’s accrual.

If your software doesn’t offer this feature or you’re using a manual system, you’ll need to remember to reverse the prior month’s accrual, or your revenue or expenses will be incorrect.

What Is the Difference Between Accruals and Actuals?

Accruals are typically an estimate of what you expect an expense to be.

When you receive the invoice for the accrued expense, that is considered the actual, since it represents an accurate total.

Except for payroll, where you know exactly how much your employees will be paid, estimating revenue or expenses is necessary.

What Is a Contra Account?

A contra account is used on a balance sheet to offset the value of a paired asset. When recording depreciation accruals, you may need to use a contra account.

For example, your business purchases a delivery truck for $40,000.

The value of the truck is listed on your balance sheet, but the truck loses value or depreciates.

The contra account; accumulated depreciation, is used to track the amount of depreciation that has been recorded against the truck’s original value.

A contra account should always have a negative balance or a zero balance since it’s used to reduce the value of an asset.

A debit balance in a contra account would be a violation of the cost principle which requires that an asset be recorded at its original value.

That means that a debit balance in a related contra account would inflate rather than reduce the value of the asset.

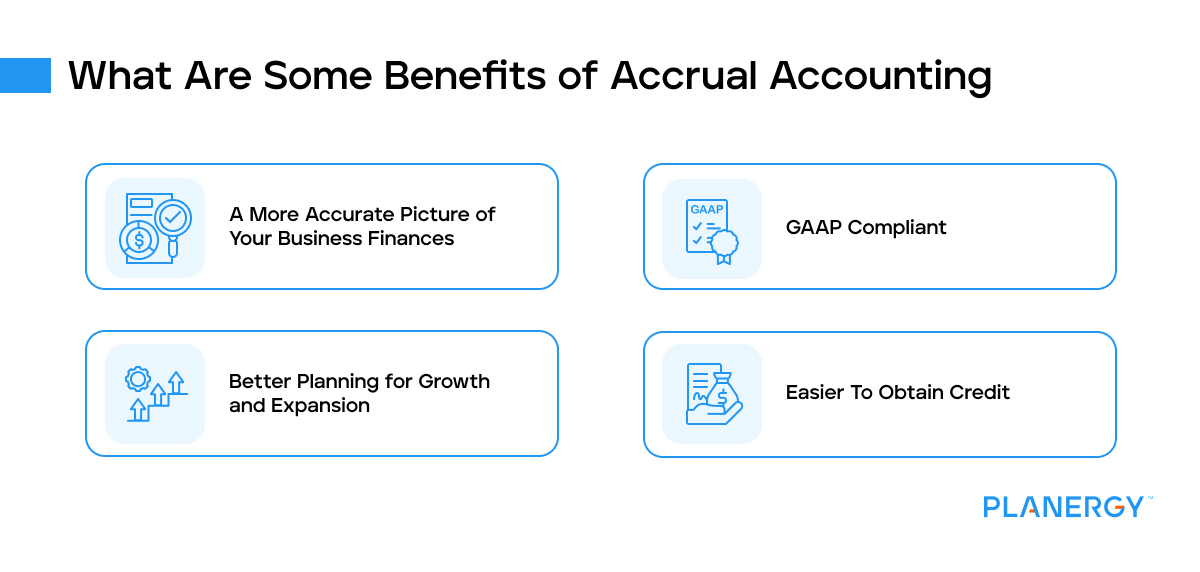

What Are Some Benefits of Accrual Accounting?

Even though accrual accounting is more complex than cash accounting, there are numerous benefits of using the accrual method to keep track of your finances.

A More Accurate Picture of Your Business Finances

While cash accounting is more straightforward, you’ll need to make the switch to accrual accounting to get the full picture of finances including which includes more accurate financial statements.

In turn, this provides you with a better understanding of how much revenue you earned and the expenses that were necessary for you to earn it.

GAAP Compliant

It may not be of major concern right now if your accounting is GAAP compliant if you’re still a private company.

However, being GAAP compliant is a good idea even for startup businesses since it provides more accurate forecasting capability and more accurate profit and loss reporting. It also helps mitigate against fraud while helping your business maintain a level of consistency.

Better Planning for Growth and Expansion

Part of growing your business is having the right tools in place to not only manage for today but also for the future.

Accrual accounting is done in real-time while cash accounting is completed after the fact, or after cash has exchanged hands during a specific period of time.

It’s also a necessity should you decide to seek out investors, who will require that your accounting records be accurate.

Like anything else, there are some downsides to accrual accounting, starting with the level of knowledge necessary to use the accrual method properly, which may require you to hire an experienced bookkeeper or accounting clerk.

Using the accrual accounting method also makes it more difficult to track and manage cash flow since your income statement balance will not reflect your true cash balance.

The best solution to the above issues is to use an automated accounting software application that streamlines the entire accounting process and automatically posts business transactions such as accruals.

Is Accrual Accounting the Best Method for Your Business?

If you’re a very small company with no plans to expand, cash accounting is likely sufficient.

However, if you carry inventory for resale, want to sell to your customers on credit, and have plans to expand in the future, the accrual method of accounting is the recommended accounting method for managing and maintaining the financial health of your business.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")