Accuracy and transparency are absolute musts when it comes to financial information.

While errors can and will happen, finding and correcting those errors is paramount for businesses.

If they’re not found, the result will be inaccurate financial reports.

Not only are erroneous financial statements a misrepresentation of your small business finances, which can directly impact areas such as cash flow, but depending on the size and scope of the variance, these errors can directly impact your relationship with vendors, suppliers, and investors.

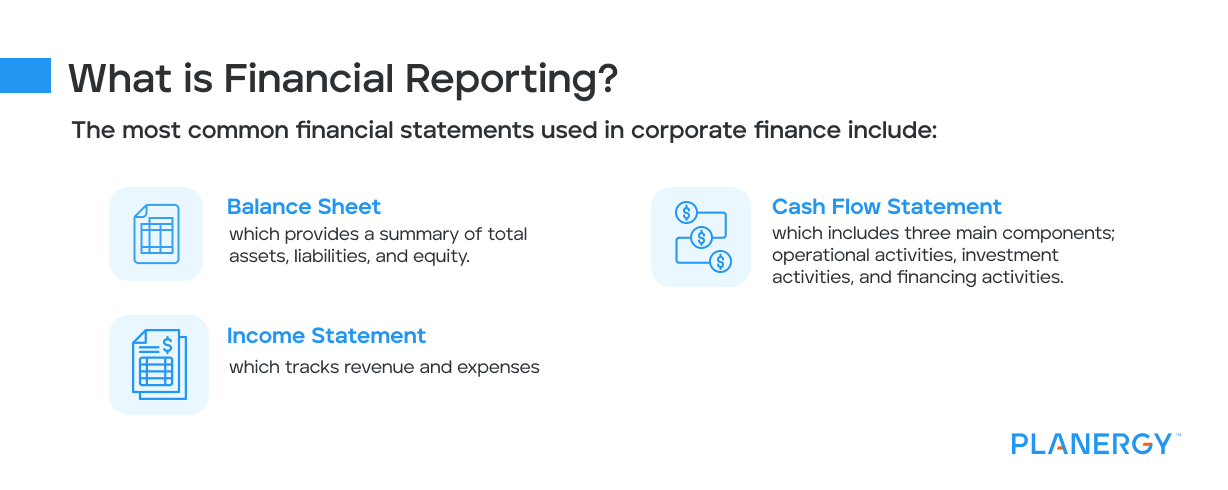

What is Financial Reporting?

Financial reporting is used to document and communicate the financial activities of your business.

Financial statements are usually produced by a bookkeeper or other accounting staff and are used internally by department managers and company officers including the CFO, and externally by CPAs, auditors, investors, shareholders, consumers, and creditors.

The most common financial statements used in corporate finance include:

Balance Sheet – which provides a summary of total assets, liabilities, and equity.

Income Statement – which tracks revenue and expenses including net and gross revenue, non-operating revenue, operating expenses, cost of goods sold, depreciation, and interest expense.

Cash Flow Statement – which includes three main components; operational activities, investment activities, and financing activities.

There are other common financial reports you can run at month’s end, but these three, along with the statement of shareholder equity, a must for public companies, are the most commonly shared externally.

Unfortunately, financial data has little use if it’s riddled with errors.

These errors, most often caused by data entry mistakes and omissions can wreak havoc with the accuracy of your financial statements.

Common Mistakes and How They Impact Financial Statements

Financial reporting errors are the result of accounting errors made throughout the fiscal year.

The following are a few of the most common errors made.

Error of Original Entry

The error of original entry occurs when the entire transaction is entered wrong.

For example, if you enter a payment of $5,000 as $500, your accounts will be in balance, but the bank balance will be understated and the customer accounts receivable balance overstated.

Error of Omission

Errors of omission are fairly common and can occur for several reasons.

The journal entry detail gets lost, or a staff member doesn’t realize that an expense hasn’t been recorded or doesn’t understand that it needs to be recorded.

This can happen quite often if you have an inexperienced accounting staff.

Errors of omission directly impact your cash flow balance since the transaction has not been recorded.

Error of Commission

This type of error can occur when something is posted to an incorrect account.

For example, you post a payment received and it’s recorded in the bank properly, but it gets posted to the wrong customer.

While this type of error may not impact your financial statements, it will certainly impact your accounts receivable balances.

Error of Transposition

Transposition errors are also common during the data entry process.

It’s easy to enter $795 as $597, leaving financial records understated or overstated.

Transposition errors can be difficult to find, particularly if you’re not up to date on bank reconciliations.

Error of Duplication

Duplication errors can happen when more than one person with access to the accounting system enters the same transactions.

Error of Principle

This error occurs when accounting transactions are not in compliance with generally accepted accounting principles (GAAP).

For example, if you spend $15,000 replacing your factory equipment, but record the cost as an operating expense, you’re violating GAAP principles.

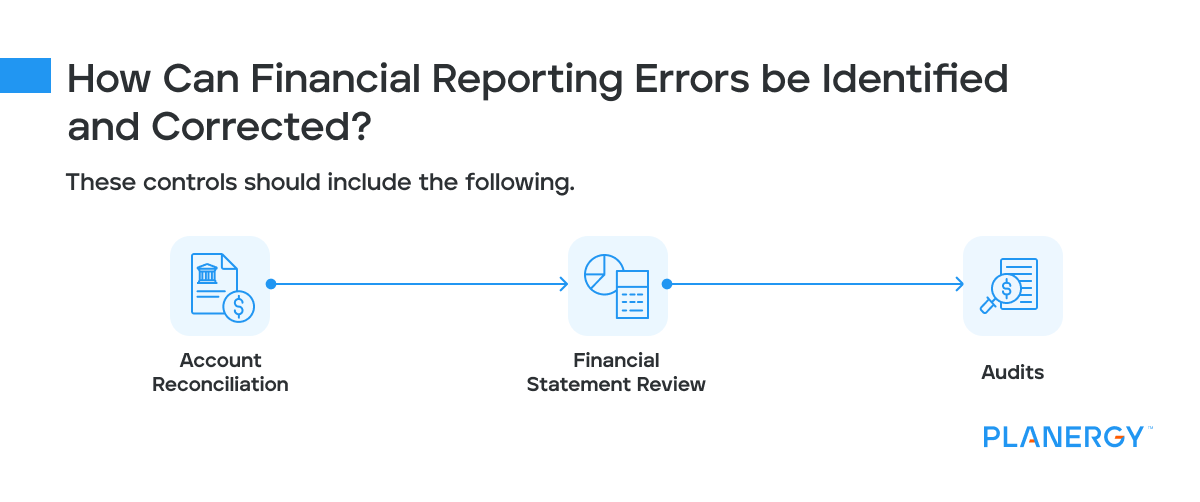

How Can Financial Reporting Errors be Identified and Corrected?

Having internal controls in place is one way you can identify accounting errors before financial statements have been finalized and distributed.

These controls should include the following.

Account Reconciliation

The most important reconciliation you’ll need to complete is your bank reconciliation.

Newer accounting software applications have made this process easier than ever.

Ideally, your bank reconciliation should be completed before running financial statements, since completing this process will help you identify income and expenses that have hit the bank but are not recorded in your general ledger.

In addition, completing the bank reconciliation can help you locate missing transactions and identify any potential data entry errors.

However, your bank account isn’t the only account that should be reconciled.

Other accounts such as your accounts payable, accounts receivable, inventory, and expense accounts should all be reviewed for potential errors and omissions.

Financial Statement Review

Another way to quickly identify potential issues is to review your preliminary financial statements.

This is best done by running month-by-month statements and comparing the results.

If you haven’t seen a major increase in spending or sales, your monthly results should trend in the same direction as the previous month’s statement.

This is one of the best ways to spot accounting errors such as transpositions or omissions because both of those will be easy to spot.

For instance, if your utility cost increased by $1,000 from the prior month, you may want to investigate that expense further to determine its legitimacy.

Audits

Both internal and external audits can guard against erroneous financial statements.

However, because audits are typically completed once a year, they aren’t a way to identify financial statement errors but are instead a way to identify prior period errors and safeguard against errors moving forward.

Once an error has been identified in your financial statements, you’ll need to make corrections.

If the error is located during a routine reconciliation, you can usually correct the error before financial statements are finalized and distributed.

How this is completed depends on the type of error made, when it occurred, and its impact on your financial statements.

There are two types of financial statement errors you should be aware of; a material error or an immaterial error.

A material error is one that directly impacts the results of your financial statement while an immaterial error will still need to be corrected but does not directly impact financial statement reporting.

If a material error is found in a prior period through an audit or internal review, the error will need to be corrected in that period, and an adjustment of opening balances restated for all accounting periods that have been impacted by the error.

An explanation of the error and its impact on the financial statements must be disclosed in the notes issued with the statements.

If an error is found in the current period, it can be corrected in that period without any repercussions on prior financial statements.

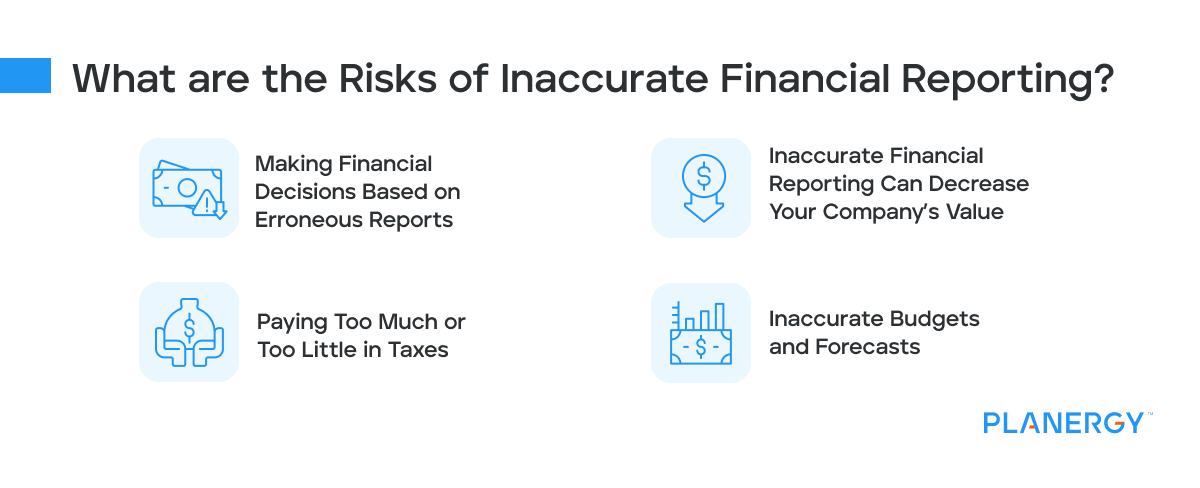

What are the Risks of Inaccurate Financial Reporting?

While an occasion error that is quickly corrected will not present any risk, regularly producing inaccurate financial statements carries a great deal of risk for businesses.

These risks include:

Making Financial Decisions Based on Erroneous Reports – The decision-making process is directly impacted by inaccurate financial reporting, which can cause any number of issues, including overdrawing your bank account.

Paying Too Much or Too Little in Taxes – If your profits are overstated due to errors, you’ll be paying more in taxes than you need to, while understating profits will cause you to pay less in taxes, which can result in late fees, penalties, and interest.

Inaccurate Financial Reporting Can Decrease Your Company’s Value –Revising reports or issuing financial statement corrections or restatements is a red flag for current and potential investors and other stakeholders and can lower stock prices.

Publicly held businesses that sign off on inaccurate financial statements may also be subject to regulatory penalties.

Inaccurate Budgets and Forecasts – It’s impossible to create an accurate budget or cash flow forecast if the numbers you’re using are not accurate.

Inaccurate reporting can also impact a business’s ability to obtain a business loan or line of credit.

Who Regulates Financial Reporting?

Two organizations actively regulate financial reporting.

In the U.S. the Financial Accounting Standards Board (FASB) is responsible for both establishing and regulating accounting and financial reporting standards for both public and private companies, with the Governmental Accounting Standards Board (GASB) responsible for setting those same parameters for both state and local governments.

Globally, the International Accounting Standards Board (IASB) is responsible for setting International Financial Reporting Standards (IFRS) and is used globally.

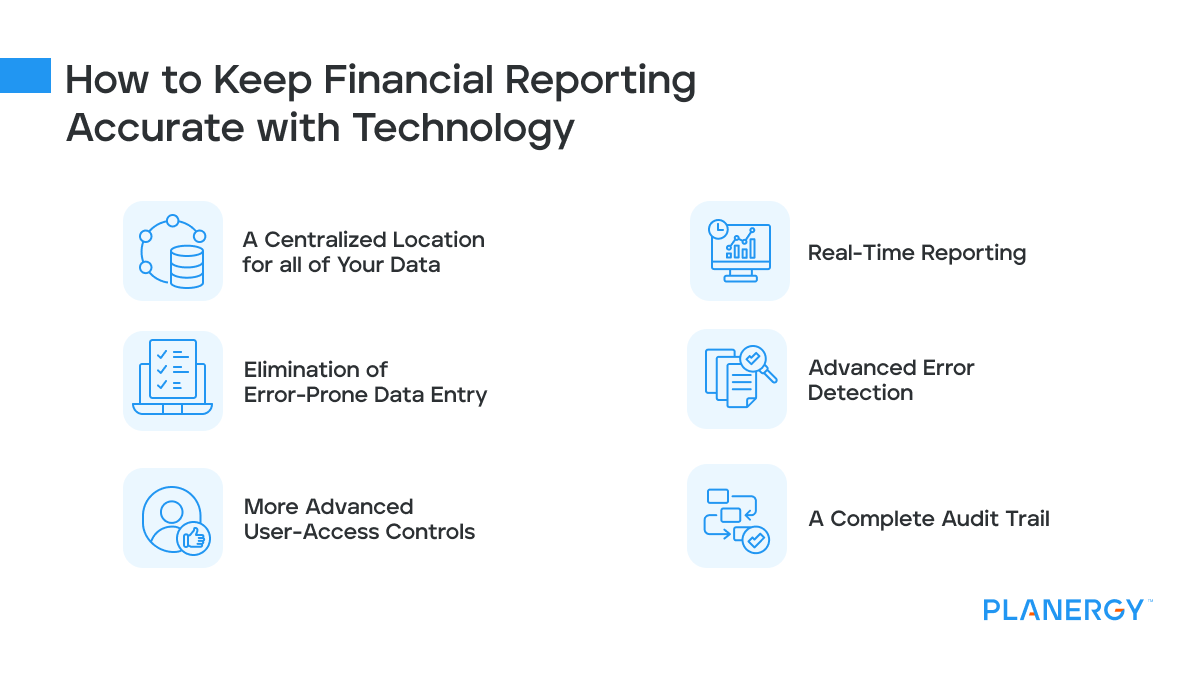

How to Keep Financial Reporting Accurate with Technology

AccountingWeb estimates that 27 percent of accounting errors are caused by data entry errors, with errors of omission and duplication close behind.

While implementing controls for your accounting practices and training staff properly on internal policies and procedures can help reduce the number of errors made, unless you automate your accounting system, chances are those errors will continue.

The best solution for eliminating errors is to implement an automated accounting system.

Doing so eliminates costly data entry errors while providing the following benefits to your business:

A Centralized Location for All of Your Data

By having all of your data at a centralized location, eliminating the need to enter transactions multiple times.

Real-Time Reporting

Using automation, you’ll have a streamlined financial reporting process in place at all times.

As a result, you’ll no longer have to wonder if everything is included in your financial reports.

Elimination of Error-Prone Data Entry

Using the latest technology, you can upload and extract data from invoices, which eliminates time-consuming data entry, which in turn, reduces the number of transaction errors significantly.

Advanced Error Detection

With the latest technology, you’ll be flagged if you try to enter an invoice more than once.

This same technology also flags exceptions, allowing you to quickly investigate discrepancies.

More Advanced User-Access Controls

One of the best ways to keep your information safeguarded is to limit the number of staff that have access to the platform.

This reduces errors and helps eliminate fraudulent activity.

A Complete Audit Trail

Having a complete audit trail is a necessity for businesses and can be extremely helpful during the annual audit process.

Taking the time to identify the issues that have contributed to financial reporting errors is the best way to correct inaccuracies.

By doing so, your business will be compliant, transparent, and accountable, solidifying your business reputation.

")