To properly manage their books, accountants and bookkeepers need to be familiar with both accounts payable and notes payable. While both accounts are liability accounts, there are significant differences between the two that need to be understood.

")

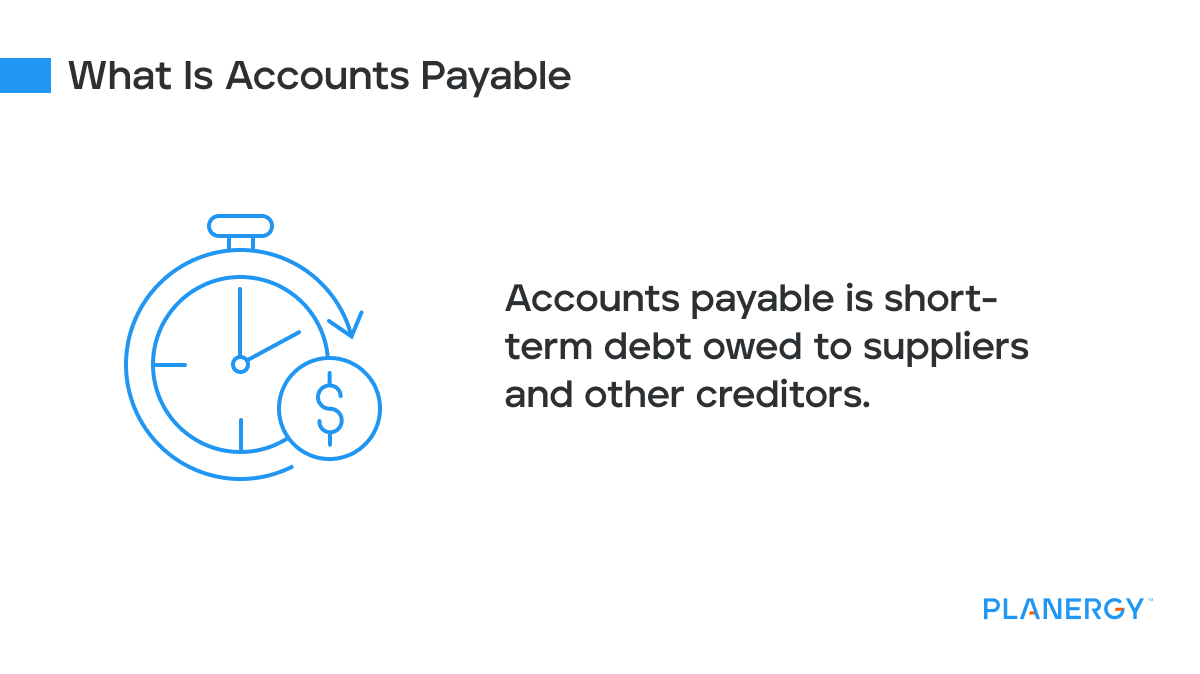

Accounts payable represents the money you owe to vendors, suppliers, and other creditors. Your accounts payable balance is considered a short-term debt or current liability and appears as such on your balance sheet.

Your accounts payable balance also directly impacts your cash flow statement along with your working capital.

A high accounts payable balance providing you with additional working capital, while a lower AP balance gives you less working capital to use for your business. This means AP also has an important role to play in liquidity management.

When invoices for items purchased on credit are entered into your accounting software application, a debit is made for the respective expense, while the accounts payable account is credited.

For example, an accounts payable entry for travel expenses for the month of June would look like this:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 6-15-2023 | Travel Expense | $900 | |

| 6-15-2023 | Accounts Payable | $900 |

The above entry ensures that the travel expense is posted in June, when it occurred, not in the month that the invoice was paid.

When the invoice is paid, the following reversing entry will need to be completed:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 7-10-2023 | Accounts Payable | $900 | |

| 7-10-2023 | Cash | $900 |

This entry reduces your accounts payable balance while also reducing your cash balance.

Accounts payable is considered a short-term liability because AP invoices are typically paid within a year’s time.

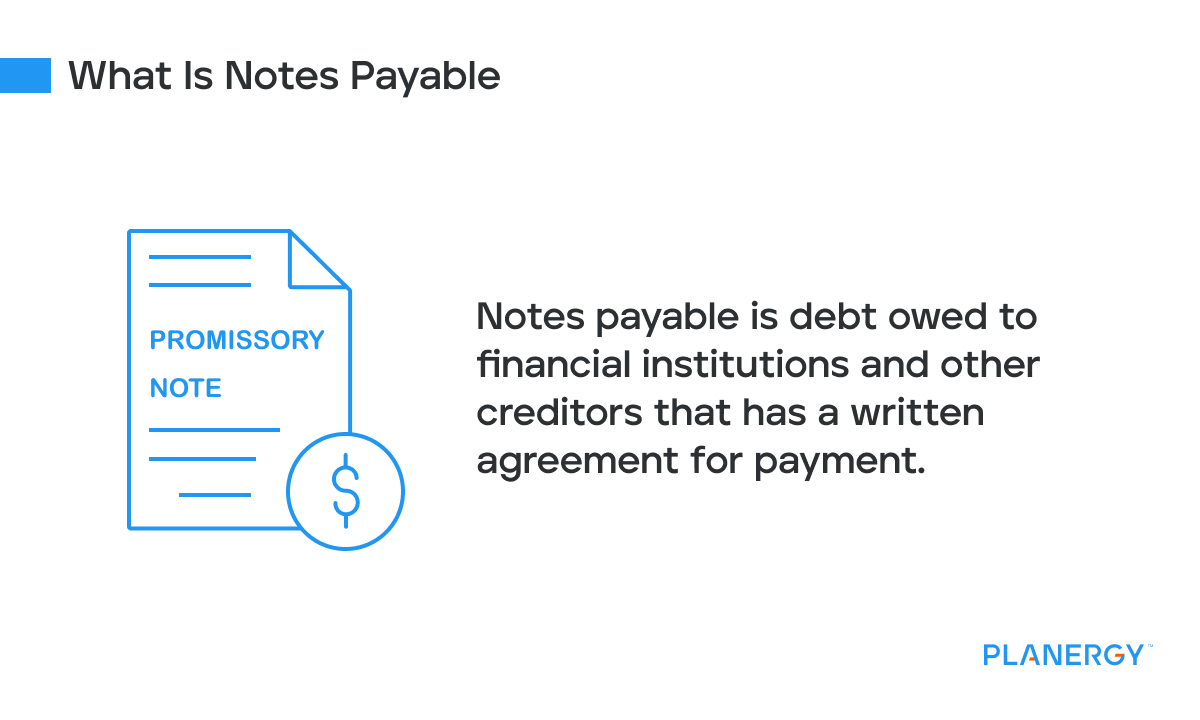

Notes payable represents the amount of money your business owes financial institutions and other creditors.

Notes payable entries always involve a written agreement between the buyer and seller, usually in the form of a promissory note. Like accounts payable, the current notes payable balance can be found on your company balance sheet.

A promissory note is a written promise to repay a loan. Promissory notes contain all the details of the loan including repayment terms, principal amount, interest rate, maturity period of the loan, as well as the date of the loan, and the signature of both the borrower and the lender.

A promissory note may also indicate whether there is a provision for late payment fees and whether the loan is secure or unsecured.

For example, in May, you take out a loan for $20,000 from a local bank to help fund your business. You agree to pay 10% interest on the loan which needs to be paid quarterly.

To record the loan as notes payable, you’ll first complete the following journal entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 4-01-2022 | Cash | $20,000 | |

| 4-01-2022 | Notes Payable | $20,000 |

Next, you’ll need to enter the interest expense for the quarter.

| Date | Account | Debit | Credit |

|---|---|---|---|

| 6-30-2022 | Interest Expense | $500 | |

| 6-30-2022 | Interest Payable | $500 |

When you pay the first quarterly interest expense, you’ll make the following entry, which should be paid at the end of the quarter.

| Date | Account | Debit | Credit |

|---|---|---|---|

| 6-30-2022 | Interest Payable | $500 | |

| 6-30-2022 | Cash | $500 |

You will have to continue making quarterly interest payments until the maturity date of the loan, entering a journal entry for September, December, and March to record the interest payments made on the loan.

Finally, when the note is paid off in full, you would complete the following entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 4-30-2023 | Notes Payable | $20,000 | |

| 4-30-2023 | Cash | $20,000 |

Notes payable are always in writing, with specific terms included, including the loan maturity date, which indicates the date that a business has to pay the principal amount owed plus any interest as shown in the promissory note if it has not already been paid.

Whether the promissory note indicates a maturity date of a year or five years, the balance in your notes payable account should always be reconciled against promissory notes that have been issued.

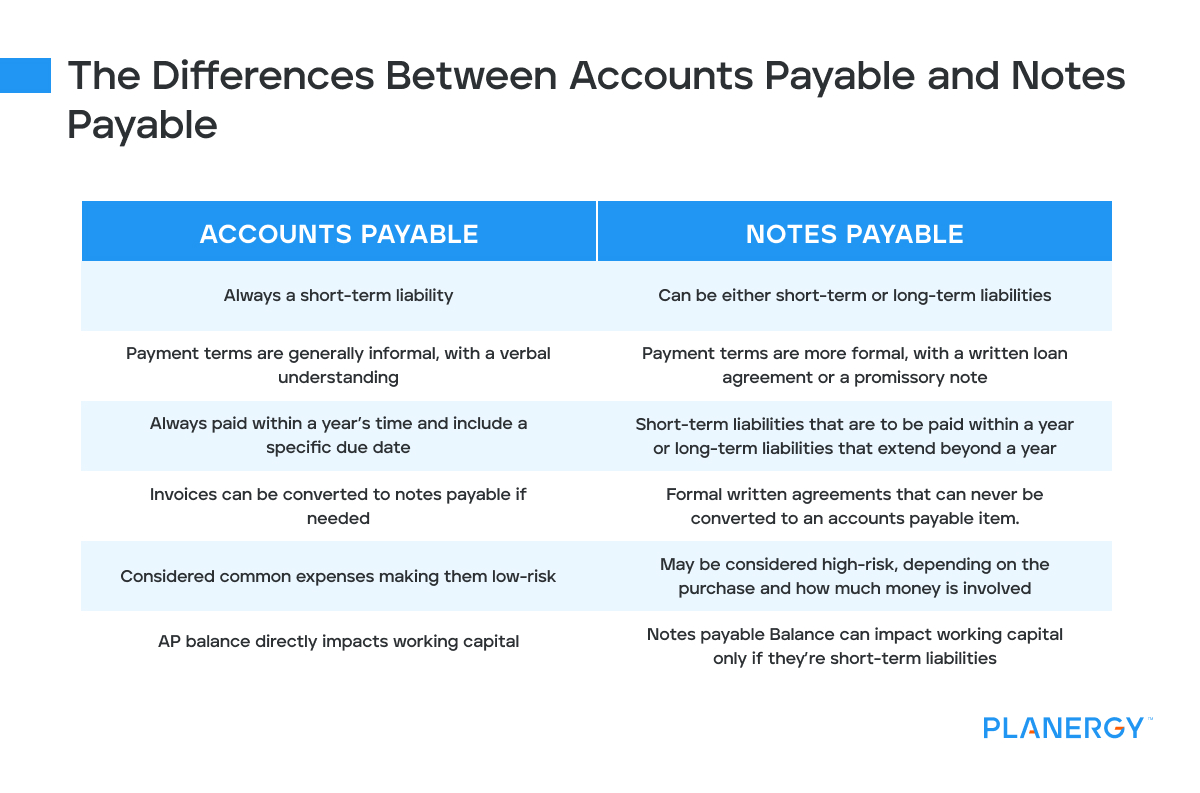

Though accounts payable and notes payable both represent money owed, in many ways they are quite different. One key difference between the two is that accounts payable is always a short-term liability while notes payable can be either short-term or long-term liabilities.

But there are other differences as well.

Accounts payable terms are generally informal, with a verbal understanding between the buyer and seller. AP terms usually include a specific due date along with a fee for late payment of the invoice, occasionally offering an early payment discount option as well.

Notes payable terms are more formal, with a written loan agreement or a promissory note issued that provides details on repayment terms, interest rates, payment schedules, and specific clauses that are put into place to address late payment or payment default.

Accounts payable are always paid within a year’s time and include a specific due date that is based on terms provided by the vendor or supplier.

Notes payable can be either short-term liabilities that need to be paid within a year or long-term liabilities when payment terms extend beyond a year.

Accounts payable invoices can be converted to notes payable if desired. This is typically done for invoices in larger amounts that a company is unable to pay within the original terms of the invoice.

Notes payable are formal, written agreements and can never be converted to an accounts payable item.

Accounts payable invoices are considered common expenses making them low-risk.

Notes payable may be considered high-risk, depending on the purchase and how much money is involved, which is why an interest charge is normally included on notes payable items. Typical notes payable expenses can include purchasing a building, purchasing business equipment, business loans or lines of credit.

Accounts payable balances directly impact working capital and play an important role in proper working capital management and day-to-day business operations. Better management of accounts payable can have a positive impact on cash flow.

Notes payable balances can also impact working capital, but only if they’re short-term liabilities, which can be used to estimate current working capital. Long-term liabilities should not be included in working capital estimates.

While notes payable uses a formal written agreement or promissory note, managing notes payable is a straightforward task.

However, when managing accounts payable, there are numerous processes that need to be performed regularly to ensure AP accuracy and proper processing.

These tasks include:

Depending on your organization, your accounts payable department may be responsible for sourcing and managing vendors and suppliers or it may be handled by the procurement department.

Whether AP or procurement is responsible for managing vendors and suppliers, both finance and procurement departments need to work together to ensure suppliers are managed properly from the very beginning.

Accounts Payable will always play an important role in managing vendor relationships. If you are not paying your suppliers invoices on time they are not going to remain happy to work with you over the longer term.

If you’re still using a manual AP system to process AP, your invoice processing time will be much higher than a company using AP Automation software.

Invoice processing requires the completion of the following:

Paper invoices require proper distribution to the correct department but invoices can become lost in the process, delaying processing times considerably. Delivering invoices electronically can save tremendous processing time.

Three-way matching helps authenticate any invoice by matching key totals such as pricing, invoice totals, quantities, and due dates against a corresponding purchase order and shipping receipt.

An automated system completes this time-consuming task for you, saving you both time and labor costs.

Again, if you’re using a manual AP system, your invoice approval processing will be manual as well, which often results in missing invoices and approval delays.

Issuing paper checks can cause numerous delays, ranging from check fraud to payments lost in the mail. They’re also an added burden during bank reconciliation time, requiring additional work hours to follow up on uncashed checks.

On the other hand, notes payable requires two processes; setting the expense up in the general ledger and timely payments made to the holder of the note.

Both are vital but fairly uncomplicated compared to managing accounts payable processes.

")

")