We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

While reconciling your bank statement, you notice the bank debited your account twice for $2,000 in error. You immediately contact the bank and they correct the error.

What would have happened if you hadn’t reconciled your account? The charge would have remained, and your bank balance would have been $2,000 less than the balance in your general ledger.

That’s why account reconciliation remains a key component of the financial close process. For publicly held companies, the reconciliation process is a necessity, mandated by Section 404 of the Sarbanes-Oxley Act which requires public companies to include an assessment of their internal controls with their annual report.

For small businesses, the account reconciliation process helps identify potential misstatements and ensures the accuracy of financial statements.

Reconciliation in accounting is the process of reconciling the balance between two different sets of documents.

For example, when you complete a bank reconciliation, you’re reconciling your ending bank balance with your ending general ledger balance to ensure that the two totals match, while finding and resolving any discrepancies found during the reconciliation process.

But before beginning the reconciliation process and focusing on the different types of reconciliations that should be completed, you’ll first need to understand the following accounting terms, including what they are and how they differ.

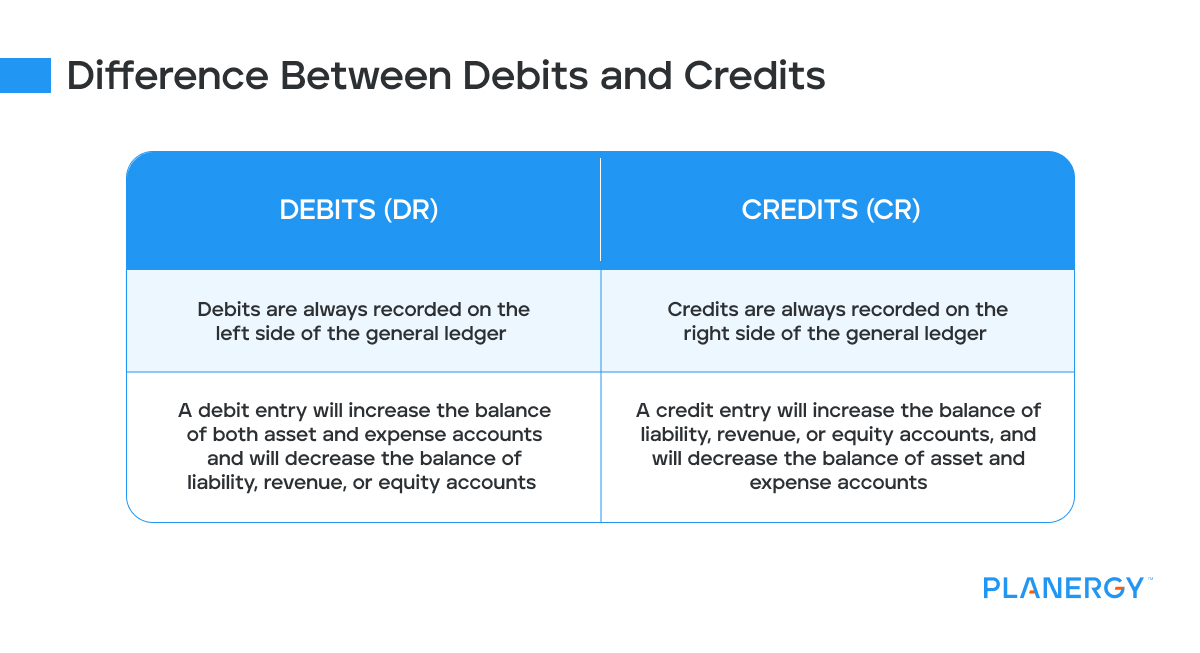

Debits and Credits

Debits and credits are truly the backbone of the double-entry accounting system, which states that every debit entry must have a corresponding credit entry for the books to remain in balance.

DEBITS (DR)

CREDITS (CR)

Debits are always recorded on the left side of the general ledger

Credits are always recorded on the right side of the general ledger

A debit entry will increase the balance of both asset and expense accounts and will decrease the balance of liability, revenue, or equity accounts.

A credit entry will increase the balance of liability, revenue, or equity accounts, and will decrease the balance of asset and expense accounts.

Though you may not see the process if you’re using accounting software, because this is generally automated, if you enter a debit to an account you will have to enter a corresponding credit for the account to remain in balance.

For example, when you pay your utility bill, you would debit your utility expense account, which increases the balance and credit your bank account, which decreases the balance.

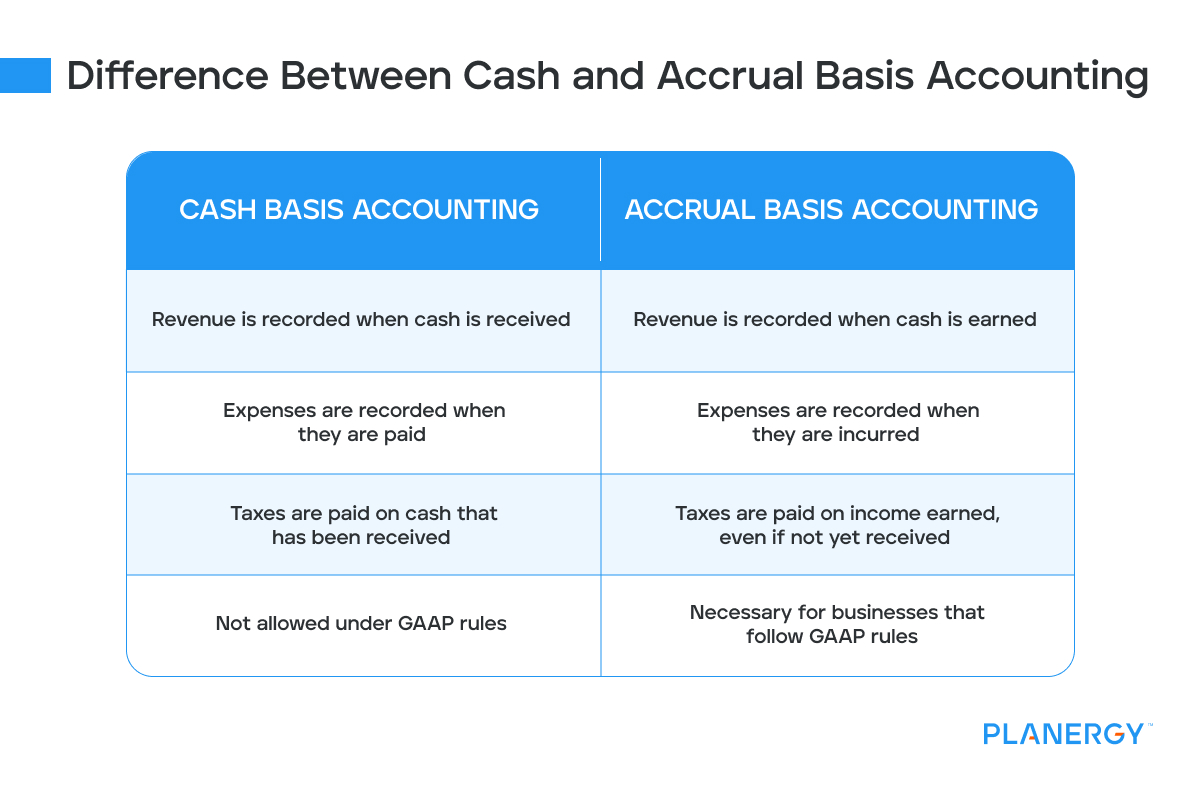

Cash accounting is the easiest way to manage your accounting, and provides a better picture of your cash flow, but is only a suitable method for very small businesses.

Accrual accounting is more complicated but provides a better insight into the financial health of your business. There are significant differences between these two methods.

CASH BASIS ACCOUNTING

ACCRUAL BASIS ACCOUNTING

Revenue is recorded when cash is received

Revenue is recorded when cash is earned

Expenses are recorded when they are paid

Expenses are recorded when they are incurred

Taxes are paid on cash that has been received

Taxes are paid on income earned, even if not yet received

Not allowed under GAAP rules

Necessary for businesses that follow GAAP rules

While very small businesses can use cash basis accounting, if you have employees or have depreciable assets, you’ll need to use accrual basis accounting.

Balance Sheets

Balance sheets and profit and loss statements are both essential resources for determining the financial health of your business.

A balance sheet is used for determining what a business owns (assets) and what it owes (liabilities). A balance sheet also displays owner equity, which is part of the accounting equation of:

assets = liabilities + owner’s equity

Balance sheets and profit and loss statements are both essential resources for determining the financial health of your business.

Profit and Loss Statements

A profit and loss statement, also known as an income statement summarizes revenue and expenses that have been incurred during a specific period.

A profit and loss statement displays revenue earned for that period, then subtracts the cost of goods sold, interest expense, and other operating expenses from the revenue to determine net income for the period.

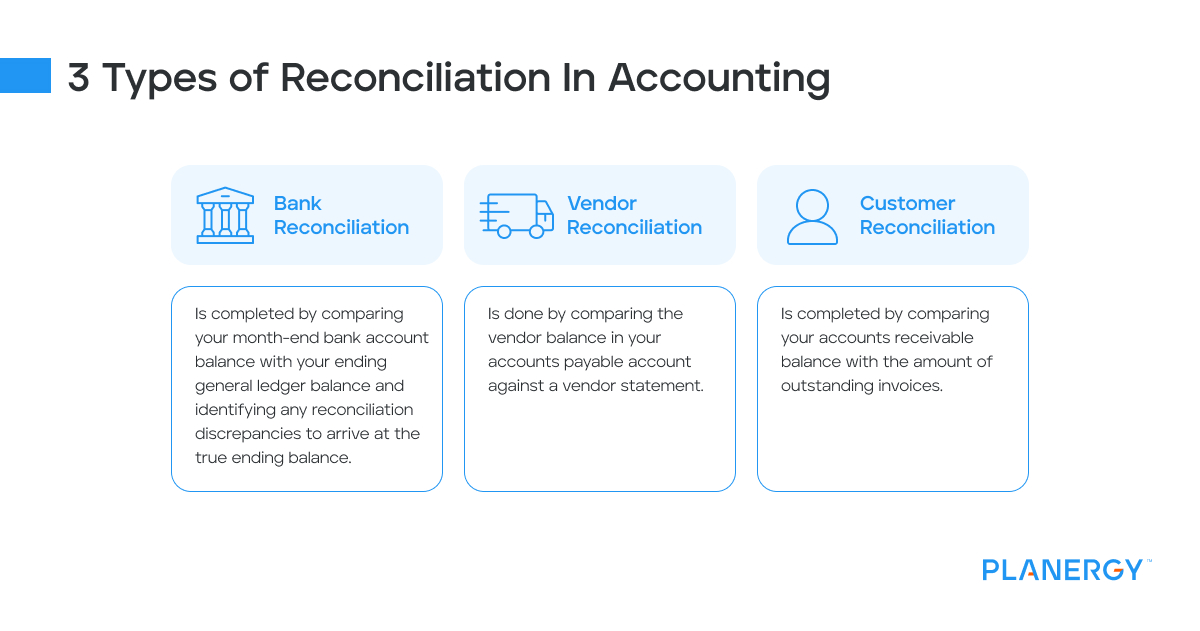

What are the Types of Reconciliation in Accounting?

No matter what you’re reconciling, it will involve comparing two sets of records to determine accuracy. In accounting, three common types of reconciliations are commonly used.

Bank Reconciliation

The bank reconciliation process is perhaps the most common accounting reconciliation that is completed regularly.

The bank reconciliation process is completed by comparing your month-end bank account balance with your ending general ledger balance and identifying any reconciliation discrepancies to arrive at the true ending balance.

For example, if you write checks regularly, you’ll likely have a list of outstanding checks at the end of the month that will need to be accounted for.

Reconciling your bank account can also help identify any bank errors and allow you to post service charges and any return item fees to your general ledger.

Vendor Reconciliation

Vendor reconciliation can be important for businesses that commonly process a large number of supplier and vendor payments.

This is done by comparing the vendor balance in your accounts payable account against a vendor statement. Both should match unless there is a payment in transit or a payment that has not yet been made.

Customer Reconciliation

Used in accounts receivable, if you sell products and services on credit, you’ll likely have an accounts receivable balance that will need to be reconciled. The balance shown in your accounts receivable balance should always match the amount of outstanding invoices. Likewise, the amount of payment received should always match the amount billed to your customers, minus any outstanding payments.

Depending on your business, you may also want to reconcile your inventory account, which is typically completed by doing a complete accounting of all inventory on hand. You may need to also reconcile goods received not invoiced also.

Larger businesses with several branches may also need to complete intercompany reconciliations.

What Is the Difference Between Account Reconciliation and Financial Reconciliation?

Account reconciliation is a financial reconciliation, with no real difference, except for how the results of the reconciliation process will be used.

For example, reconciling general ledger accounts can help maintain accuracy and would be considered account reconciliation. While reconciling your bank statement would be considered a financial reconciliation since you’re dealing with bank balances.

What Is the Difference Between Account Reconciliation and Invoice Reconciliation?

While the reconciliation process remains the same, with two sets of documents compared for accuracy, the difference lies in what is being reconciled.

Account reconciliation is done to ensure that account balances are correct at the end of an accounting period. The account reconciliation process also helps to identify any outstanding items that need to be taken into consideration in the reconciliation process.

For example, when completing a bank reconciliation, any checks that have not yet cleared the bank are considered outstanding, with those check amounts subtracted from the ending bank balance so that it matches with the general ledger balance, which has already recorded those same checks.

Invoice reconciliation also compares two sets of documents for accuracy, but instead of ending balances, you’re comparing invoice details against a hard copy.

Reconciling invoices once they’ve been entered into your accounting application can help identify potential errors and help to prevent duplicate payments, underpayments, and overpayments, with reconciling invoices against a bank statement as another option.

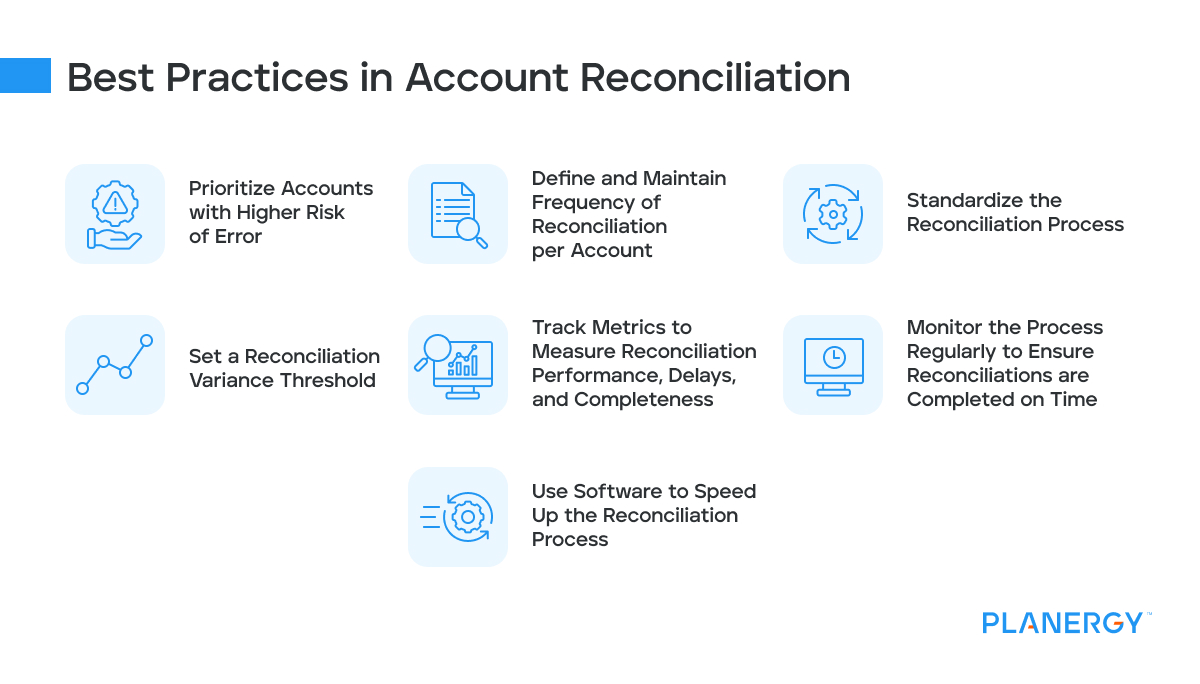

What Are Best Practices in Account Reconciliation?

It is important to follow best practices for account reconciliation. According to the Journal of Accountancy, account reconciliation best practices should include:

Prioritize reconciling accounts that have the greatest risk of error.

Determine the frequency (e.g., monthly, quarterly) of reconciliation for each account.

Create a series of processes for all reconciliations that should be followed company-wide.

Accounts don’t have to be reconciled to the penny to be in balance. Set a threshold for variances and stick to it.

Use metrics to measure reconciliation performance to spot delays and measure completeness.

Monitor the reconciliation process regularly to make sure reconciliations are completed on time.

Use technology to improve the reconciliation process. Programs using AI and machine learning, like PLANERGY’s AP Automation software, can assist in the reconciliation process and point out discrepancies much faster than manual reconciliations can.

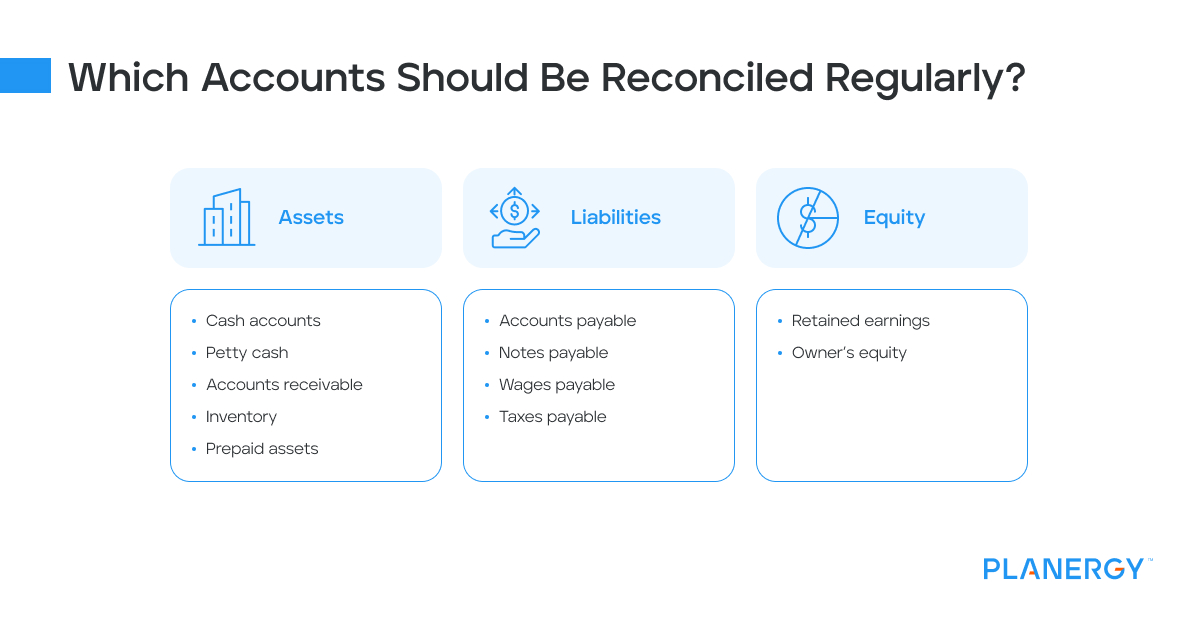

Which Accounts Should Be Reconciled Regularly?

All balance sheet accounts including asset, liability, and equity accounts should be reconciled regularly. Balance sheet reconciliations should include the following:

Assets

Cash accounts

Petty cash

Accounts receivable

Inventory

Prepaid assets

Liabilities

Accounts payable

Notes payable

Wages payable

Taxes payable

Equity

Retained earnings

Owner’s equity

Because these account balances are carried forward from year to year, they should be reconciled regularly. It’s also helpful to reconcile expense accounts for accuracy as well.

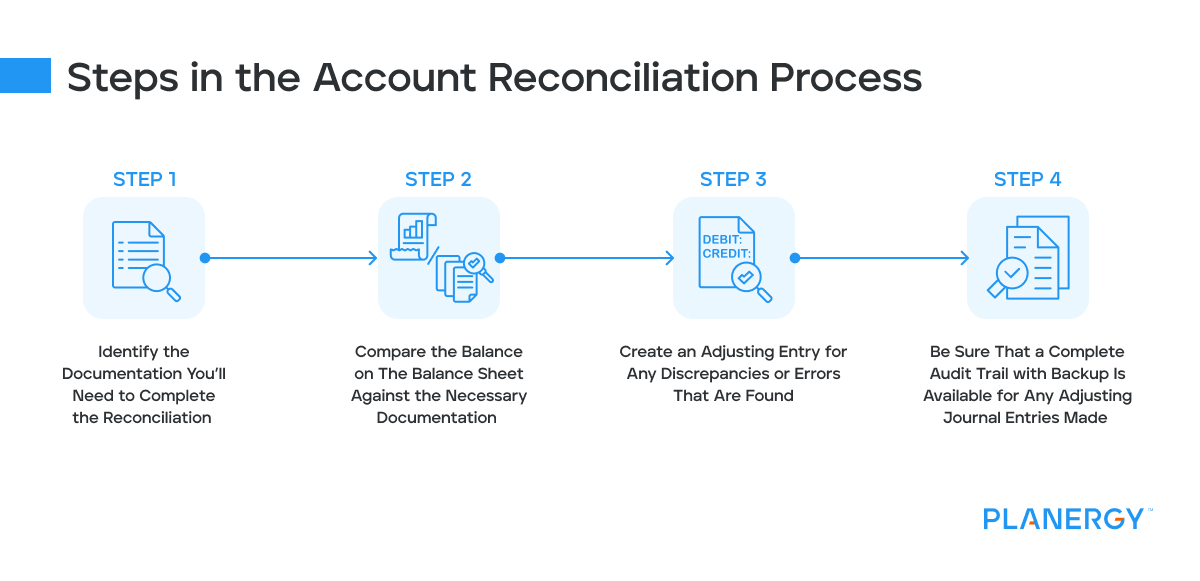

What Are the Steps in Account Reconciliation?

There are several steps involved in the account reconciliation process, depending on the accounts that you’re reconciling.

Identify the documentation you’ll need to complete the reconciliation. For example, if you’re reconciling your cash accounts, you will need your current bank statement for that period. If you’re reconciling your travel expense account, you’ll probably need to compare expenses against a credit card statement.

Compare the balance on the balance sheet against the necessary documentation, taking note of any missing transactions or discrepancies that will need further investigation.

Create an adjusting entry for any discrepancies or errors that are found during the reconciliation process.

Be sure that a complete audit trail with backup is available for any adjusting journal entries made to correct any issue found in the reconciliation process.

These steps can vary depending on what accounts you are reconciling, but the underlying premise is always the same – compare your ending balance against supporting documentation and make any adjustments as needed.

What Is an Example of Accounting Reconciliation?

ABC Manufacturing receives its monthly bank statement in the mail. The ending bank balance is $37,850, while their general ledger balance is $45,000.

These are the steps required to complete the reconciliation process.

Subtract from the bank balance any checks that have been issued but have not yet cleared the bank. For this reconciliation, five outstanding checks total $4,975.

Add to the bank balance any deposits that were made that have not been deposited.

There was one deposit that was recorded in the general ledger for $12,000, but because of timing differences, did not hit the bank until the following month.

Subtract from the general ledger balance any bank fees that have not been recorded. For this month, there was a $25 service fee that was not recorded in the general ledger.

Identify any bank transactions that do not have a corresponding general ledger entry for legitimacy.

There was one manual check issued for $100 that was never recorded in the general ledger that will need to be subtracted from the general ledger ending balance.

The reconciliation spreadsheet will look like this:

Bank Balance

General Ledger Balance

Ending balance: $37,850

Ending balance: $45,000

Outstanding checks: – $ 4,975

Bank service fee – $ 25

Deposit in transit +$12,000

Check not recorded – $ 100

Ending Balance $44,875

Ending Balance $44,875

Why Is Account Reconciliation Important?

Keeping your accounts reconciled is the best way to make sure that your balances are accurate and an important part of ensuring adequate financial controls are in place.

Using the bank reconciliation example above, if your spending doesn’t take into account the $12,000 in outstanding checks, you can easily overspend available funds.

The same process holds when reconciling your accounts receivable balance. If your AR balance is $60,000, but you only have $40,000 in invoices that are due, your net profit will be overstated and you’ll be paying taxes on income that you’ll never receive.

Regularly reconciling your accounts, especially bank accounts and credit card statements can also help you identify suspicious activity and investigate it immediately, rather than months after it has occurred. And if you never reconcile your accounts, chances are that fraudulent activity will continue.

Account reconciliations can also help identify bank and credit card errors. Though rare, it’s not unheard of that a bank or credit card company makes an error on your account, perhaps deducting funds for a check that isn’t yours, or charging you for a purchase that you never made.

And while most financial institutions do not hold you responsible for fraudulent activity on your account, you may never know about that fraudulent activity if you don’t reconcile those accounts.

Using accounting software will make it much easier to reconcile your balance sheet accounts regularly.

Today, most accounting software applications will perform much of the bank reconciliation process for you, but it’s still important to regularly review your statements for errors and discrepancies that may appear.

Finally, without adequate account reconciliation processes in place, both internal and external financial statements will likely be inaccurate.

Automated Reconciliation Is Best for Your Business

Whether you’re a small business owner working with multiple sub-ledgers or a multi-million dollar business using an ERP system, reconciling your accounts will always be necessary.

It’s also a very time-consuming process if it’s completed manually. Accounting software automation and adding a procure-to-pay software, like PLANERGY, can streamline the process and increase functionality by automatically accessing the appropriate financial records.

Automated reconciliation also flags discrepancies so they can be investigated immediately rather than months later.

The frequency of your reconciliation process can be determined by the size and type of business.

A business that processes a few transactions a month may be able to reconcile its accounts monthly, while a larger business with hundreds of transactions daily may need to reconcile its accounts more frequently.

The important thing is to establish internal processes for account reconciliation and adhere to those processes. Your CPA will thank you.

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.