We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with PLANERGY.

Accounts payable accruals are a very specific type of expense accrual that is typically recorded at year-end, though some companies may find it necessary to record accounts payable accruals at other times as well.

Though similar to expense accruals, there are some very distinct differences between these two essential accounting tasks, and when each one should be used.

Cash basis accounting can be useful for very small businesses that do not have a staff to pay or a lot of business expenses.

Cash basis accounting means that income and expenses are not recognized until money changes hands.

For example, if you receive a bill from your office cleaner, the expense is not recorded until you pay the bill. The same premise holds for incoming cash.

If a client owes you $1,000, using cash basis accounting, you won’t record the income until the payment is received from your client.

The biggest benefit to cash basis accounting is that it’s easy. Cash basis accounting also provides a much clearer picture of your current cash flow.

The downside is that it does not provide a true reflection of your business finances.

Instead of recognizing income and expenses when money changes hands, they are recorded when incurred.

When you bill your client $1,000, you record it in the accounting period when the work was done, not when you receive the payment.

The same goes for expenses. When you receive your utility bill for the month, you record it for the month you’re being billed for, not when they are paid.

Accrual accounting is necessary for growing businesses and is required by GAAP (Generally Accepted Accounting Principles) for all publicly held businesses.

On the other hand, accrual basis accounting is also more complicated, and requires some accounting knowledge, particularly when dealing with accrued expenses.

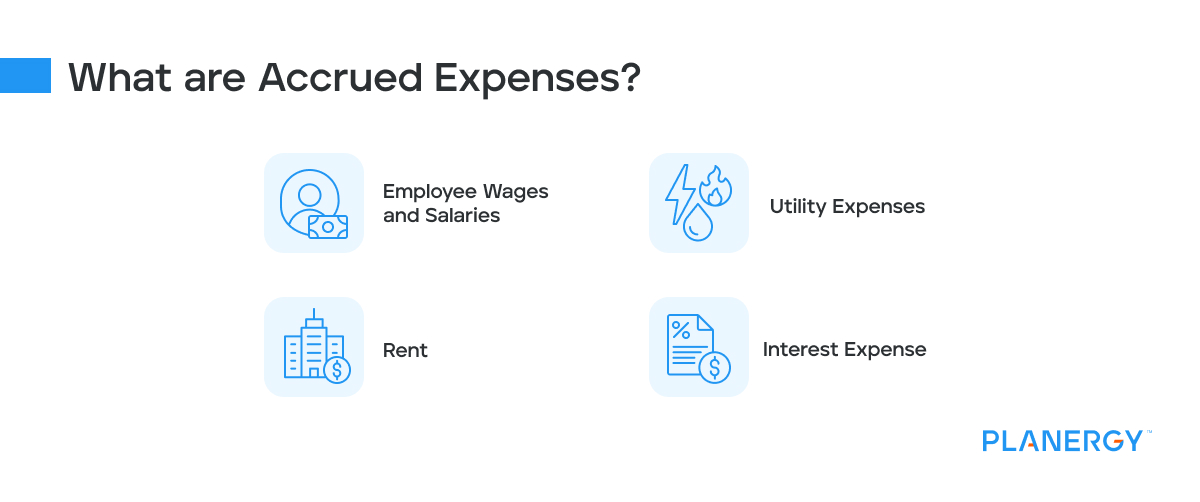

What Are Accrued Expenses?

Accrued expenses are expenses that are recorded in your general ledger before payment has been made.

If you are using the accrual method of accounting, you will need to accrue both accounts payable and other expenses periodically.

Accrued expenses generally include the following:

Employee wages and salaries

Utility expenses

Interest expense

Rent

In the examples above, you will not receive a corresponding invoice for these expenses, yet they still need to be recorded as an expense.

Examples of Accrued Expenses

It’s month-end and you won’t receive the actual electric bill for April until May.

To ensure that your utility expense is recorded for April, you’ll want to accrue April’s electric bill.

The accrual journal entry would be as follows:

April 30

Account

Debit

Credit

Utility Expense

$150

Accrued Expenses

$150

This journal entry is completed so that your expenses will be accurately reflected in your monthly financial statements.

In May, when the water bill is paid, you’ll need to complete the following adjusting entry:

May 1

Account

Debit

Credit

Accrued Expenses

$150

Utility Expenses

$150

The second journal entry reverses the original journal entry.

When you receive the actual bill, which is $145, that bill is then entered into the AP system for payment in late May.

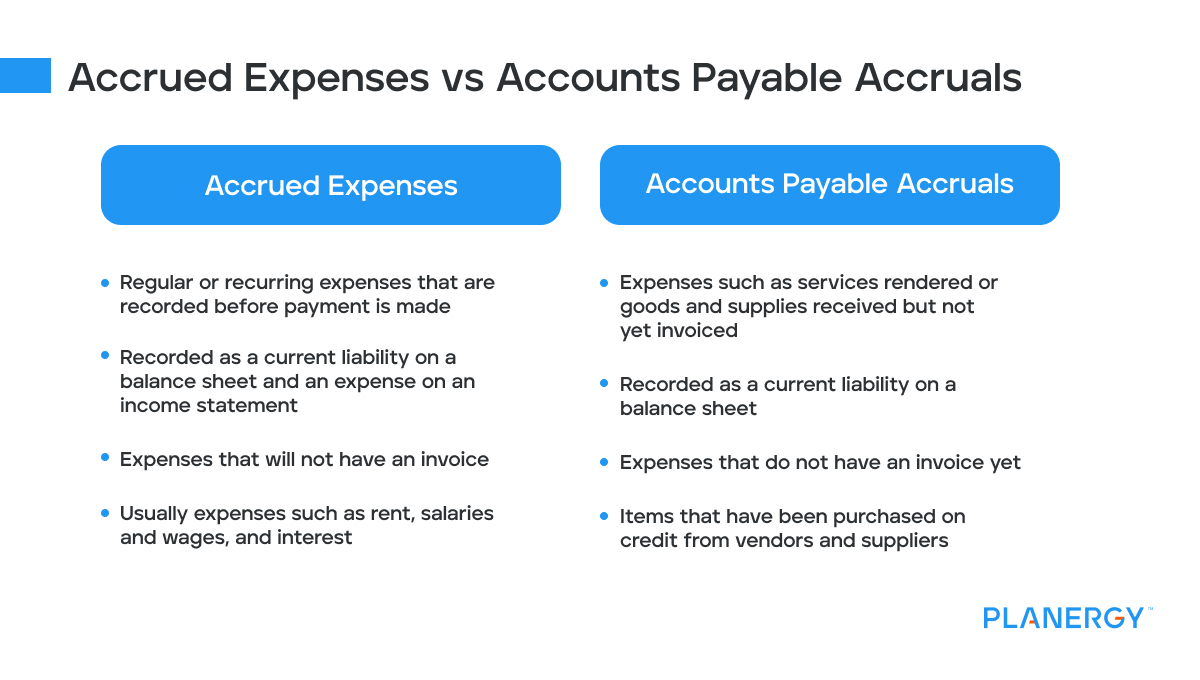

Are Accounts Payable Accruals Considered Accrued Expenses?

Both accounts payable and accounts payable accruals are considered short-term debt since they are typically paid within a year’s time.

The utility bill above is a perfect example of an accrued expense.

Other accrued expenses that you’ll likely process include wages and salaries along with bank interest on a loan, all expenses that will need to be accrued at month’s end to ensure that financial statements are accurate.

The scenario is slightly different for accounts payable accruals. Accounts payable accruals are typically tied to goods and services that were purchased on credit. Let’s look at a typical accounts payable entry using the following scenario.

Let’s say you ordered $2,500 worth of inventory products on March 16th. You receive the product on March 21 and the invoice on March 25th.

With the invoice in hand, you (or your accounting software application) can make the following entry:

March 25

Account

Debit

Credit

Inventory

$2,500

Accounts Payable

$2,500

This means that even if your payment terms with your supplier is Net 45, you’ll be recording the expense in March, where it belongs.

But what happens if March draws to a close and you still haven’t received an invoice for the inventory you received on March 21?

You’ll have to accrue it with the following journal entry:

March 31

Account

Debit

Credit

Inventory

$2,500

Accrued AP Expenses

$2,500

You’ll have to remember to reverse the entry when the invoice is received so that your expenses are not overstated.

Reversing the accrual is particularly important if you have an automated AP system that records invoices when received.

However, if you’re using a manual system, many accountants may opt to skip the traditional reversal and record the payment by completing the following journal entry when the invoice has been paid.

April 15

Account

Debit

Credit

Accrued AP Expenses/td>

$2,500

Cash

$2,500

You’ll notice that only part of the original entry was reversed. Though the easier option, this is typically only used with manual accounting systems.

In most cases, it’s better to enter the invoice into accounts payable and pay it from there.

What’s the Difference Between Accounts Payable Accruals and Accrued Expenses?

It’s important to reconcile your accounts monthly to make sure that any supplies or products that have been received or services rendered, but have not yet been invoiced, are accounted for as a month-end AP accrual.

What Are Year-end AP Accruals?

Year-end AP accruals are similar to other year-end accruals that a business may need to process.

Again, the end of your fiscal year is the perfect time to reconcile your AP account to ensure that all items that have been ordered and received have a corresponding invoice.

If an invoice has not yet been received, that amount will need to be accrued.

John’s company ordered a dozen laptops for its employees in mid-December for $15,000. The computers were received in late December, but as of December 31, an invoice had not yet been received.

To correctly show that the expense belongs in December, you’ll need to accrue the expense. The invoice is received on January 10 of the following year.

To properly record this expense, you will need to make the following journal entries:

Step 1.

December 31, 2022

Account

Debit

Credit

Computer Expense

$15,000

Accrued Expense

$15,000

Step 2.

Account

Debit

Credit

Accrued Expense

$15,000

Computer Expense

$15,000

But you’re not done yet. When the invoice arrives in early January, you’ll now need to enter the invoice detail and the expense again.

But because you already reversed the accrual from December, entering the computer expense now will have no impact on your company’s balance sheet or income statement because they zero each other out.

Many of these steps are partially or fully automated if you’re using accounting software.

Step 3.

January 1, 2023

Account

Debit

Credit

Computer Expense

$15,000

Accrued Expense

$15,000

Once the invoice is paid in February, the accounts payable balance will be zeroed out by doing the following entry:

Step 4.

February 10, 2023

Account

Debit

Credit

Accounts Payable

$15,000

Cash

$15,000

This illustrates the steps that it takes to post accruals but also the steps that need to be taken to adequately reverse them.

That’s why handling your accounting manually can often be overwhelming, resulting in missed items, inaccurate cash flow statements, and other financial statements.

What Is the Difference Between Accruals and Prepayments?

While accruals and prepayments are both used to ensure that financial statements reflect accurate income and expense totals, they represent two very different aspects of accounting.

Accruals are liabilities that are recorded in the general ledger at month’s end to account for expenses that have occurred during a specific accounting period that have not yet been paid.

For example, wages and salaries are often accrued at the end of one accounting period because they won’t be paid until the following accounting period.

Prepaid expenses are expenses that are paid in advance.

For example, you have a contract with a local cleaning service to clean your office at a rate of $13,000 annually, with the cost dropping to $12,000 if you pay for the entire year upfront.

You take advantage of the discount and pay the entire amount in January.

However, you don’t want to show a $12,000 expense for January, so you’ll record it as a prepaid expense, and expense a set amount each month until the prepayment has been used in its entirety.

The initial journal entry would be for the total amount:

January 31, 2023

Account

Debit

Credit

Prepaid Expense

$12,000

Cash

$12,000

Next, you’ll want to expense $1,000 a month for the next twelve months for cleaning expenses, until the entire $12,000 has been expensed.

Starting in January and for each month in 2023, you will complete the following journal entry:

January 31, 2023

Account

Debit

Credit

Cleaning Expense

$1,000

Prepaid Expense

$1,000

This entry records the $1,000 expense each month while reducing the prepaid expense account balance each month as well.

Prepaid expenses are often used for paying for yearly contracts such as insurance, subscriptions, memberships, and even rent.

How Can Software Help Report on Accruals More Quickly and Accurately?

Managing accruals manually can be overwhelming. Not only will you have to remember to manually enter an accrual at month-end, but you’ll also have to remember to reverse that accrual the following month.

Forgetting to do so can seriously impact the accuracy of your financial statements.

Using an automated accounting software application, posting accruals is a much simpler process, with most of today’s accounting software applications automatically reversing accrual entries the following accounting period.

Using accounting software also makes it easier to pinpoint missing invoices, allowing you to follow up with vendors and suppliers promptly, eliminating the need to accrue accounts payable.

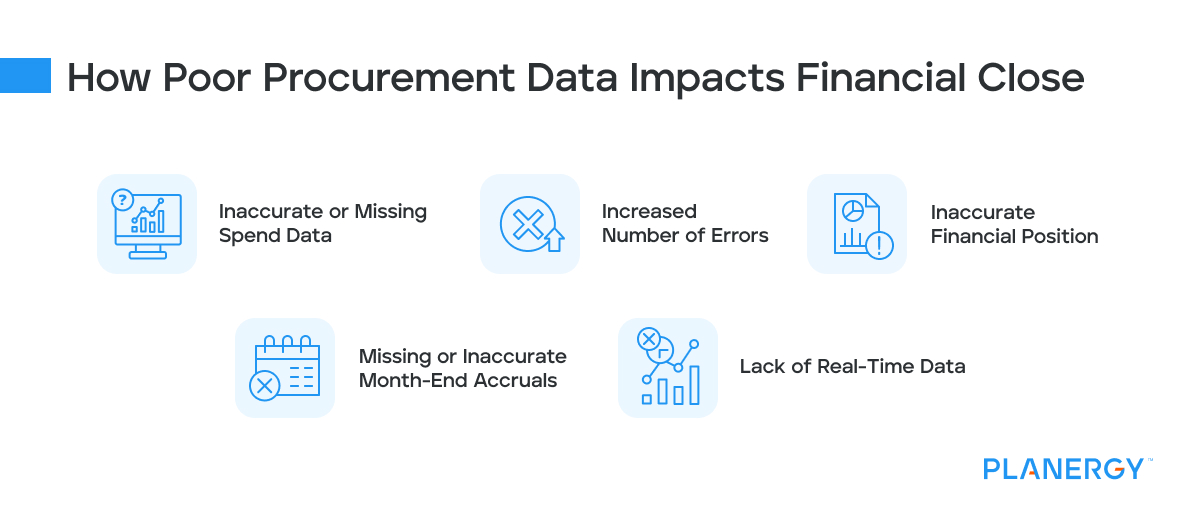

How Does Poor Procurement Data Impact Financial Close?

The ultimate goal when managing financial close is to produce financial statements that provide an accurate, in-depth look at your business.

Poor procurement data can directly impact that accuracy in several areas including:

Inaccurate or missing spend data

Increased number of errors

Lack of real-time data

Missing or inaccurate month-end accruals

Inaccurate financial position

Using an automated procurement and accounts payable application, like PLANERGY, can eliminate these challenges and more, providing filtered reports on committed spend and GRNI, so you can be confident that your month-end close is accurate.

What Are Best Practices for Accounts Payable Accruals?

Aside from regular accruals that are completed monthly or annually, reconciling your AP accounts can help you determine when it’s necessary to accrue accounts payable expenses.

Reconciling your accounts regularly can also help you spot inaccuracies or accruals that may need to be reversed.

By far, the best practice for handling accounts payable accruals or any accruals is to automate your accounting system.

Automation Is a Necessity to Properly Manage Accruals

AP departments can experience other benefits when utilizing an automated accounting or procurement application.

Linking procurement data with your accounts payable and financial close has many benefits, including the following:

The ability to capture expenditures immediately

Automating three-way matching which reduces errors while freeing up staff time considerably

1. Use PLANERGY to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how PLANERGY can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

")

")

")